Disclosure: The author holds stock in companies

reviewed in this article.

Crash. Burn. Only one lone survivor made it out alive in 2008.

Before you look at the performance of location technology's public companies in 2008 you need to make sure your air bag is working properly and that a seat belt is firmly strapped around your waist. Last year saw every public company take a whipping in the stock market, except one. A worldwide collapse of the financial markets did not spare location technology and the result was a drastic plummet in stock prices and investor wealth. It was a year that made all initial predictions of potential gains look foolish.

This year's analysis includes some changes to the industry categories in which each company is analyzed. The changes may reflect acquisitions that occurred within the last 12 to 18 months. Autodesk, Pitney Bowes and Trimble are now grouped into the Enterprise Geospatial Technology segment. New to that segment is Hexagon, owner of ERDAS and Leica Geosystems, and subsidiaries that sell geospatial technology. Descartes and ClickSoftware are included in the Geospatial Application group. ClickSoftware, a new addition, gains its competitive advantage from geocoding, routing and map display, as does Descartes. Having acquired Tele Atlas, TomTom is grouped with Garmin into Portable Navigation Device Manufacturers. Nokia joins the list after acquiring NAVTEQ. Nokia, with so many lines of business and just a toe in location technology, falls in with the large enterprise technology companies, including Microsoft and Oracle. GeoEye and Intermap Technologies remain in the Geospatial Data company group. Openwave, InfoSpace and TeleCommunications Systems Inc. remain in the Location-based Systems (LBS) Company category.

All of the charts included in this analysis, with the exception of Figure 1, show a 12-month timeline for each stock's percentage gain or loss with respect to its opening share price on January 1, 2008.

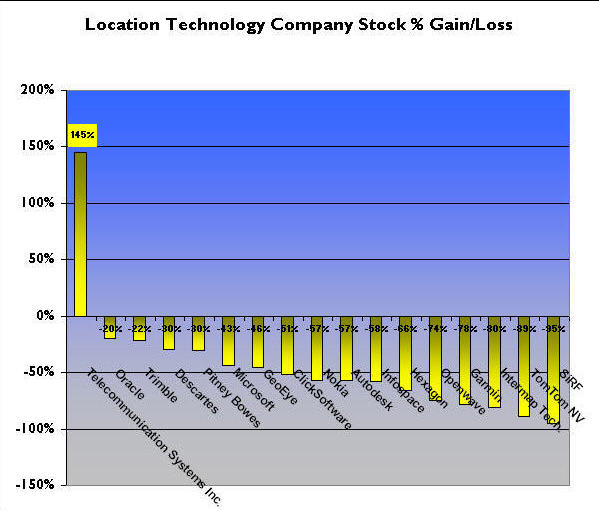

Figure 1 shows the rather discouraging news of 2008 – a compilation of each stock's performance for the year. Oracle's 20% drop in stock price looks modest when compared with SiRF Technology's 95% drop in value. And the lone survivor? TeleCommunications Systems Inc. rallied to a 145% gain due to increased volume of text messaging and its E911 solutions. The reasons behind the bloodletting of the other public stocks in our analysis require a more thorough examination. Why did some merely slump, versus those that really tanked? Let's look at those reasons.

Enterprise Geospatial Technology

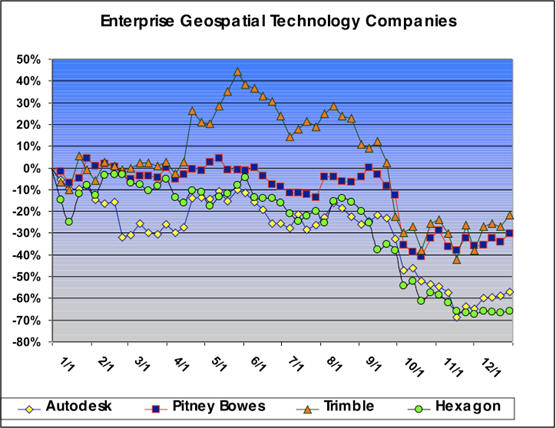

In this sector, each company should be evaluated with respect to the broader industries it serves. Figure 2 below shows this segment's performance for 2008 and is representative of the malaise that every other sector experienced. Pitney Bowes (PBI) is an outlier in this group in that its core business is not geospatially connected. PBI, a company with $6 billion in revenue, primarily serves the mailstream market, from which it generates approximately $4 billion of that total revenue. The PB Business Insight division now includes the PB MapInfo business unit, providing a small part of the company's overall revenue. MapInfo was a part of PB's revenue for its first full year in 2008. (PB acquired MapInfo in March 2007.) The 30% decline in stock value is relatively shallow due to the cash flow strength of its mailstream business.

For Autodesk (ADSK), losing over 50% in value was a sign that it wasn't spared the anxiety of investors even though it generally showed solid growth with good management. Last week's news that it was cutting 10% of its workforce was another indication that the company is preparing for a year of uncertainty, even with the possibility that the economic stimulus package suggested by the incoming U.S. administration would impact its business positively. The company announced, in a recent statement, that it is writing down goodwill to its Media and Entertainment business and spinning off its Location Services unit, which had a large contract with Verizon Wireless. Autodesk did not feel that the Location Services unit of the company was in line with its core business.

Trimble (TRMB) finished 2008 with only a 22% decline in its value. Coming off a 19% gain in 2007, Trimble had added considerably to its gains by mid-2008, rising over 40% in value before the fall swoon. The stock looked like it was on the road to recovery by year's end, perhaps buoyed by announcements that the stimulus package would be directed at infrastructure projects. And then, just last week, it revised its fourth quarter guidance. "The drop in demand has been concentrated in the Engineering and Construction segment. Our revenue from agricultural products continued to grow at double-digit levels in the fourth quarter. The Mobile Solutions segment's order pipeline continues to be resilient. We also believe the launch of new products, new ventures and new lines of business will positively contribute to 2009 results and set the stage for additional growth as the economy stabilizes," said President and CEO Steve Berglund. The company's stock has already dropped 33% in 2009.

Hexagon (HEXAB:SS) experienced a drop in value throughout 2008 and ended the year down steeply with a decline in value of 67%, but still grew earnings per share of six to eight cents per share according to a recent statement released by the company. As the parent company that purchased Leica Geosystems Geospatial Imaging (image processing and GIS solutions), now ERDAS, as well as Leica Geosystems (GPS and sensor equipment), Hexagon is a multinational, diversified corporation with a specialty in measurement equipment. But it expects to accelerate a cost reduction program and incur layoffs in the first half of 2009.

Geospatial Data Companies

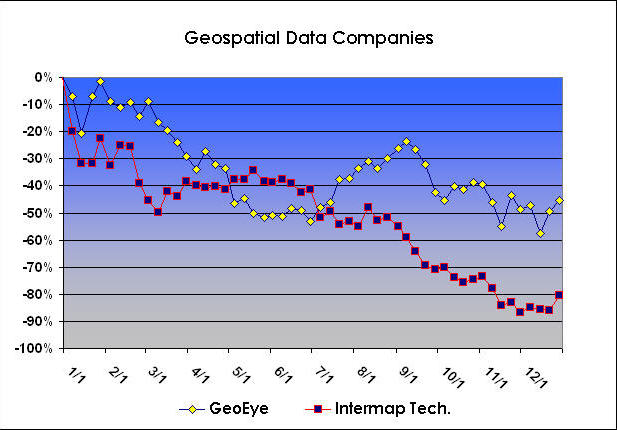

The high flyers of 2007, Geospatial Data companies could not maintain their momentum in 2008. Intermap Technologies (TSE:IMP) reversed a rise of 75% in value in 2007 with an 80% drop in value in 2008. Some of IMP's major customers are in the automotive and personal navigation industries. This is contributing to investor worries about the company's ability to maintain its revenue growth. But IMP is a data collector and lies at the crux of the geospatial food chain along with other data suppliers like DigitalGlobe and GeoEye. It is engaged in data collection around the world, in particular in its capture of 3D terrain models. With the emphasis on 3D sure to continue, IMP appears to be positioned for growth once the economy improves.

Despite launching GeoEye-1 on September 6, 2008 after many delays, GeoEye (GEOY) followed the rest of the market into negative territory with a 46% drop in value. With the highest spatial resolution satellite in orbit, a contract with Google to supply it with imagery, and plans already in the works for GeoEye-2, it stands as one of only two remaining U.S. satellite image providers. In a presentation (PDF) made to investors late last year, the company revealed a 53.5% compound annual growth rate (CAGR) through 2007, but had to acknowledge income tax accounting miscues which the company said are being addressed. Despite its drop in value in 2008, the stock stands at relatively the same price seen in early 2007 and appears to maintain a price support level at around $17 per share.

LBS Companies

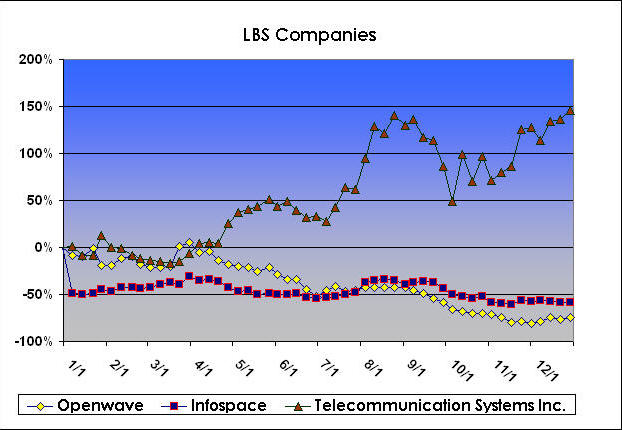

Openwave (OPWV) is a company trying to position itself at the intersection of the Internet and broadband mobile service, which includes location-based services. It's hard to do this when all around you the world is still trying to figure out if mobile Internet is a useful service for which people are willing to pay. Eventually the market will understand its virtues, but during these times, mobile Internet seems to be a luxury for the average person. Converged devices are the key for Openwave and the company is still waiting for the boom to hit. Down 74% in 2008 after a precipitous 66% drop in 2007, you may reasonably wonder if this company will survive.

After the huge dividend payouts in 2007, InfoSpace (INSP), a company mostly offering local search solutions, kept a relatively low profile in 2008 despite finishing down 58%. In fact the news was rosy, as the company reported a 17% increase in revenue when it revealed third quarter results last November. "Our strong operating results in the third quarter were driven by growth in both our owned and operated and distribution businesses," said Jim Voelker, chairman and CEO. "Based on the success we've seen in driving traffic to our sites in both the second and third quarters, we will continue to invest in marketing programs for our flagship search site Dogpile.com. We are pleased with our progress and performance this year and are confident in our ability to continue this success despite the challenges in the macroeconomic environment." The company, however, is now being sued by a stockholder alleging improper payments relating to the dividend payouts (as reported in the Seattle Post Intelligencer).

Telecommunications Systems Inc. (TSYS) defied all macroeconomic conditions and posted a 145% gain in value in 2008, which followed a 15% gain in 2007. The company, according to an investor presentation (PDF) last November, expects to continue its 13% CAGR when it reports full year earnings in February. Its business in the VoIP, text messaging, LBS and military markets is fueling the company's growth and is not expected to abate. This diversification in a relatively hot market positions TSYS to have another growth year in stock value for the company.

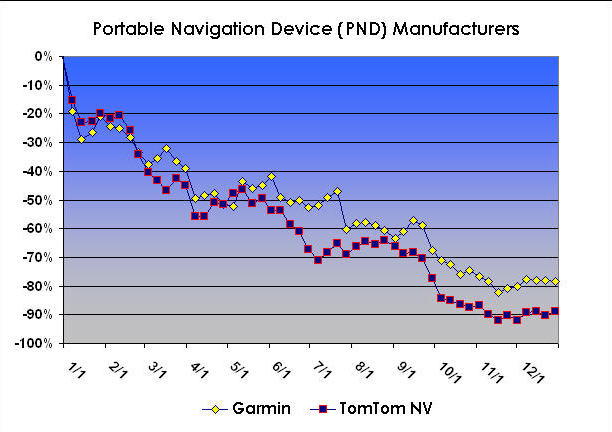

Portable Navigation Device Manufacturers

Sink. Sank. Sunk. The bottom fell out of the portable navigation device (PND) market in 2008. Competition from low-priced foreign manufacturers, as well as alternatives from cellular providers, stung both Garmin (GRMN) and TomTom (TMOAF.PK). In its third quarter 10Q report, Garmin saw sales increases in both outdoor and automotive segments of its business. However, in that report, the company stated, "Gross profit margin percentage for the Company overall decreased primarily as a result of the automotive/mobile segment remaining a significantly larger percentage of the Company's product mix." In its third quarter outlook, TomTom informed investors that it expects demand for PNDs to grow but at a slower pace, with both European and North American markets each to buy 18 million units - down from projected sales of 20 million units. Look for both companies to make headway into the connected navigation device market in 2009.

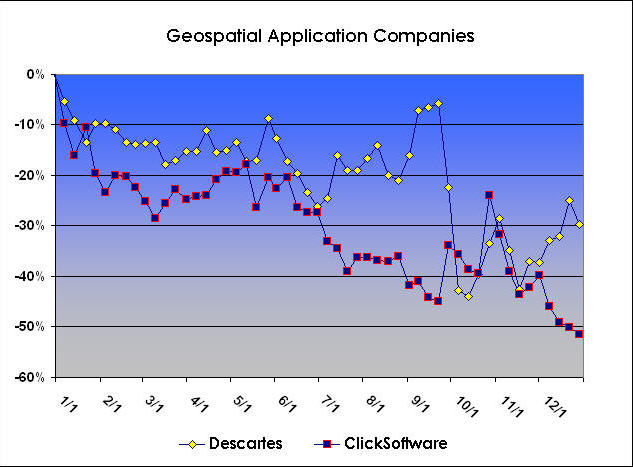

Geospatial Applications

Descartes (DSGX) declined 30% for 2008 but in December announced plans to buy back approximately 10% of its outstanding shares. Descartes' software as a service (SaaS) logistics solutions appear to be well positioned in this market where cost savings are sought. In its third quarter report, revenue and profits were up 10% and 50%, respectively, from Q3 one year ago.

ClickSoftware (CLKS), another company engaged in workforce planning and optimized scheduling that looks to support clients with cost saving solutions, declined over 50% in value in 2008. However, in its third quarter report, the company announced record revenues and profits, stating: "As previously announced on October 2, 2008, the Company currently expects to achieve annual revenues in the range of approximately $52 to $54 million dollars, exceeding the annual guidance of $48 to $50 million given at the beginning of the year. This will bring the year-over-year growth to the approximate range of 30% to 35%." Dr. Moshe BenBassat, ClickSoftware's chairman and CEO, also stated that given the current global economic situation, "We are closely monitoring our pipeline and short-term prospects. We have good visibility into the coming quarter and are excited by the long-term prospects of ClickSoftware."

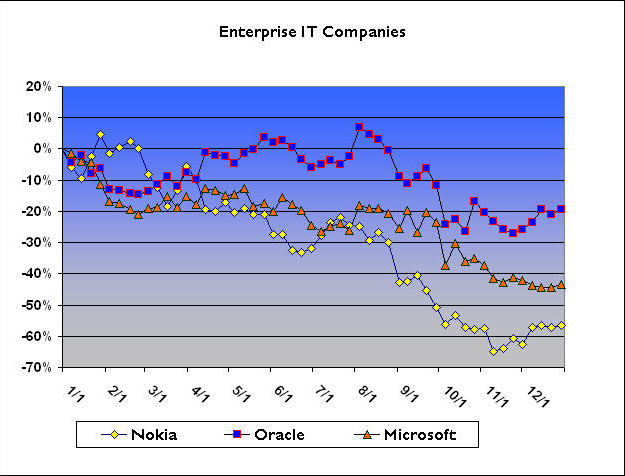

Enterprise IT Companies

It's useful to include these selected enterprise information technology (IT) companies in this report for a somewhat broader perspective on the overall IT market. No one was spared, despite generally good earnings. Remember, the stock market is a leading economic indicator so the drop in stock price is often a reflection of an anticipated drop in company performance. For the year, Microsoft (MSFT), Oracle (ORCL) and Nokia (NOK) all fell in value. All have invested heavily in location technology, especially Nokia with the purchase of NAVTEQ, which closed on July 10, 2008. And all are expected to continue with product enhancements that include geospatial technology. Microsoft continues to improve Virtual Earth, announced support of spatial data primitives in the newest version of SQL Server, and also released MapPoint 2009 last year. Oracle continues to win converts to Oracle Spatial, and Nokia plans to leverage NAVTEQ's investment in geospatial data in applications from location-based social networks to advertising.

Summary

While 2009 looks gloomy from this perspective, we are all holding our breath in hopes that global financial markets will stabilize and location technology will grow. It is not a luxury IT expense. It is a technology that will support infrastructure investment and consumer services. It will support both cost savings and revenue enhancement. From the individual reports of most of the companies in this analysis, few believed that prospects would not pick up in 2009. It's not a matter of if, but when, the market turns for the location technology IT sector.

Crash. Burn. Only one lone survivor made it out alive in 2008.

Before you look at the performance of location technology's public companies in 2008 you need to make sure your air bag is working properly and that a seat belt is firmly strapped around your waist. Last year saw every public company take a whipping in the stock market, except one. A worldwide collapse of the financial markets did not spare location technology and the result was a drastic plummet in stock prices and investor wealth. It was a year that made all initial predictions of potential gains look foolish.

This year's analysis includes some changes to the industry categories in which each company is analyzed. The changes may reflect acquisitions that occurred within the last 12 to 18 months. Autodesk, Pitney Bowes and Trimble are now grouped into the Enterprise Geospatial Technology segment. New to that segment is Hexagon, owner of ERDAS and Leica Geosystems, and subsidiaries that sell geospatial technology. Descartes and ClickSoftware are included in the Geospatial Application group. ClickSoftware, a new addition, gains its competitive advantage from geocoding, routing and map display, as does Descartes. Having acquired Tele Atlas, TomTom is grouped with Garmin into Portable Navigation Device Manufacturers. Nokia joins the list after acquiring NAVTEQ. Nokia, with so many lines of business and just a toe in location technology, falls in with the large enterprise technology companies, including Microsoft and Oracle. GeoEye and Intermap Technologies remain in the Geospatial Data company group. Openwave, InfoSpace and TeleCommunications Systems Inc. remain in the Location-based Systems (LBS) Company category.

All of the charts included in this analysis, with the exception of Figure 1, show a 12-month timeline for each stock's percentage gain or loss with respect to its opening share price on January 1, 2008.

Figure 1 shows the rather discouraging news of 2008 – a compilation of each stock's performance for the year. Oracle's 20% drop in stock price looks modest when compared with SiRF Technology's 95% drop in value. And the lone survivor? TeleCommunications Systems Inc. rallied to a 145% gain due to increased volume of text messaging and its E911 solutions. The reasons behind the bloodletting of the other public stocks in our analysis require a more thorough examination. Why did some merely slump, versus those that really tanked? Let's look at those reasons.

|

In this sector, each company should be evaluated with respect to the broader industries it serves. Figure 2 below shows this segment's performance for 2008 and is representative of the malaise that every other sector experienced. Pitney Bowes (PBI) is an outlier in this group in that its core business is not geospatially connected. PBI, a company with $6 billion in revenue, primarily serves the mailstream market, from which it generates approximately $4 billion of that total revenue. The PB Business Insight division now includes the PB MapInfo business unit, providing a small part of the company's overall revenue. MapInfo was a part of PB's revenue for its first full year in 2008. (PB acquired MapInfo in March 2007.) The 30% decline in stock value is relatively shallow due to the cash flow strength of its mailstream business.

For Autodesk (ADSK), losing over 50% in value was a sign that it wasn't spared the anxiety of investors even though it generally showed solid growth with good management. Last week's news that it was cutting 10% of its workforce was another indication that the company is preparing for a year of uncertainty, even with the possibility that the economic stimulus package suggested by the incoming U.S. administration would impact its business positively. The company announced, in a recent statement, that it is writing down goodwill to its Media and Entertainment business and spinning off its Location Services unit, which had a large contract with Verizon Wireless. Autodesk did not feel that the Location Services unit of the company was in line with its core business.

Trimble (TRMB) finished 2008 with only a 22% decline in its value. Coming off a 19% gain in 2007, Trimble had added considerably to its gains by mid-2008, rising over 40% in value before the fall swoon. The stock looked like it was on the road to recovery by year's end, perhaps buoyed by announcements that the stimulus package would be directed at infrastructure projects. And then, just last week, it revised its fourth quarter guidance. "The drop in demand has been concentrated in the Engineering and Construction segment. Our revenue from agricultural products continued to grow at double-digit levels in the fourth quarter. The Mobile Solutions segment's order pipeline continues to be resilient. We also believe the launch of new products, new ventures and new lines of business will positively contribute to 2009 results and set the stage for additional growth as the economy stabilizes," said President and CEO Steve Berglund. The company's stock has already dropped 33% in 2009.

Hexagon (HEXAB:SS) experienced a drop in value throughout 2008 and ended the year down steeply with a decline in value of 67%, but still grew earnings per share of six to eight cents per share according to a recent statement released by the company. As the parent company that purchased Leica Geosystems Geospatial Imaging (image processing and GIS solutions), now ERDAS, as well as Leica Geosystems (GPS and sensor equipment), Hexagon is a multinational, diversified corporation with a specialty in measurement equipment. But it expects to accelerate a cost reduction program and incur layoffs in the first half of 2009.

|

Geospatial Data Companies

The high flyers of 2007, Geospatial Data companies could not maintain their momentum in 2008. Intermap Technologies (TSE:IMP) reversed a rise of 75% in value in 2007 with an 80% drop in value in 2008. Some of IMP's major customers are in the automotive and personal navigation industries. This is contributing to investor worries about the company's ability to maintain its revenue growth. But IMP is a data collector and lies at the crux of the geospatial food chain along with other data suppliers like DigitalGlobe and GeoEye. It is engaged in data collection around the world, in particular in its capture of 3D terrain models. With the emphasis on 3D sure to continue, IMP appears to be positioned for growth once the economy improves.

Despite launching GeoEye-1 on September 6, 2008 after many delays, GeoEye (GEOY) followed the rest of the market into negative territory with a 46% drop in value. With the highest spatial resolution satellite in orbit, a contract with Google to supply it with imagery, and plans already in the works for GeoEye-2, it stands as one of only two remaining U.S. satellite image providers. In a presentation (PDF) made to investors late last year, the company revealed a 53.5% compound annual growth rate (CAGR) through 2007, but had to acknowledge income tax accounting miscues which the company said are being addressed. Despite its drop in value in 2008, the stock stands at relatively the same price seen in early 2007 and appears to maintain a price support level at around $17 per share.

|

LBS Companies

Openwave (OPWV) is a company trying to position itself at the intersection of the Internet and broadband mobile service, which includes location-based services. It's hard to do this when all around you the world is still trying to figure out if mobile Internet is a useful service for which people are willing to pay. Eventually the market will understand its virtues, but during these times, mobile Internet seems to be a luxury for the average person. Converged devices are the key for Openwave and the company is still waiting for the boom to hit. Down 74% in 2008 after a precipitous 66% drop in 2007, you may reasonably wonder if this company will survive.

After the huge dividend payouts in 2007, InfoSpace (INSP), a company mostly offering local search solutions, kept a relatively low profile in 2008 despite finishing down 58%. In fact the news was rosy, as the company reported a 17% increase in revenue when it revealed third quarter results last November. "Our strong operating results in the third quarter were driven by growth in both our owned and operated and distribution businesses," said Jim Voelker, chairman and CEO. "Based on the success we've seen in driving traffic to our sites in both the second and third quarters, we will continue to invest in marketing programs for our flagship search site Dogpile.com. We are pleased with our progress and performance this year and are confident in our ability to continue this success despite the challenges in the macroeconomic environment." The company, however, is now being sued by a stockholder alleging improper payments relating to the dividend payouts (as reported in the Seattle Post Intelligencer).

Telecommunications Systems Inc. (TSYS) defied all macroeconomic conditions and posted a 145% gain in value in 2008, which followed a 15% gain in 2007. The company, according to an investor presentation (PDF) last November, expects to continue its 13% CAGR when it reports full year earnings in February. Its business in the VoIP, text messaging, LBS and military markets is fueling the company's growth and is not expected to abate. This diversification in a relatively hot market positions TSYS to have another growth year in stock value for the company.

|

Sink. Sank. Sunk. The bottom fell out of the portable navigation device (PND) market in 2008. Competition from low-priced foreign manufacturers, as well as alternatives from cellular providers, stung both Garmin (GRMN) and TomTom (TMOAF.PK). In its third quarter 10Q report, Garmin saw sales increases in both outdoor and automotive segments of its business. However, in that report, the company stated, "Gross profit margin percentage for the Company overall decreased primarily as a result of the automotive/mobile segment remaining a significantly larger percentage of the Company's product mix." In its third quarter outlook, TomTom informed investors that it expects demand for PNDs to grow but at a slower pace, with both European and North American markets each to buy 18 million units - down from projected sales of 20 million units. Look for both companies to make headway into the connected navigation device market in 2009.

|

Descartes (DSGX) declined 30% for 2008 but in December announced plans to buy back approximately 10% of its outstanding shares. Descartes' software as a service (SaaS) logistics solutions appear to be well positioned in this market where cost savings are sought. In its third quarter report, revenue and profits were up 10% and 50%, respectively, from Q3 one year ago.

ClickSoftware (CLKS), another company engaged in workforce planning and optimized scheduling that looks to support clients with cost saving solutions, declined over 50% in value in 2008. However, in its third quarter report, the company announced record revenues and profits, stating: "As previously announced on October 2, 2008, the Company currently expects to achieve annual revenues in the range of approximately $52 to $54 million dollars, exceeding the annual guidance of $48 to $50 million given at the beginning of the year. This will bring the year-over-year growth to the approximate range of 30% to 35%." Dr. Moshe BenBassat, ClickSoftware's chairman and CEO, also stated that given the current global economic situation, "We are closely monitoring our pipeline and short-term prospects. We have good visibility into the coming quarter and are excited by the long-term prospects of ClickSoftware."

|

It's useful to include these selected enterprise information technology (IT) companies in this report for a somewhat broader perspective on the overall IT market. No one was spared, despite generally good earnings. Remember, the stock market is a leading economic indicator so the drop in stock price is often a reflection of an anticipated drop in company performance. For the year, Microsoft (MSFT), Oracle (ORCL) and Nokia (NOK) all fell in value. All have invested heavily in location technology, especially Nokia with the purchase of NAVTEQ, which closed on July 10, 2008. And all are expected to continue with product enhancements that include geospatial technology. Microsoft continues to improve Virtual Earth, announced support of spatial data primitives in the newest version of SQL Server, and also released MapPoint 2009 last year. Oracle continues to win converts to Oracle Spatial, and Nokia plans to leverage NAVTEQ's investment in geospatial data in applications from location-based social networks to advertising.

|

Summary

While 2009 looks gloomy from this perspective, we are all holding our breath in hopes that global financial markets will stabilize and location technology will grow. It is not a luxury IT expense. It is a technology that will support infrastructure investment and consumer services. It will support both cost savings and revenue enhancement. From the individual reports of most of the companies in this analysis, few believed that prospects would not pick up in 2009. It's not a matter of if, but when, the market turns for the location technology IT sector.

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement