The

average consumer now has many choices of navigation and GPS-enabled

tools. There are onboard navigation systems, off-the-shelf personal

navigation devices, and navigation applications available on cell

phones or smart phones. Do the availability and use of navigation and

tracking tools in the consumer space, as well as the broader cost and

productivity ramifications associated with real-time tracking,

scheduling and navigation, support significantly high adoption rates in

the enterprise space as well?

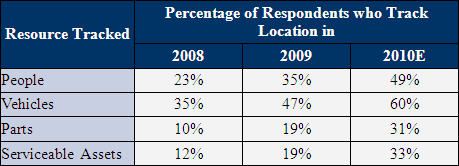

In a recent research survey of field service and manufacturing organizations conducted by Aberdeen, with the support of Directions Media, Wireless Matrix, Intergis and GPS Insight, only 35% of responding firms indicated that they currently track the whereabouts of their field technicians, with 47% indicating that they track the location of their service vehicles with the help of GPS technology. Just 19% of firms indicated that they actively track resources, such as parts and serviceable assets.

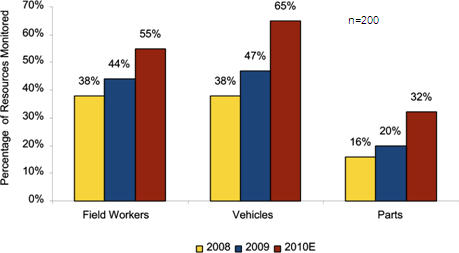

Responding firms indicated that on average they track the locations of approximately 44% of their field workers, 47% of their service vehicles and 20% of their service parts. There are positive indications of these proportions moving up to 55% for workers, 65% for vehicles and 32% for service parts in 2010. Responding firms clearly saw the value of tracking their resources as they indicated that nearly three-quarters of their workforce and service vehicles would benefit from the aid of GPS tracking technology.

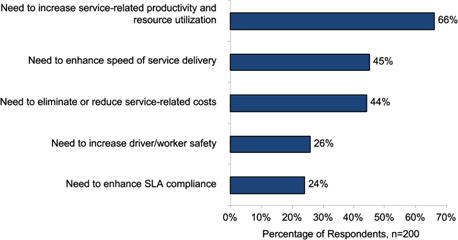

The need to increase worker productivity and vehicle utilization is the key driver for the increasing evaluation and use of location intelligence in the management of service resources. Given that firms indicated current utilization rates at around 50% for both workers and vehicles, it isn’t surprising that nearly two-thirds of firms indicated the pressing need to increase resource utilization. Nearly one-half of firms also cited the need to enhance the speed of service delivery and the need to cut service-related costs as key pressures driving the quest for location-enabled tools and workflows.

Cost containment continues to be the top priority for service executives; the research indicated that the cost per service dispatch has risen from $209 in 2006, to $263 in 2008, and to $276 in 2009. Efficiency is paramount for today’s service executive, striving to get the most from service resources in order to maintain and exceed customer expectations, while keeping a tight control on resource-related costs.

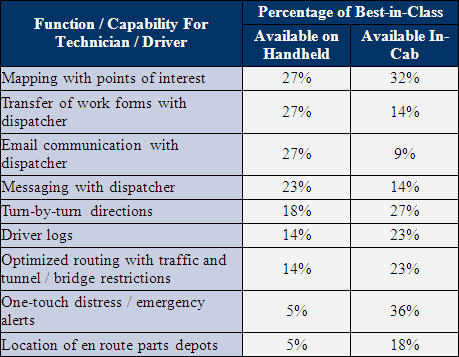

Firms have chosen a variety of devices and tools to incorporate the tracking and visibility components of GPS while providing their workers with access to mapping, navigation and routing. Devices range from the use of vehicle black boxes, mobile data terminals and vehicle sensors, to the use of mobile and smart phones, laptops or ruggedized handhelds. At this stage there seems to be a divergence between the use of handheld devices for work order functionality and the use of in-cab devices for mapping, navigation and tracking functionalities.

In fact, nearly 40% of firms indicated that they currently leverage separate devices for work order and location functionalities. However, 70% of respondents indicated their preference for a single device for all work order and location-enabled functionalities (handheld or in-cab), laying down the path for the increased convergence between GPS or workforce tracking and overall workforce mobility.

Best-in-Class organizations, those falling in the top 20% of aggregate performance metrics, are most likely to provide field workers with information on their mobile or in-cab devices using fleet management, routing and mobile applications. These firms are nearly twice as likely as all others to have fleet management applications in place and more than three times as likely to have intelligent routing applications. Routing is a key enabler for these firms as they look to decrease unnecessary mileage and service delays. Best-in-Class firms are also significantly more likely to leverage mobile field service applications so as to empower their field workers with required work order management functionalities.

Along with the increased reliance on these resource management applications, Best-in-Class firms are also significantly more likely to integrate location information in real-time with their scheduling, parts management and analytics systems. Integration with scheduling ensures the accurate dispatch of the right technician for every service order using location coordinates as a key input. Item-level parts tracking and integration with parts management systems ensure improved inventory management, and that service technicians are equipped with or made aware of the location of parts required for service visits. Effective integration with analytics tools allows for in-depth performance analysis by service executives and facilitates resource planning and forecasting capabilities.

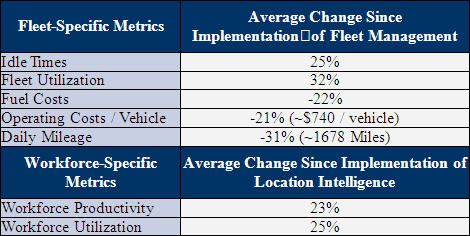

In terms of returns seen from the use of LBS, firms that have deployed location-enabled or fleet management tools have seen a significant improvement in the key metrics that are used to monitor workforce and fleet performance. For instance, responding firms highlighted a 23% improvement in workforce productivity with the assistance of better routing, scheduling and tracking, along with a 25% increase in workforce utilization.

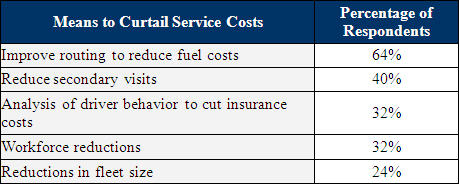

From a fleet perspective, firms reported a nearly 22% decrease in fuel costs with intelligent routing, navigation and vehicle management. This savings comes, in part, from the near-25% reduction in idle time, plus a daily mileage reduction of approximately 1,678 miles experienced by responding service organizations. The reduction in fuel, maintenance and insurance costs ultimately related to a 21% reduction in operating costs per vehicle for the average responding firms. This reduction amounted to nearly $750 in per-vehicle savings. While these results are impressive, they are typical of the average firm and not as high as those revealed by Best-in-Class companies. These firms magnify returns through the appropriate focus on processes and organizational capabilities mentioned throughout this article, which allow for the maximum utilization of the investment in technology.

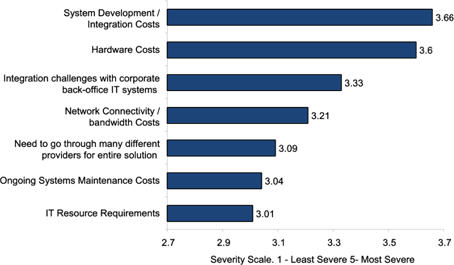

Despite the impressive returns, cost, integration and resource requirements are the challenges standing in the way of increased adoption of location-enabled tools. On a scale of 1 to 5, with 5 being the most severe, firms ranked system development and integration costs at a 3.66, and hardware costs at a 3.6. Further integration complexities with corporate back-office systems ranked third at 3.33. The firms that are ultimately able to maximize the use and value of location intelligence are those that are able to integrate and facilitate the bi-directional flow of data between location tracking tools in the field along with back office scheduling, routing and parts management systems. Not only does this ensure the effective empowerment of workers in the field, it also provides increased visibility to the back end service organization to effectively build a winning roadmap to Best-in-Class performance.

The current economic climate is exacerbating the cost challenges tied to solution adoption. While location intelligence tools and fleet management solutions go a long way in reducing service costs, nearly 35% of responding firms indicated that they are currently delaying their purchase of these solutions in the short-term, with another 18% delaying deployments. Twenty-four percent (24%) indicate that the economy is having no impact on purchase decisions. These statistics reveal a need for improved documentation of, and education around, the complete ROI offered by these location-enabled solutions.

A copy of this report on GPS in field service, made available with the support of Directions Media, Wireless Matrix, Intergis and GPS Insight, is available.

In a recent research survey of field service and manufacturing organizations conducted by Aberdeen, with the support of Directions Media, Wireless Matrix, Intergis and GPS Insight, only 35% of responding firms indicated that they currently track the whereabouts of their field technicians, with 47% indicating that they track the location of their service vehicles with the help of GPS technology. Just 19% of firms indicated that they actively track resources, such as parts and serviceable assets.

|

Responding firms indicated that on average they track the locations of approximately 44% of their field workers, 47% of their service vehicles and 20% of their service parts. There are positive indications of these proportions moving up to 55% for workers, 65% for vehicles and 32% for service parts in 2010. Responding firms clearly saw the value of tracking their resources as they indicated that nearly three-quarters of their workforce and service vehicles would benefit from the aid of GPS tracking technology.

|

The need to increase worker productivity and vehicle utilization is the key driver for the increasing evaluation and use of location intelligence in the management of service resources. Given that firms indicated current utilization rates at around 50% for both workers and vehicles, it isn’t surprising that nearly two-thirds of firms indicated the pressing need to increase resource utilization. Nearly one-half of firms also cited the need to enhance the speed of service delivery and the need to cut service-related costs as key pressures driving the quest for location-enabled tools and workflows.

|

Cost containment continues to be the top priority for service executives; the research indicated that the cost per service dispatch has risen from $209 in 2006, to $263 in 2008, and to $276 in 2009. Efficiency is paramount for today’s service executive, striving to get the most from service resources in order to maintain and exceed customer expectations, while keeping a tight control on resource-related costs.

|

Firms have chosen a variety of devices and tools to incorporate the tracking and visibility components of GPS while providing their workers with access to mapping, navigation and routing. Devices range from the use of vehicle black boxes, mobile data terminals and vehicle sensors, to the use of mobile and smart phones, laptops or ruggedized handhelds. At this stage there seems to be a divergence between the use of handheld devices for work order functionality and the use of in-cab devices for mapping, navigation and tracking functionalities.

|

In fact, nearly 40% of firms indicated that they currently leverage separate devices for work order and location functionalities. However, 70% of respondents indicated their preference for a single device for all work order and location-enabled functionalities (handheld or in-cab), laying down the path for the increased convergence between GPS or workforce tracking and overall workforce mobility.

Best-in-Class organizations, those falling in the top 20% of aggregate performance metrics, are most likely to provide field workers with information on their mobile or in-cab devices using fleet management, routing and mobile applications. These firms are nearly twice as likely as all others to have fleet management applications in place and more than three times as likely to have intelligent routing applications. Routing is a key enabler for these firms as they look to decrease unnecessary mileage and service delays. Best-in-Class firms are also significantly more likely to leverage mobile field service applications so as to empower their field workers with required work order management functionalities.

|

Along with the increased reliance on these resource management applications, Best-in-Class firms are also significantly more likely to integrate location information in real-time with their scheduling, parts management and analytics systems. Integration with scheduling ensures the accurate dispatch of the right technician for every service order using location coordinates as a key input. Item-level parts tracking and integration with parts management systems ensure improved inventory management, and that service technicians are equipped with or made aware of the location of parts required for service visits. Effective integration with analytics tools allows for in-depth performance analysis by service executives and facilitates resource planning and forecasting capabilities.

In terms of returns seen from the use of LBS, firms that have deployed location-enabled or fleet management tools have seen a significant improvement in the key metrics that are used to monitor workforce and fleet performance. For instance, responding firms highlighted a 23% improvement in workforce productivity with the assistance of better routing, scheduling and tracking, along with a 25% increase in workforce utilization.

|

From a fleet perspective, firms reported a nearly 22% decrease in fuel costs with intelligent routing, navigation and vehicle management. This savings comes, in part, from the near-25% reduction in idle time, plus a daily mileage reduction of approximately 1,678 miles experienced by responding service organizations. The reduction in fuel, maintenance and insurance costs ultimately related to a 21% reduction in operating costs per vehicle for the average responding firms. This reduction amounted to nearly $750 in per-vehicle savings. While these results are impressive, they are typical of the average firm and not as high as those revealed by Best-in-Class companies. These firms magnify returns through the appropriate focus on processes and organizational capabilities mentioned throughout this article, which allow for the maximum utilization of the investment in technology.

Despite the impressive returns, cost, integration and resource requirements are the challenges standing in the way of increased adoption of location-enabled tools. On a scale of 1 to 5, with 5 being the most severe, firms ranked system development and integration costs at a 3.66, and hardware costs at a 3.6. Further integration complexities with corporate back-office systems ranked third at 3.33. The firms that are ultimately able to maximize the use and value of location intelligence are those that are able to integrate and facilitate the bi-directional flow of data between location tracking tools in the field along with back office scheduling, routing and parts management systems. Not only does this ensure the effective empowerment of workers in the field, it also provides increased visibility to the back end service organization to effectively build a winning roadmap to Best-in-Class performance.

|

The current economic climate is exacerbating the cost challenges tied to solution adoption. While location intelligence tools and fleet management solutions go a long way in reducing service costs, nearly 35% of responding firms indicated that they are currently delaying their purchase of these solutions in the short-term, with another 18% delaying deployments. Twenty-four percent (24%) indicate that the economy is having no impact on purchase decisions. These statistics reveal a need for improved documentation of, and education around, the complete ROI offered by these location-enabled solutions.

A copy of this report on GPS in field service, made available with the support of Directions Media, Wireless Matrix, Intergis and GPS Insight, is available.

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement