In a recent podcast,

I discussed a new categorization and profile for the geospatial

technology industry that I called the "Geospatial Quadrant" (GQ). I

received many comments on the GQ, and in response to them let me

further define the quadrant extents and boundaries.

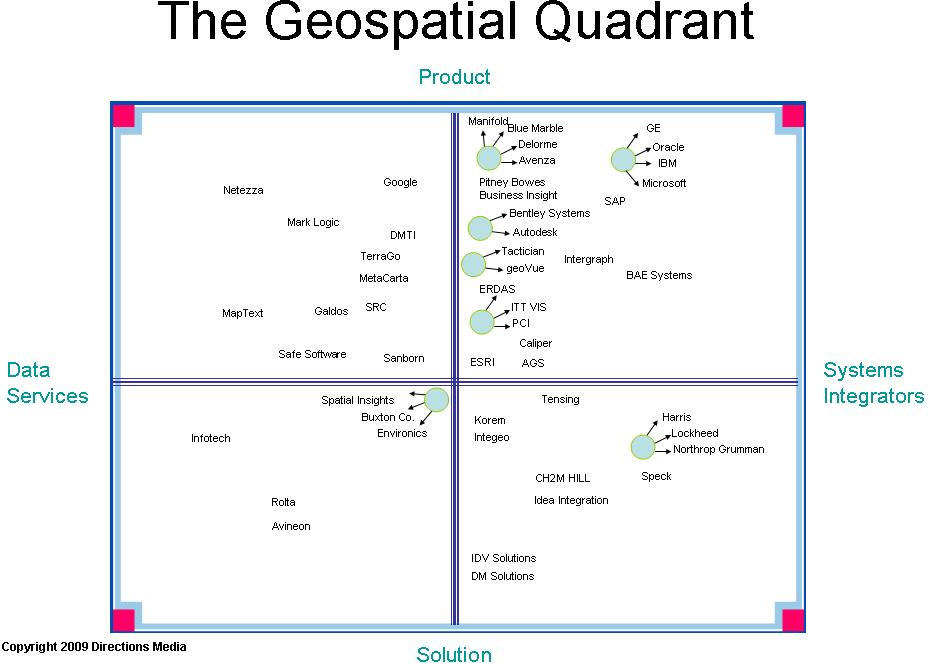

Many people asked me if the GQ has a "magic quadrant." It does not. The question references Gartner's "magic quadrant," that market research company’s diagram which describes a market or industry. In its diagram, Gartner’s magic quadrant identifies the market sector’s "leaders" and others including "visionaries," "niche players" and "challengers." Each, in that order, is placed clockwise from the upper left, with "leaders" in that upper left quadrant. Gartner’s quadrants are used to describe the dynamics of a market, specifically which companies might be considered the market leaders and which hold lesser roles, constrained by size, revenue or expertise - at least that is my interpretation.

In contrast, the GQ illustrates the extents of the services, products and solutions that comprise the geospatial technology market. As a dynamic market, there is movement between quadrants. The axes of the GQ represent extreme extents. For example, pure product companies reside at the top of the Product axis, whereas Solution companies, those offering none of their own software or hardware for sale, reside at the opposite end of this axis. The vertical "y" axis would be best described as the Build & Make axis. At the other extent, Data Services companies manipulate and augment attribution to geospatial data that creates a value-added result. Systems Integrators take value-added solutions, software products and other components and deliver client-specified work products and consulting services on which their in-house experts or team of sub-contractors collaborate. As such, this "x" axis of Data Services-Systems Integrators represents companies that Serve & Consult rather than Build & Make. Already, you probably see gray areas and potential overlap, and that is certainly the nature of these quadrants.

Let me further define the extents. Consider each definition in the extreme sense.

There is a missing component of the GQ framework: geospatial data. If I could add a third dimension to the original GQ, I would add Raster-Vector-Content (RVC), where content is best represented by demographic information, as well as dynamic, real-time data. But there is no continuum among these geospatial data formats; they are either of one type or another. Services vary depending on scope and complexity. RVC is represented by discrete entities.

In the context of the geospatial market, there has been a radical shift toward services and solutions in the last three to five years, with mergers, acquisitions and new players entering this technology sector. In the early 1990s, when the first real boom in the geospatial technology sector was taking place and doing so in parallel to the PC market, mainframe and mini-computer software solutions were evolving to desktop mapping products. Software companies like ESRI, Intergraph, Autodesk and MapInfo were engaged in a fight to develop the best channel of qualified business partners. Today, the channel is more important to some (Autodesk), less important to others (ESRI, Intergraph, MapInfo).

In the Product domain, more niche, component solutions (e.g. APIs, visualization platforms like Google Earth, etc.) are offered rather than monolithic, "do-it-all" thick clients. More products are server-based to accommodate some customization (e.g. ArcGIS Server) and more users. Some applications (e.g. ERDAS Image Web Server) are developed to be Web services for better integration and to be updated more frequently. The development architectures of Flex and REST, for example, provide "simplified component implementation" (source: Wikipedia) and rich Internet application development. Google sits at the top of this axis as a provider of APIs and consumer visualization Web services (Google Maps/Earth), and because it is data-driven through its search engine business, it resides on the left side of the GQ. Netezza (Netezza Spatial), to the far left, delivers as a box of hardware and software to crunch data. By contrast, Oracle (Oracle Spatial), crunches data but has such a large service element to its business that it clearly must be positioned in the upper right quadrant.

In the Solution domain, the ability to rapidly prototype solutions has led some smaller companies to question whether they are pure solution architects or "mini" systems integrators. Again, the market is dynamic and movement within and between quadrants is constant, leaving quadrant placement up for interpretation. I listed IDV Solutions as an example here because of its strong services business. While the company does offer products, it most often uses them in its solution business. IDV Solutions is a good example of a company likely to move up the axis as its business moves toward a product-oriented future, if the leadership so desires.

In the Data Quality domain, I think there are some "pure" examples. Infotech is a good example of a company with a primary focus in quality assurance (QA) and quality control (QC). While visiting the company’s offices in Hyderabad, India I was amazed to see floor upon floor, building upon building, staffed with GIS workers. Their job was to perform QA for companies like Tele Atlas, and data entry for a telecommunications network compilation project. Both involved dozens of workers for each. And yet, clearly companies want to move among the quadrants. If they are big enough, they probably reside in more than one. Rolta is an example of a company that may have started in the lower left quadrant but because of the introduction of geospatial products such as Rolta OnPoint it could easily move diagonally into the upper right.

SIs are strange beasts; by their nature and idiomatic definition, they are behemoths of the IT industry. In the geo-intelligence sector of the defense business they are particularly potent animals. These companies usually don’t touch a deal unless millions of dollars are at stake and they are right at home pulling together "smaller" companies into their fold to bid on large contracts. They are the least likely to move to a different sector of the GQ.

Finally, let me acknowledge that this not an exhaustive study, nor is it quantitative. It is based on my 30 years in the geospatial business. I offer this as a guide for our readers who might benefit from some deeper understanding of the marketplace. I welcome any and all feedback.

Many people asked me if the GQ has a "magic quadrant." It does not. The question references Gartner's "magic quadrant," that market research company’s diagram which describes a market or industry. In its diagram, Gartner’s magic quadrant identifies the market sector’s "leaders" and others including "visionaries," "niche players" and "challengers." Each, in that order, is placed clockwise from the upper left, with "leaders" in that upper left quadrant. Gartner’s quadrants are used to describe the dynamics of a market, specifically which companies might be considered the market leaders and which hold lesser roles, constrained by size, revenue or expertise - at least that is my interpretation.

In contrast, the GQ illustrates the extents of the services, products and solutions that comprise the geospatial technology market. As a dynamic market, there is movement between quadrants. The axes of the GQ represent extreme extents. For example, pure product companies reside at the top of the Product axis, whereas Solution companies, those offering none of their own software or hardware for sale, reside at the opposite end of this axis. The vertical "y" axis would be best described as the Build & Make axis. At the other extent, Data Services companies manipulate and augment attribution to geospatial data that creates a value-added result. Systems Integrators take value-added solutions, software products and other components and deliver client-specified work products and consulting services on which their in-house experts or team of sub-contractors collaborate. As such, this "x" axis of Data Services-Systems Integrators represents companies that Serve & Consult rather than Build & Make. Already, you probably see gray areas and potential overlap, and that is certainly the nature of these quadrants.

Let me further define the extents. Consider each definition in the extreme sense.

- Product: Product companies sell boxes: software, hardware, etc.

- Solution: Solution providers make, design or program none of their own software, but would construct software solutions from APIs, components and other platforms using programming expertise. The end result is a unique, customized product that may be integrated with other solutions or may stand alone.

- Data Services: These companies "massage" data. Companies in this sector provide quality assurance (QA) services; extract, transform and load (ETL) services; indexing, translation, geocoding and a host of other processes that take data in one form and create a hybrid or value-added form.

- Systems Integrator (SI): SIs perform consultative, advisory and project management services. In other words, rarely do they deal directly with QA, but they do bring the by-products of QA, and solutions and products together. I defer to the Wikipedia definition of an SI, which states that it is "a person or company that specializes in bringing together component subsystems into a whole and ensuring that those subsystems function together."

|

There is a missing component of the GQ framework: geospatial data. If I could add a third dimension to the original GQ, I would add Raster-Vector-Content (RVC), where content is best represented by demographic information, as well as dynamic, real-time data. But there is no continuum among these geospatial data formats; they are either of one type or another. Services vary depending on scope and complexity. RVC is represented by discrete entities.

In the context of the geospatial market, there has been a radical shift toward services and solutions in the last three to five years, with mergers, acquisitions and new players entering this technology sector. In the early 1990s, when the first real boom in the geospatial technology sector was taking place and doing so in parallel to the PC market, mainframe and mini-computer software solutions were evolving to desktop mapping products. Software companies like ESRI, Intergraph, Autodesk and MapInfo were engaged in a fight to develop the best channel of qualified business partners. Today, the channel is more important to some (Autodesk), less important to others (ESRI, Intergraph, MapInfo).

In the Product domain, more niche, component solutions (e.g. APIs, visualization platforms like Google Earth, etc.) are offered rather than monolithic, "do-it-all" thick clients. More products are server-based to accommodate some customization (e.g. ArcGIS Server) and more users. Some applications (e.g. ERDAS Image Web Server) are developed to be Web services for better integration and to be updated more frequently. The development architectures of Flex and REST, for example, provide "simplified component implementation" (source: Wikipedia) and rich Internet application development. Google sits at the top of this axis as a provider of APIs and consumer visualization Web services (Google Maps/Earth), and because it is data-driven through its search engine business, it resides on the left side of the GQ. Netezza (Netezza Spatial), to the far left, delivers as a box of hardware and software to crunch data. By contrast, Oracle (Oracle Spatial), crunches data but has such a large service element to its business that it clearly must be positioned in the upper right quadrant.

In the Solution domain, the ability to rapidly prototype solutions has led some smaller companies to question whether they are pure solution architects or "mini" systems integrators. Again, the market is dynamic and movement within and between quadrants is constant, leaving quadrant placement up for interpretation. I listed IDV Solutions as an example here because of its strong services business. While the company does offer products, it most often uses them in its solution business. IDV Solutions is a good example of a company likely to move up the axis as its business moves toward a product-oriented future, if the leadership so desires.

In the Data Quality domain, I think there are some "pure" examples. Infotech is a good example of a company with a primary focus in quality assurance (QA) and quality control (QC). While visiting the company’s offices in Hyderabad, India I was amazed to see floor upon floor, building upon building, staffed with GIS workers. Their job was to perform QA for companies like Tele Atlas, and data entry for a telecommunications network compilation project. Both involved dozens of workers for each. And yet, clearly companies want to move among the quadrants. If they are big enough, they probably reside in more than one. Rolta is an example of a company that may have started in the lower left quadrant but because of the introduction of geospatial products such as Rolta OnPoint it could easily move diagonally into the upper right.

SIs are strange beasts; by their nature and idiomatic definition, they are behemoths of the IT industry. In the geo-intelligence sector of the defense business they are particularly potent animals. These companies usually don’t touch a deal unless millions of dollars are at stake and they are right at home pulling together "smaller" companies into their fold to bid on large contracts. They are the least likely to move to a different sector of the GQ.

Finally, let me acknowledge that this not an exhaustive study, nor is it quantitative. It is based on my 30 years in the geospatial business. I offer this as a guide for our readers who might benefit from some deeper understanding of the marketplace. I welcome any and all feedback.

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement