Location-Based Services… another floundering data

service, or mobile application area of rapid growth? The answer to the

question today largely depends on geography. Not the geography inherent

to location-based applications themselves, but rather the geographic

characteristics of historical deployment trends. Since 1997, wireless

carrier mobile location services deployments across Europe, Asia and

the Americas have either focused on mobile positioning first or

applications first - a chicken and egg quandary driven largely by the

need to satisfy legislative requirements or respond to competitive

market pressures. Depending on whom you talk to within these

geographies, you might get one answer that suggests location-based

applications have not achieved the user adoption levels once

anticipated; where the other opposite answer will assert location-based

services’ ecosystem revenues are growing at unprecedented rates and

hold the promised balance of one of the brightest new futures of

Telecom-enabled IT. The former answer comes from those who deployed

applications first and the latter answer comes from those who deployed

high accuracy positioning first - and both answers are right.

In the late nineties, GSM wireless carriers throughout Europe assumed the global LBS market lead, deploying consumer-focused applications typically marketed and sold as premium data services under a larger mobile data bundle. During this time, the collective GSM goal was to get to market as fast as possible with applications in order to differentiate and attract mobile subscribers away from the competition or draw new subscribers through differentiation. Initial location-based application adoption rates across European geographies were lower than expected, leaving bitter aftertastes with most. Even today, some across the GSM world are quick to denounce location-based applications as viable revenue generators, often citing poor user experiences due to location-accuracy cavities with the underlying infrastructure and Cell-ID location technology deployed years ago.

During

the same time frame that Europe was leading the application race,

lagging US wireless carriers postponed commercial application promises

and focused energy on fulfilling legislative 911 emergency services

compliance mandates passed down by Washington and the FCC. With stiff

non-compliance fines looming, the collective US carrier-community’s

number one goal was to avoid federal government penalties, and the only

way to do that was to focus resources on deploying high-accuracy mobile

location infrastructure. With these initial goals achieved, and now set

aside as we move into a new era of market development, the focus for

each geographic market has shifted yet again.

During

the same time frame that Europe was leading the application race,

lagging US wireless carriers postponed commercial application promises

and focused energy on fulfilling legislative 911 emergency services

compliance mandates passed down by Washington and the FCC. With stiff

non-compliance fines looming, the collective US carrier-community’s

number one goal was to avoid federal government penalties, and the only

way to do that was to focus resources on deploying high-accuracy mobile

location infrastructure. With these initial goals achieved, and now set

aside as we move into a new era of market development, the focus for

each geographic market has shifted yet again.

In the US, the focus for the last two years has been on building out and diversifying commercial applications that use high-accuracy mobile location foundations - this refreshing renaissance will continue for many years to come. In Europe and elsewhere, however, GSM wireless carriers are now looking to embark on their own high-accuracy phase of mobile location deployments following the US market lead.

Proof that high-accuracy mobile location systems pay off is hard to come by. Outside of the US and Asia, there simply are not many successes to reference. In Asian CDMA markets, modest gains in pedestrian navigation, gaming and community collaboration services have sprung up around A-GPS-in-CDMA foundations, but for cultural characteristics these application services mysteriously find rare replication in markets outside the Asia-Pacific region.

In the US, successes thus far are limited predominantly to the Sprint Nextel ecosystem, with Verizon making recent gains. Sprint Nextel, along with its large developer community, has become a sort of global poster child for success. Most in the global Telecom community recognize that its years of diligent work with its device manufacturers, GPS chipset vendors, mobile software providers, and partner-developers primed the carrier for rapid growth beginning in late 2003 and early 2004. Within the first year of exposing IP-based network and handset-initiated mobile location APIs to its business customers and developer-partners, Sprint Nextel had built an application portfolio unmatched by any wireless carrier in world. To date, Sprint Nextel has deployed dozens upon dozens of branded and private label applications into the customer base.

With a strong heritage in serving businesses, Sprint Nextel users now find mobile resource management no longer confined to the big business elite who can afford expensive GPS black-box tracking systems designed for large fleets. Now, any small-to-medium business across all vertical industries can use inexpensive GPS-enabled mobile phones and supporting applications for remote monitoring, communications and safety. They will also increase mobile productivity by accurately accounting for billable employee time to lower operational expenditures and provide higher levels of service to their customers, partners and suppliers. In addition to easy return on investment found by users, Sprint Nextel and its developer-partners are also reaping the rewards, positioning location-enhanced business productivity tools as high-yield premium mobile consumables that business subscribers are willing to purchase given the ROI results achieved.

All around, Sprint Nextel’s application ecosystem economics

present compelling adoption proofs that high accuracy mobile location

platforms pay off. The collective developer-partner community serves

nearly half-a-million individual subscribers, of which 90% are business

customers [Driscoll, 2006]. Most business users pay on the order of $10

- $15 per subscriber per month for various point-solution applications.

Do the math and at a glance you can see that modest revenue is being

generated, with enough for all value-chain players to accrue profits.

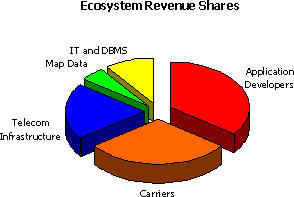

Approximately 60% of top line revenue is going to partner-developers

and their IT and map data suppliers, and approximately 40% is going to

Sprint Nextel and its telecom infrastructure suppliers and partners, as

shown in the figure to the right.

All around, Sprint Nextel’s application ecosystem economics

present compelling adoption proofs that high accuracy mobile location

platforms pay off. The collective developer-partner community serves

nearly half-a-million individual subscribers, of which 90% are business

customers [Driscoll, 2006]. Most business users pay on the order of $10

- $15 per subscriber per month for various point-solution applications.

Do the math and at a glance you can see that modest revenue is being

generated, with enough for all value-chain players to accrue profits.

Approximately 60% of top line revenue is going to partner-developers

and their IT and map data suppliers, and approximately 40% is going to

Sprint Nextel and its telecom infrastructure suppliers and partners, as

shown in the figure to the right.

Furthermore, the community has just scratched the surface, considering there are 47 million more addressable subscribers on the Sprint Nextel network alone. Beyond partner-developer point solution application revenues, comes an additional promise of direct carrier revenue gains from content providers, businesses and developers using mobile location and other Telecom capabilities directly within existing applications. This application genre uses the carrier as a ‘software service’ provider to power existing applications, simplifying the value chain to direct out-of-pocket Web services expenses for content providers, businesses and developers, and direct software-service revenues for the carrier. This emerging ‘smart pipe’ concept, while in a nascent stage of adoption, is nonetheless the one approach that flirts with the Holy Grail vision for a truly converged Telecom and IT world, and places the carrier in a new position to enter the software business through Web services. It might be a stretch to think of a carrier as a software provider, but from an application perspective, what’s the difference between making a Web services-based request for a map or a photo, and making a Web service request for a mobile location or to push an MMS alert? I bet a coder immersed in the Web 2.0 mash-up trend wouldn’t recognize the difference and neither should a professional…

Now, I again have to ask the question I asked nearly a year ago - "Why so successful? Is it because Sprint Nextel traditionally serves a business and government customer base that already understands the value of location, and how to use it? Is it because they built a developer-friendly habitat? Is it because they have aggressively embraced LBS and dedicated marketing energy and campaigns behind applications? Is it because they deployed superior location technology?" [Directions Magazine, 2005].

Advocates of the Sprint Nextel market approach and business development/marketing philosophy will contend that all of the above successful executions have catapulted the carrier to the global LBS pole position. But without a doubt, the high-accuracy A-GPS location catalyst and efficiencies of their IP-based architectures laid the foundations from which to initially grow so rapidly. The GSM community, now embarking on their own high-accuracy mobile location initiatives (be they A-GPS or built on foundations of the future Galileo system), will serve themselves well by not only exploring the IP-based location foundations that Sprint Nextel adopted, but by also gravitating towards business models that monetize mobile location on an open API Web services basis, bundled transport basis for handset-initiated location queries, as well as through premium messaging packages where location costs are camouflaged.

European developers have no shortage of application creativity and ideas, as early years proved, and once the mobile location technology and business model items are sorted out (yet again), I look forward to seeing the European flavors of applications that accurate mobile location will support. My guess is there are a lot more local pedestrian services on the horizon, as well as a new breed of analytical applications that content providers will use to serve localized mobile information societies with relevant content based on their own semantically defined community of interest geographies.

References

Mobile Resource Management Systems Market Study, C.J. Driscoll & Associates 2005-06

Wireless Location Uses in the User Plane and Control Plane, Directions Magazine, July 4, 2005

In the late nineties, GSM wireless carriers throughout Europe assumed the global LBS market lead, deploying consumer-focused applications typically marketed and sold as premium data services under a larger mobile data bundle. During this time, the collective GSM goal was to get to market as fast as possible with applications in order to differentiate and attract mobile subscribers away from the competition or draw new subscribers through differentiation. Initial location-based application adoption rates across European geographies were lower than expected, leaving bitter aftertastes with most. Even today, some across the GSM world are quick to denounce location-based applications as viable revenue generators, often citing poor user experiences due to location-accuracy cavities with the underlying infrastructure and Cell-ID location technology deployed years ago.

During

the same time frame that Europe was leading the application race,

lagging US wireless carriers postponed commercial application promises

and focused energy on fulfilling legislative 911 emergency services

compliance mandates passed down by Washington and the FCC. With stiff

non-compliance fines looming, the collective US carrier-community’s

number one goal was to avoid federal government penalties, and the only

way to do that was to focus resources on deploying high-accuracy mobile

location infrastructure. With these initial goals achieved, and now set

aside as we move into a new era of market development, the focus for

each geographic market has shifted yet again. In the US, the focus for the last two years has been on building out and diversifying commercial applications that use high-accuracy mobile location foundations - this refreshing renaissance will continue for many years to come. In Europe and elsewhere, however, GSM wireless carriers are now looking to embark on their own high-accuracy phase of mobile location deployments following the US market lead.

Proof that high-accuracy mobile location systems pay off is hard to come by. Outside of the US and Asia, there simply are not many successes to reference. In Asian CDMA markets, modest gains in pedestrian navigation, gaming and community collaboration services have sprung up around A-GPS-in-CDMA foundations, but for cultural characteristics these application services mysteriously find rare replication in markets outside the Asia-Pacific region.

In the US, successes thus far are limited predominantly to the Sprint Nextel ecosystem, with Verizon making recent gains. Sprint Nextel, along with its large developer community, has become a sort of global poster child for success. Most in the global Telecom community recognize that its years of diligent work with its device manufacturers, GPS chipset vendors, mobile software providers, and partner-developers primed the carrier for rapid growth beginning in late 2003 and early 2004. Within the first year of exposing IP-based network and handset-initiated mobile location APIs to its business customers and developer-partners, Sprint Nextel had built an application portfolio unmatched by any wireless carrier in world. To date, Sprint Nextel has deployed dozens upon dozens of branded and private label applications into the customer base.

With a strong heritage in serving businesses, Sprint Nextel users now find mobile resource management no longer confined to the big business elite who can afford expensive GPS black-box tracking systems designed for large fleets. Now, any small-to-medium business across all vertical industries can use inexpensive GPS-enabled mobile phones and supporting applications for remote monitoring, communications and safety. They will also increase mobile productivity by accurately accounting for billable employee time to lower operational expenditures and provide higher levels of service to their customers, partners and suppliers. In addition to easy return on investment found by users, Sprint Nextel and its developer-partners are also reaping the rewards, positioning location-enhanced business productivity tools as high-yield premium mobile consumables that business subscribers are willing to purchase given the ROI results achieved.

All around, Sprint Nextel’s application ecosystem economics

present compelling adoption proofs that high accuracy mobile location

platforms pay off. The collective developer-partner community serves

nearly half-a-million individual subscribers, of which 90% are business

customers [Driscoll, 2006]. Most business users pay on the order of $10

- $15 per subscriber per month for various point-solution applications.

Do the math and at a glance you can see that modest revenue is being

generated, with enough for all value-chain players to accrue profits.

Approximately 60% of top line revenue is going to partner-developers

and their IT and map data suppliers, and approximately 40% is going to

Sprint Nextel and its telecom infrastructure suppliers and partners, as

shown in the figure to the right. Furthermore, the community has just scratched the surface, considering there are 47 million more addressable subscribers on the Sprint Nextel network alone. Beyond partner-developer point solution application revenues, comes an additional promise of direct carrier revenue gains from content providers, businesses and developers using mobile location and other Telecom capabilities directly within existing applications. This application genre uses the carrier as a ‘software service’ provider to power existing applications, simplifying the value chain to direct out-of-pocket Web services expenses for content providers, businesses and developers, and direct software-service revenues for the carrier. This emerging ‘smart pipe’ concept, while in a nascent stage of adoption, is nonetheless the one approach that flirts with the Holy Grail vision for a truly converged Telecom and IT world, and places the carrier in a new position to enter the software business through Web services. It might be a stretch to think of a carrier as a software provider, but from an application perspective, what’s the difference between making a Web services-based request for a map or a photo, and making a Web service request for a mobile location or to push an MMS alert? I bet a coder immersed in the Web 2.0 mash-up trend wouldn’t recognize the difference and neither should a professional…

Now, I again have to ask the question I asked nearly a year ago - "Why so successful? Is it because Sprint Nextel traditionally serves a business and government customer base that already understands the value of location, and how to use it? Is it because they built a developer-friendly habitat? Is it because they have aggressively embraced LBS and dedicated marketing energy and campaigns behind applications? Is it because they deployed superior location technology?" [Directions Magazine, 2005].

Advocates of the Sprint Nextel market approach and business development/marketing philosophy will contend that all of the above successful executions have catapulted the carrier to the global LBS pole position. But without a doubt, the high-accuracy A-GPS location catalyst and efficiencies of their IP-based architectures laid the foundations from which to initially grow so rapidly. The GSM community, now embarking on their own high-accuracy mobile location initiatives (be they A-GPS or built on foundations of the future Galileo system), will serve themselves well by not only exploring the IP-based location foundations that Sprint Nextel adopted, but by also gravitating towards business models that monetize mobile location on an open API Web services basis, bundled transport basis for handset-initiated location queries, as well as through premium messaging packages where location costs are camouflaged.

European developers have no shortage of application creativity and ideas, as early years proved, and once the mobile location technology and business model items are sorted out (yet again), I look forward to seeing the European flavors of applications that accurate mobile location will support. My guess is there are a lot more local pedestrian services on the horizon, as well as a new breed of analytical applications that content providers will use to serve localized mobile information societies with relevant content based on their own semantically defined community of interest geographies.

References

Mobile Resource Management Systems Market Study, C.J. Driscoll & Associates 2005-06

Wireless Location Uses in the User Plane and Control Plane, Directions Magazine, July 4, 2005

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement