It's all too easy to adopt a doom-and-gloom perspective in the wake of the financial downturn. While the housing and bank crises have undeniably impacted the global markets, a recent study of European retail by GfK GeoMarketing reveales that there are still areas of growth and untapped potential.

GfK GeoMarketing performed a spatial analysis of a wealth of economic and socio-demographic data to provide a detailed portrait of Europe's 2009 and 2010 retail scene. Although the results generally confirm the impact of the financial downturn, they also illustrate notable areas of growth and opportunities for businesses looking to improve their margins in these challenging times.

|

The study is an example of how the spatial analysis of market data - along with its visualization on up-to-date digital maps - can illuminate trends and pinpoint "hotspots" of growth even in periods of economic crisis.

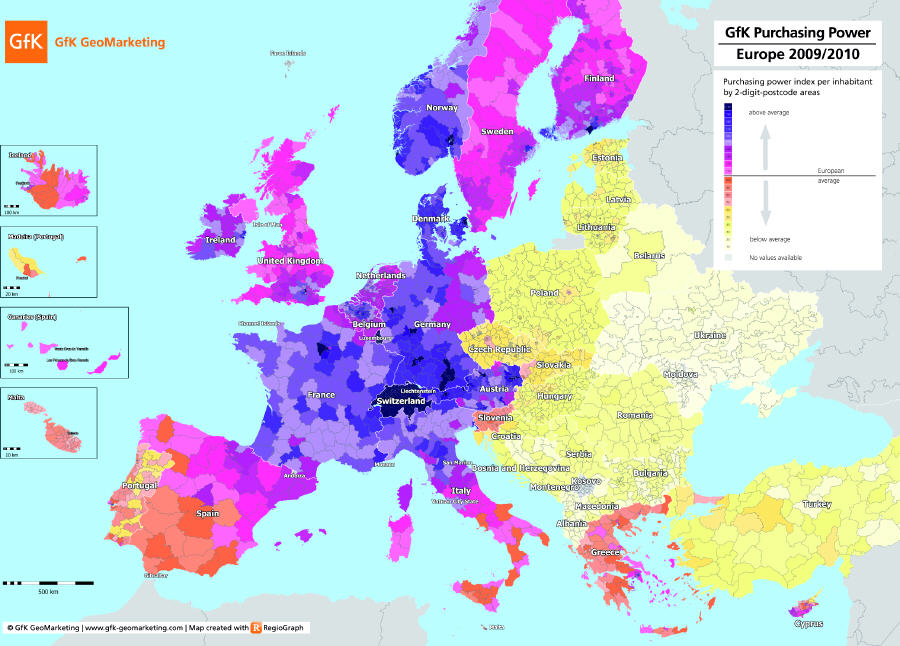

Mapping Europe-wide per capita GDP and purchasing power levels

The economic downturn has clearly impacted European retail on the whole, with per capita GDP levels down by more than 4% among the EU 29 (the 27 European Union member states, plus Norway and Switzerland). A geographic trend is apparent when these values are illustrated on a map. Purchasing power levels tend to increase moving from east to west and, to a lesser degree, south to north. Also, some of Europe's smallest countries boast the highest values.

At the top of the list is Luxembourg with €76,000, with a significant gap between the second- and third-ranking countries - Norway (€57,000) and Switzerland (€46,600). The average value among the EU 27 is €24,500. The large economies of France, Germany, Italy and the United Kingdom exceed this average. At the bottom of the rankings are the recent EU member states of Bulgaria (€4,400) and Romania (€5,600). The non-EU member countries of Russia (€7,400) and Turkey (€6,100) lie just above those in the rankings.

Per capita purchasing power levels exhibit a similar geographic pattern. Per capita purchasing power refers to the amount of net income an individual has at his or her disposal for a particular period of time. As such, this calculation is the most important benchmark of consumer potential.

Europe's 2009 purchasing power equates to an average of €11,699 per inhabitant. However, this figure varies significantly depending on the country and region in question. For example, while Norway has a purchasing power of €20,535 per inhabitant, Bulgaria has only €2,850 per inhabitant.

Purchasing power generally declines precipitously moving east of the former Iron Curtain. There are also significant geographic variations within individual countries. For example, purchasing power levels fall moving south in Italy, east in Germany and west in Spain. Also, many of Europe's major metropolitan areas - particularly in Western Europe - have significantly higher purchasing power levels than those found in the surrounding regions.

"A geographic analysis of market data gives companies a road map for reaching their turnover targets," explains GfK GeoMarketing retail expert Doris Hardt-Beischl. "Location is paramount, which is precisely why a geographic approach is so essential."

Substantial variations in retail spending across Europe

Retail spending levels differ tremendously from country to country. For example, economically plagued Russia is at the top of the list in retail spending compared to total private expenditures (61%). This percentage far outpaces even the closest runner-up, which is Bulgaria at 47%. Retail spending as a share of total private spending falls below 30% in Italy, Germany and Greece. Austria, Switzerland and Slovakia lie just above this mark at 31%. In the middle are Bulgaria, Estonia, Hungary, Croatia and Slovenia at 45%.

The determining factors for the noticeable variations in consumption behavior in Europe are primarily the differing levels of economic development and wealth, as well as pronounced differences in shopping cultures and lifestyles. Striking in this regard is the fact that France and Germany generated approximately the same amount of 2009 retail turnover (approx. €398 billion), despite the fact that Germany has an extra 20 million consumers. This can be attributed to the renowned frugality of the German people.

|

At €2,764 billion, the combined retail turnover of the EU 29 - including Croatia, Russia and Turkey - has declined over the past year for almost all European countries. Exceptions include Belgium (+0.3%), Austria (+2.1%) and Switzerland (+6.0%), although in the latter case the high level of growth is essentially a result of the exchange rate (the nominal growth in Swiss francs corresponded to around 0.8% from 2009 to 2010).

"Even if the retail turnover for a given country has declined as a whole, specific areas in that country can still offer growth opportunities," explains Hardt-Beischl. "This is another instance in which a spatial analysis of the data is so valuable, because it helps businesses focus their efforts in the areas that are going against the general trend."

Some modest signs of retail growth in 2010 despite financial crisis

GfK GeoMarketing's projections for retail in 2010 show the continuing effect of the economic downturn. Stagnation is anticipated for six countries, among which are the large markets of France (+0.4%) and Italy (-0.4%). Declines in retail turnover are forecasted for 11 countries, including Germany (-2.4%), the United Kingdom (-1.3%) and Spain (-1.5%). At the bottom of the 2010 turnover rankings are the two Baltic states of Lithuania (-6.6%) and Latvia (-15%). Given the recent events in Greece, retail turnover in this country will decline much more significantly than previously expected.

There is, however, a silver lining to these predictions. GfK GeoMarketing anticipates an increase in nominal retail turnover for 14 European countries in 2010. Positive developments are forecasted for Turkey (+8.5%) and Russia (+2.5%), the two countries with the highest nominal turnover growth, although this growth will be thwarted by a significant currency devaluation.

Inflation also remains a concern. For example, despite the forecasted retail growth for Russia, it remains plagued by inflation: 10.5% in 2009 and 9% in 2010. Turkey faces a similar predicament. By contrast, the price increase in consumption goods significantly slowed or even slipped into deflation in some countries in 2009 as a response to the economic downturn. Due to the anticipated increase in economic activity in 2010, the inflation rates in most European countries are expected to again increase slightly, although they will continue to remain at a very moderate level. The EU Commission expects an average change in inflation among the EU 27 from 1.1% in 2009 to 1.4% in 2010.

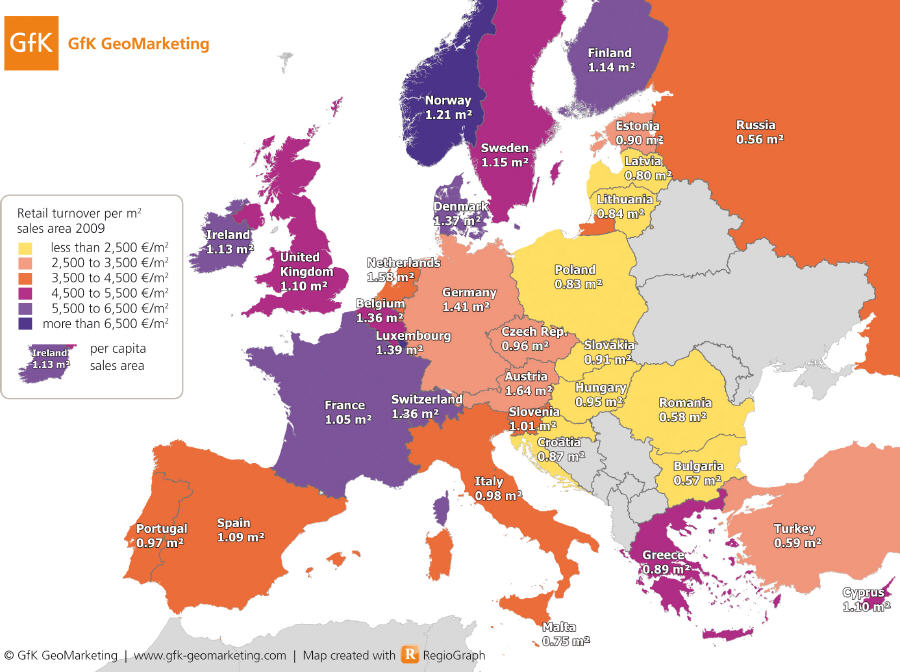

Tracking sales area productivity across Europe with geomarketing

Sales area productivity and per capita sales area are two of the key benchmarks used to assess retail performance. GfK GeoMarketing's spatial analysis of the relevant data reveals significant differences in these values across the continent.

|

The countries with the highest per capita sales area are generally in Central Europe, with Austria and the Netherlands occupying the top of the rankings at around 1.6 m2 per inhabitant. At the other end of the spectrum are Russia, Bulgaria and Turkey with a per capita sales area sometimes significantly below 0.6 m2.

"As a general rule, the peripheral regions of most countries tend to have comparatively low per capita sales areas," explains Hardt-Beischl. "There is even an over-capacity in many major cities in Central and Eastern Europe."

Given the general stagnation of economic development, it's notable that the recent EU member states of Slovenia, Hungary, Slovakia, the Czech Republic, Poland and the Baltic States have been catching up with the rest of Europe since the 1990s. These countries have now obtained a per capita sales area that nearly matches that of Italy and France, two of the EU founding countries.

Sales area productivity is a measure of the amount of turnover generated per square meter. With respect to this benchmark, Central and Eastern European countries - with the exception of Slovenia - are outperformed by the rest of Europe. Romania, Poland, Lithuania and Hungary generate around €2,000/m2. There is significant variation in sales area productivity among the large EU states, ranging from €6,100/m2 in France and €4,800 m2 in the United Kingdom to €4,200 m2 in Italy and €3,400 m2 in Germany. Luxembourg, with its unusually high level of purchasing power, is again top of the rankings in 2009 with €7,000 m2, followed by Norway and Ireland.

Spatial analysis essential for pinpointing "oases" of growth

One of the takeaways of GfK GeoMarketing's recent study of Europe's retail climate is the importance of avoiding generalizations in favor of an objective analysis of the relevant data. The geographic illustration of these data allows companies to tailor their operations and goals to the ever-shifting realities of the global marketplace.

"While the economic downturn makes achieving success more challenging, it does not preclude it," says Hardt-Beischl. "Companies can lay the groundwork for this success by implementing a geomarketing approach. This entails analyzing and illustrating place-based factors in order to spot trends and make more informed decisions."