Plenary Sessions:

Top 10 Predictions for the Energy Industry in 2005

A Blueprint for the Next Decade

The Next Frontier: Conquering the Digital Home

Tracks:

Applications and Transformations

Software Companies of the Future

Redefining the Software Value Equation

Mobile in Your World

Mobile Life: How Mobility is Impacting Personal and Professional Lives

Revolutionizing Wireless Again with Consumer Multimedia

Mobility's Measured March into the Enterprise

Keynote:

Geoffrey Moore on the Next Decade

Introduction

IDC held its Directions '05 (we like the name!) conference in Boston on March 16.The annual one-day conference aims to outline the future of IT.Hal Reid (HR) and Adena Schutzberg (ABS) attended and agreed it was most valuable to "pull our heads out of GIS" and take a step back into the broader world of IT.We share IDC's analysts' take on industry IT and communications topics and our reactions.

Top 10 Predictions for the Energy Industry in 2005 (HR)

|

Rich Nicholson, Vice President, Energy Insights, an IDC Company, discussed several areas that were driving the outlook for 2005.These included commodity prices (March 16th saw oil above $55 a barrel) and the financial health of the entire energy industry.His 10 predictions for 2005 included:

1.An increase in mergers and acquisitions

2.Utilities getting serious about Business Process Outsourcing

3.Capital will flow to alternative and renewable energy technologies

4.Energy companies will re-deploy capital and resources to better integrate, Geology, Geophysics and Engineering (the digital, interactive oilfield)

5.The resumption of energy trading (post Enron age of trading)

6.A new focus on operational efficiency and regulatory compliance

7.An increase in retail investment, including outsourcing of customer care and billing (see number 2).

8.First prototypes and pilots of Intelligent Grid technology, full scale implementation is still years away.

9.Energy and Telcom convergence with limited success.Continued interest in broadband over power lines, lots of resistance here, including expertise, RF interference, etc.

10.U.S energy spending will exceed $22B in 2005.

The opportunities for IT in this arena were in creating greater efficiencies and in linking to the business process outsource resources.Mergers and acquisitions required infrastructure consolidation which could provide opportunities to move beyond legacy systems.Perhaps the 11th prediction that came out of this session was that the CIO would be in the spotlight.A wise man once noted that the spotlight could very quickly become the heat lamp.

A Blueprint for the Next Decade (ABS)

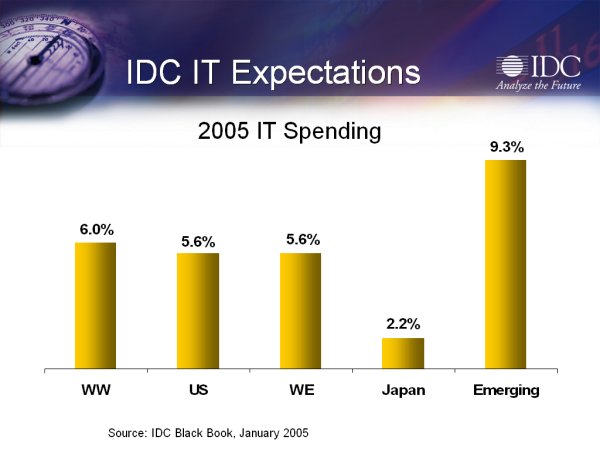

The day opened with a session that described a "Blueprint for the Next Decade." John Gantz, Senior Vice President and Chief Research Officer, IDC started with the past: in the past 10 years the number of Internet users went from basically 0 to 1 billion.He moved to the present: the present state of the economy is good and CIOs are generally bullish on ITC spending.(Information Technology and Communications, from IDC's perspective, are all merging together.) Worldwide IT growth is at 6% with worldwide communications services growth at 4.9%.Still, those in the industry should be too blasé, argued Gantz, because "there's a high probability of a low probability event that might shake things up."

|

With that base Gantz addressed transformations going on in the world that will help direct the future including:

China - China's move into the world economy means that IT supply and demand is moving westward.Note to students: learn Chinese!

Telephony - VOIP is becoming real.Mobile device users.who number less than 1 billion today, will number more than 5 billion in ten years.And, anything can be used as a phone.The reverse is true too: a phone might be used as something else, too, such as a wallet to pay for a soda.

Broadband - Broadband use is rising.The 600 million households using broadband in ten years will drive up the number of transactions on the Web significantly from today's numbers.

Digital - Both TV and radio are becoming digital and perhaps interactive.It's that interactive payload that will drive change.Even today, some Internet Service Providers report that one third of bandwidth is used by BitTorrent and other "two way" data sharing technologies.

ITC Blanket - The earth is now blanketed with ITC devices - be they RFID chips, GPS, security cameras, WiFi, or others in and outdoors, and in our vehicles.

What may just come out of all this? Perhaps, Gantz offer, it's a huge jump the number of "touchpoints," the number of commercial transactions on the Internet.Exactly how ITC players will manage that jump is unclear.But Gantz sees the jump as something that will accompany the development of the "invisible computing era." Devices will be smaller and embedded.The fact that communications or transactions occurs over the Internet will be pushed further and further from the actual experience of the user.Thus, "invisible" computing!

The challenge, says Gantz is to see the future and react.That will divide the DECs and Computerlands (who lost to the PC industry in general and Dell in particular, respectively, by not changing) from the IBMs and Microsofts of the world (who won by changing).

The Next Frontier: Conquering the Digital Home (HR)

Danielle Levitas, Vice President, Consumer and Broadband Markets, IDC, began with the fact that current consumer spending is reaching close to 70% of the U.S.GDP which in turn means that companies are focusing on consumers.Broadband and networking, digital TV and technology miniaturization are the targets of this spending.To effectively address this market, vendors need to better understand consumers.Much of this presentation (and others during the day) were standard marketing points revolving around the theme of the need to understand the consumer.

|

Why do consumers use technology?

• Control - e.g.what to watch on TV and when - TIVO

• Community - e.g.contact with friends, family regardless of location - Cell Phones

• Convenience - e.g.instant access to information, - the Internet

• Choice & Customization - e.g.ring tones,

• Content - e.g.Multi-media messaging, video

Companies need to be aware that technology is moving faster than consumers can absorb and understand it.Said another way: the wide range of products and services offered may be solving problems consumers don't know they have.The challenge of purchasing a TV (digital or not, high definition or not, etc.) was offered as an example.

The key advice for companies was, simplify, make the products and services easy to use (setting your VCR's clock is where this has failed), and make the user interface as intuitive as possible.Service providers need to bear this in mind, too.Levitas pointed out that the consumer may not yet see the difference products and service providers.The key takeaway quote was "It's a world where technology adapts to people, versus people adapting to technology".

Applications and Transformations (ABS)

Software Companies of the Future

|

Tony Picardi, Senior Vice President, Software, IDC, outlined a thesis that software companies of the future would include a new type of player, a "software broker." These brokers are needed to address the complexity of the current software market.That complexity means that it's too complicated (too expensive) for organizations to do simple things.Instead, they must spend time (and money) to install bug fixes, build portals, add applications, manage licenses, etc.The brokers would do all that work on behalf of the ultimate software customer.

In ten years, Picardi offered, brokers will "own" the customers and will in turn be the main customers of the software publishers.The brokers will manage licenses, certify implementations, test new protocols, solve problems, recommend innovation and create intelligence through integration...That sounded to me like today's integrators.The difference? Integrators do one off work and move on the next project.Brokers will focus on one domain and act as "partners for life" with the customer.

He highlighted some potential brokers of the future: IBM, SAP, Oracle, Microsoft, Sage, Intuit and down at the consumer level Apple, whose iPod (which integrates hardware and software) and Amazon (which certainly solves complexity).He offered that it's time for software vendors and integrators to decide the role they want to play in the future.

While I concur that there is a complexity crisis, I'm not sure this will be the way it's solved.Why won't today's integrators slip into that role instead of these powerhouses of development and services taking on the role? And, might the software producers finally address these issues so that users can manage without a broker? I was not the only skeptical one, those sitting around me noted "we don't buy it!"

Redefining the Software Value Equation

|

Today's challenge, said Amy Kontary, is that there is a disconnect between the customer's price and acquisition experience and the perceived value of software.

Customers feel that they are forced to buy more software than they use.She offered that customers cite using 16% of what is purchased.And, while vendors may discount, that doesn't seem to help balance the price vs.value situation.Customers are quite savvy - they are aware that they need to explore a software investment in the context of new technologies (like grid computing), they are aware of "pay per use" options, they've run into software as a service, open source, subscriptions and other options.Customers feel that licensing is inconsistent and complex and that vendors propose pricing that attempts to match what they think the customer will pay.

Vendors see things a bit differently.They realize that price pressures are forcing them to reassess their pricing and licensing structures.Licensing, from the vendor standpoint, is identified as a key differentiator in the marketplace today.Vendors report they often feel they are leaving money on the table.

To illustrate the value of product, Kontary shared a story.Before leaving for her honeymoon trip to New Zealand, she bought a digital camera that also shot movies.The goal was to film her new husband's bungie jump.She studied the manual on the plane and when the big jump happened, she was unable to film it (Lucikly, the bungie company filmed it and offered a very expensive VHS tape of the event, which the couple did purchase.) The camera was returned once the couple returned to the States.While the camera had value, it did not deliver the successful experience the buyer required.So, in effect, its value to Kontary was zero.

With that in mind she offered a new model for software pricing, one that defined value on customer/vendor interaction and one which focused on the product's ease of use and the user's success with it.What customers want (and this harkens back to the camera) is access to experience (what the vendor typically has).It's the vendor's role to put more focus on experience and how to make the customer successful.That means a stronger, more balanced dialog with the user, it means enhanced transparency when it comes to pricing and it means enhanced access to the vendor by the customer.Licensing, Kontary noted, won't go away, but more clever methods (like volume licensing and pay per use) may well simplify agreements and reduce costs.

Mobile in Your World (HR)

Mobile Life: How Mobility is Impacting Personal and Professional Lives

|

Randy Giusto, Group Vice President, Personal Technology and Services identified the differences between the Mobile Worker and the Mobile Consumer.Each one had four segments:

Mobile Workers Segments

• Display Mavens - High end graphics users

• Mobile Elite - early adopters, want latest & greatest

• Voice & Tex Maniacs - SMS, IM, Communicators

• Minimalists - No frills, simple is good

Consumer Segments

• Fast Trackers - DINKs, high income, image is important

• Techno Tribes - Families, kids very techno savvy, lots of tech

• Quintessentials - Empty nesters, tech savvy, but ease of use important

• Mainstream - Tech takes a backseat to everything else.

As these groups converge, IT vendors are challenged to determine the levels of expectations of each segment.Restraint by IT and the efforts to prescribe mobile hardware are not well received by the mobile worker segments.User expectations included not just mobile email and messaging, but elements of location-based services (LBS) and mobilized back office applications so that information was available all the time from anyplace.

Revolutionizing Wireless Again with Consumer Multimedia

|

Scott Ellison, Program Director, Wireless & Mobile Communications, IDC suggested that wireless will be revitalized and expanded through the introduction of multimedia, (TV, video, music, etc.to the cell phone), for both consumers and mobile workers.3G wireless networks and enhanced speed of applications make these services more viable and marketable.Wireless will be the universal communicator merging data, remote storage (phone to the network) and be the 3rd screen in the user's life, after the TV and the computer.

These changes require fundamental shifts in telco thinking about the need to merge a lot of IT functions into wireless technology.Concepts as per-use billing as opposed to flat rates are challenging the industry.The traditional telco approach to billing is proving obsolete.Because cost is an issue in expanding a market, the relationships between telco technology, user interfaces (delivery of services) and pricing structures make the revolution more difficult than it has to be.There is a market of willing consumers and willing vendors.The missing piece of the puzzle is a better space in between.

Mobility's Measured March into the Enterprise

|

Kevin Burden, Research manager, Mobile Devices, IDC explored the measured march of mobility into the enterprise.He suggested the slow movement is due in part to the resistance of IT.IT managers face the dilemma of prescribing devices, managing access, and controlling costs along with following the priorities set by the command structure within the enterprise.Mobile worker productivity increases when companies move beyond mobile email as the method to access information.Doing reports and using LBS may require job re-tooling and workflow changes that were not envisioned with the initial roll-out of mobile technology and may create new challenges.

Mobile is not always defined as wireless.Mobile may also address the larger problem of the mobile worker, the virtual office and the telecommuter.As a result, with advances and changes brought on by mobile technology, that mobile technology will be introduced through the "back door" by people outside of IT who need to solve a business problem.

The dichotomy is in the desires of the enterprise and the individual.

The enterprise wants:

• A real keyboard for data intensive applications

• Broad application support, e-mail and PIMs

• A world phone

• Security

• A manageable device (hope says one device, reality says two)

The individual wants:

• The device, system, etc., to improve the quality of life

• One device for communication

• Newness and coolness

• Minimal pain

The reality is:

• Mobility in the enterprise inevitable

• While the enterprise realizes the inevitability, enterprise IT needs to be the driver and manager

• Enterprise and individual devices will continue to diverge.That is, enterprise devices move avay from consumer devices and vice versa.

• Enterprise mobility is complex

Geoffrey Moore on the Next Decade (ABS)

|

Author and businessman Geoffrey Moore (Crossing the Chasm and others) ended the day with a keynote.In his "Blueprint for the Next Decade" he redefined the battle taking place in the marketplace around the "IT stack," that is the layers required in an enterprise architecture.The battle is being driven, he argued, by three key things: system oriented architectures (SOAs), globalization and outsourcing.These all "push" on the interoperability in the stack, which creates an instability and can allow some rearranging of the players.The companies that succeed will grab onto and own one or more layers in the stack.

The "gorillas," aka the big winners will be those who marginalize the smaller players (chimps and monkeys) and transform their layer(s) in the stack into platforms.Moore walked through eight key players to identify the layers they "own" now and those they might target.(This vision gave me a new perspective on IBM's recent acquisition of Ascential and the current plays by Oracle and SAP over Retek.) IBM, for example, owns consulting and mainframes.It might move into several others.SAP owns transaction applications but might look at analytical applications and application server infrastructure.Microsoft owns the operating system (Windows) and collaborative applications (Office) and has many targets.Of the eight, he praised the strategies of these three and along with Oracle, EMC and Cisco.He was less confident about the futures of SUN and HP.

Some of the gorillas, he noted are well entrenched, but in the near future that stability will be disrupted by SOAs and cause a new set of platforms to be born.That means that the marketplace will need to define the stable layers, determine if the platform architecture makes sense and spit out some winners and losers.