Latin America’s political dance card is full for the

rest of the year. The region will face more Presidential elections in

one year than it has in over a generation, a coincidental confluence of

electoral calendars. Remarkably, the experienced players in the region,

be they financial or direct investors, are calm. Latin America will

likely enjoy a year of moderate to healthy growth, a fourth consecutive

year of expansion, thanks to strong commodity prices that favor many of

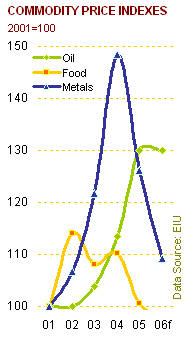

the region’s economies. In 2006 the price of oil, metals and food

commodities will impact the region more than the busy election cycle.

Three

successive years of commodity price growth (five years in the case of

oil) have generated a massive cumulative cash windfall for the region’s

largest economies. Currencies have appreciated, imports have grown, and

increased liquidity has reduced interest rates in almost every market.

In Chile and Mexico, where longer positive track records are in place,

the markets are so liquid that consumer credit is now accessible to the

majority of the population. In recovering economies like Argentina,

Brazil, Colombia and Peru, growth is only now switching gears from

export-led to domestic consumer-led.

Three

successive years of commodity price growth (five years in the case of

oil) have generated a massive cumulative cash windfall for the region’s

largest economies. Currencies have appreciated, imports have grown, and

increased liquidity has reduced interest rates in almost every market.

In Chile and Mexico, where longer positive track records are in place,

the markets are so liquid that consumer credit is now accessible to the

majority of the population. In recovering economies like Argentina,

Brazil, Colombia and Peru, growth is only now switching gears from

export-led to domestic consumer-led.

Prudent Financial Management

What is most startling to those who have grown cynical about the region is how prudently the region’s finance ministers have managed their newfound wealth. During the commodities boom of the 1970s governments reacted to the availability of cheap money by indebting themselves even further, paving the way for the “lost decade†of the 1980s when commodity prices collapsed and foreign debt service payments ballooned. This time round, governments are paying down foreign debt, running fiscal surpluses and maintaining strict monetary policies. By reducing government’s reliance on foreign and domestic debt markets, they create more room for consumers and small business. Mexican and Chilean banks are now extending credit to the working classes and small business, igniting the growth of consumer spending in these segments for the first time in decades. Interest rates will continue to drop this year in Brazil, Argentina, Peru, Colombia and elsewhere, unleashing the long-awaited recovery of their domestic markets.

Currency Strength Drives Value-Added Imports

For foreign suppliers that are not yet established in Latin America and rely on export strategies to reach these markets, continued high (albeit slightly dampened) commodity prices offer some assurance that Latin currencies will remain strong in 2006. When the region began its export boom in 2003, its currencies remained too weak to stimulate reciprocal import growth. That situation is now changing. In spite of the expanding credit boom Latin America remains under-banked. As a result, most consumers and small business must save for a considerable period before they can afford large ticket items like cars, computers, industrial equipment and software, as well as foreign travel and education. Now that the region has been saving its dollars for three consecutive years, it is ready to spend on those most coveted large ticket items. This is good news for the Miami area, with its cost-effective export platform for value-added goods into Latin America. These exports saw record growth in 2005 and will continue through 2006 as Latin American markets catch up on previous years of under spending.

Internal Risks

This rosy picture is not devoid of risks. Within the region, electoral surprises may shake a few markets, generating unwelcome currency risks in the short term. Most notable is Peru, where Ollanta Humala has come out of the political wilderness to capture a slight lead in the polls ahead of the seasoned Lourdes Flores. Humala is already aligned with Chavez and Morales, having attended a mini-summit in Caracas when President-elect Evo Morales began his post-election international road trip. Humala would represent a major shift in a country that has been consistently friendly towards international business and has achieved currency stability thanks to massive foreign investment in its dollar-producing mining sector. Even a rhetorical anti-globalist who turns out to be a moderate could shake the normally rock-solid Sol by 10-to-15% during the campaign.

The other worrisome market, although to a lesser extent, is Mexico. It is the region’s most important economy where multinationals make most of their Latin American profits, where the peso has been stable for a decade, and where the domestic economy has been in steady expansion since 2000. Nonetheless, uncertainty lingers as the end of the Fox administration nears. Fox’s regime has been disappointing in terms of legislative leadership. But his government has held watch over an incredibly stable economy that now boasts a strong currency, a very healthy stock market, record low inflation and real wage growth.

There is a three-way race for the Presidency which is becoming increasingly difficult to predict. On the positive side, all three parties are converging on the center to sway the historically pragmatic Mexican voter. Negatively, the market is still not comfortable with how either AMLO of the PRD or Madrazo of the PRI would govern. AMLO’s views concerning the role of international business in Mexico are largely unknown. What little is known, like his strong objections to energy reform or his proposed mega-billion dollar high-speed train link to Texas, demonstrate a worrisome lack of pragmatism. Madrazo is seen as uncomfortably old-school in his way of governing. International business does not want to return to the bad old days of the PRI where graft and nepotism clouded the business climate. The election campaign will begin to take shape in the first quarter. As more information about each candidate is revealed, uneasiness in the marketplace will probably diminish, except perhaps in the event of a political gaffe by a novice like AMLO. That could send a few billion headed off-shore, and trigger some currency jitters.

Who is Leading the Political Dance?

The shift of the political pendulum to the left is now well documented. But some recent journalistic analyses are wrong in their notion that political contagion jumps from one country to the next. In reality, the influence of the media in Latin America is national, not regional. Chileans do not read Argentine papers or learn about Argentina on television, or vice-versa. In spite of the evident friendship between Evo Morales and Hugo Chavez, Bolivians voted for Morales because of Bolivian issues, not in support of a pan-regional political shift. In Latin America, like most of the world, politics is local.

The seemingly simultaneous lurch to the left in Latin America is rooted in the shift to the right in the 1990s after the previous decade’s debt crisis forced the region’s leaders to embark on the Neo-liberal experiment spoon fed by the IMF. The partially completed neo-liberal reforms across Latin America have generated results ranging from mild success (Chile and Mexico) to dismal failure in most of the Andean markets and to mixed success elsewhere. The reforms worked best where there was some degree of institutional vigilance (Chile) or where privatizations ushered in sustained foreign direct investment (Chile, Mexico, Brazil). In Bolivia, Peru, and Venezuela, foreign direct investment was less of a positive impact and many privatizations were plagued with corruption and nepotism, setting up the conditions for today’s populist political backlash.

External Risks

Latin America is home to the world’s most globalized economies, which means that it is well poised to benefit from world economic growth, as it did in 2004 and 2005, but also likely to suffer if the global economy slows. The world’s twin economic engines, the US and China, are both highly reliant on one source of growth: the US consumer. The US government, now spending more than it can tax, relies on baby boomer savings to keep it afloat. The US current account deficit presently stands at more than $600 billion, financed mainly by sales of T-Bills and stocks to the Middle East, Eastern Asia and Germany, which have prevented further devaluation of the dollar. US deficits can continue to be financed by these groups only as long as the tenuous relationships that tie them together remain in good standing. A trade dispute with China, a Mid-East led sell off of US reserves, or a collapse of housing prices could trigger a big slide in the dollar, sending interest rates higher and choking off the great US consumer. In that event China’s consumer exports would suffer and China would stop buying commodities, leaving Latin America with depleted commodity export revenue, weaker currencies and higher debt costs.

Where does Latin America stand in the global economy?

With real GDP growth forecasted at 4% for 2006, Latin America will outperform the US, Western Europe and most other developed markets but will still lag behind most emerging Asian markets and Russia. What Latin America offers over Asia is a less crowded market where market entry can still be achieved at a reasonable cost, and where competition is less fierce, leading to comparable or higher profits.

The groundbreaking Goldman Sachs analysis of the BRIC economies as the future giants in a global economy made the point that global companies must establish themselves in the world’s largest emerging markets as the economic dominance of the US and Europe continues to decline. For many companies, global coverage is not achieved by taking on a whole region but rather by taking positions in the future mega-sized economies: China, India, Brazil, Mexico, Russia, Argentina, Turkey, South Africa, Indonesia, and Thailand. These top 10 emerging markets, as opposed to the regions they are located in, are increasingly seen as sources of future growth, particularly for consumer-oriented product and service companies. Home to three of the world’s top 10 emerging markets, Latin America is rapidly becoming a strategic linchpin for any global firm.

Three

successive years of commodity price growth (five years in the case of

oil) have generated a massive cumulative cash windfall for the region’s

largest economies. Currencies have appreciated, imports have grown, and

increased liquidity has reduced interest rates in almost every market.

In Chile and Mexico, where longer positive track records are in place,

the markets are so liquid that consumer credit is now accessible to the

majority of the population. In recovering economies like Argentina,

Brazil, Colombia and Peru, growth is only now switching gears from

export-led to domestic consumer-led. Prudent Financial Management

What is most startling to those who have grown cynical about the region is how prudently the region’s finance ministers have managed their newfound wealth. During the commodities boom of the 1970s governments reacted to the availability of cheap money by indebting themselves even further, paving the way for the “lost decade†of the 1980s when commodity prices collapsed and foreign debt service payments ballooned. This time round, governments are paying down foreign debt, running fiscal surpluses and maintaining strict monetary policies. By reducing government’s reliance on foreign and domestic debt markets, they create more room for consumers and small business. Mexican and Chilean banks are now extending credit to the working classes and small business, igniting the growth of consumer spending in these segments for the first time in decades. Interest rates will continue to drop this year in Brazil, Argentina, Peru, Colombia and elsewhere, unleashing the long-awaited recovery of their domestic markets.

Currency Strength Drives Value-Added Imports

For foreign suppliers that are not yet established in Latin America and rely on export strategies to reach these markets, continued high (albeit slightly dampened) commodity prices offer some assurance that Latin currencies will remain strong in 2006. When the region began its export boom in 2003, its currencies remained too weak to stimulate reciprocal import growth. That situation is now changing. In spite of the expanding credit boom Latin America remains under-banked. As a result, most consumers and small business must save for a considerable period before they can afford large ticket items like cars, computers, industrial equipment and software, as well as foreign travel and education. Now that the region has been saving its dollars for three consecutive years, it is ready to spend on those most coveted large ticket items. This is good news for the Miami area, with its cost-effective export platform for value-added goods into Latin America. These exports saw record growth in 2005 and will continue through 2006 as Latin American markets catch up on previous years of under spending.

Internal Risks

This rosy picture is not devoid of risks. Within the region, electoral surprises may shake a few markets, generating unwelcome currency risks in the short term. Most notable is Peru, where Ollanta Humala has come out of the political wilderness to capture a slight lead in the polls ahead of the seasoned Lourdes Flores. Humala is already aligned with Chavez and Morales, having attended a mini-summit in Caracas when President-elect Evo Morales began his post-election international road trip. Humala would represent a major shift in a country that has been consistently friendly towards international business and has achieved currency stability thanks to massive foreign investment in its dollar-producing mining sector. Even a rhetorical anti-globalist who turns out to be a moderate could shake the normally rock-solid Sol by 10-to-15% during the campaign.

The other worrisome market, although to a lesser extent, is Mexico. It is the region’s most important economy where multinationals make most of their Latin American profits, where the peso has been stable for a decade, and where the domestic economy has been in steady expansion since 2000. Nonetheless, uncertainty lingers as the end of the Fox administration nears. Fox’s regime has been disappointing in terms of legislative leadership. But his government has held watch over an incredibly stable economy that now boasts a strong currency, a very healthy stock market, record low inflation and real wage growth.

There is a three-way race for the Presidency which is becoming increasingly difficult to predict. On the positive side, all three parties are converging on the center to sway the historically pragmatic Mexican voter. Negatively, the market is still not comfortable with how either AMLO of the PRD or Madrazo of the PRI would govern. AMLO’s views concerning the role of international business in Mexico are largely unknown. What little is known, like his strong objections to energy reform or his proposed mega-billion dollar high-speed train link to Texas, demonstrate a worrisome lack of pragmatism. Madrazo is seen as uncomfortably old-school in his way of governing. International business does not want to return to the bad old days of the PRI where graft and nepotism clouded the business climate. The election campaign will begin to take shape in the first quarter. As more information about each candidate is revealed, uneasiness in the marketplace will probably diminish, except perhaps in the event of a political gaffe by a novice like AMLO. That could send a few billion headed off-shore, and trigger some currency jitters.

Who is Leading the Political Dance?

The shift of the political pendulum to the left is now well documented. But some recent journalistic analyses are wrong in their notion that political contagion jumps from one country to the next. In reality, the influence of the media in Latin America is national, not regional. Chileans do not read Argentine papers or learn about Argentina on television, or vice-versa. In spite of the evident friendship between Evo Morales and Hugo Chavez, Bolivians voted for Morales because of Bolivian issues, not in support of a pan-regional political shift. In Latin America, like most of the world, politics is local.

The seemingly simultaneous lurch to the left in Latin America is rooted in the shift to the right in the 1990s after the previous decade’s debt crisis forced the region’s leaders to embark on the Neo-liberal experiment spoon fed by the IMF. The partially completed neo-liberal reforms across Latin America have generated results ranging from mild success (Chile and Mexico) to dismal failure in most of the Andean markets and to mixed success elsewhere. The reforms worked best where there was some degree of institutional vigilance (Chile) or where privatizations ushered in sustained foreign direct investment (Chile, Mexico, Brazil). In Bolivia, Peru, and Venezuela, foreign direct investment was less of a positive impact and many privatizations were plagued with corruption and nepotism, setting up the conditions for today’s populist political backlash.

External Risks

Latin America is home to the world’s most globalized economies, which means that it is well poised to benefit from world economic growth, as it did in 2004 and 2005, but also likely to suffer if the global economy slows. The world’s twin economic engines, the US and China, are both highly reliant on one source of growth: the US consumer. The US government, now spending more than it can tax, relies on baby boomer savings to keep it afloat. The US current account deficit presently stands at more than $600 billion, financed mainly by sales of T-Bills and stocks to the Middle East, Eastern Asia and Germany, which have prevented further devaluation of the dollar. US deficits can continue to be financed by these groups only as long as the tenuous relationships that tie them together remain in good standing. A trade dispute with China, a Mid-East led sell off of US reserves, or a collapse of housing prices could trigger a big slide in the dollar, sending interest rates higher and choking off the great US consumer. In that event China’s consumer exports would suffer and China would stop buying commodities, leaving Latin America with depleted commodity export revenue, weaker currencies and higher debt costs.

Where does Latin America stand in the global economy?

With real GDP growth forecasted at 4% for 2006, Latin America will outperform the US, Western Europe and most other developed markets but will still lag behind most emerging Asian markets and Russia. What Latin America offers over Asia is a less crowded market where market entry can still be achieved at a reasonable cost, and where competition is less fierce, leading to comparable or higher profits.

The groundbreaking Goldman Sachs analysis of the BRIC economies as the future giants in a global economy made the point that global companies must establish themselves in the world’s largest emerging markets as the economic dominance of the US and Europe continues to decline. For many companies, global coverage is not achieved by taking on a whole region but rather by taking positions in the future mega-sized economies: China, India, Brazil, Mexico, Russia, Argentina, Turkey, South Africa, Indonesia, and Thailand. These top 10 emerging markets, as opposed to the regions they are located in, are increasingly seen as sources of future growth, particularly for consumer-oriented product and service companies. Home to three of the world’s top 10 emerging markets, Latin America is rapidly becoming a strategic linchpin for any global firm.

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement