After numerous fits and starts, over-hyped

expectations, technology turmoil and vendor shakeouts, location-based

services (LBS) are finally poised to take off

in 2006 and 2007. In essence, all the business and technology stars

have finally started to align.

Why didn’t this happen earlier? The reasons for the slow takeoff of LBS, and why things are different now, boil down to the following:

Other issues still need to be resolved. Difficulties in location tracking in indoor environments continue to bedevil certain applications. Privacy concerns are, if anything, even more acute then they were a few years ago, yet the technical, legal and political mechanisms for dealing with them have progressed only slightly.

That said, improvements have been made on enough fronts that we are finally on the cusp of an LBS breakout. 2005 was the year of LBS’ reemergence, with carriers such as Sprint Nextel and Vodafone demonstrating a renewed commitment to location based services. 2006 will be the year of new application introduction, as other carriers and a proliferation of new developers begin to bring their applications online. 2007 will see subscriptions to LBS applications begin an explosive growth phase as familiarity with LBS applications penetrates a critical mass of market segments and those segments, which will see the benefits of adoption enjoyed by their peers or competitors.

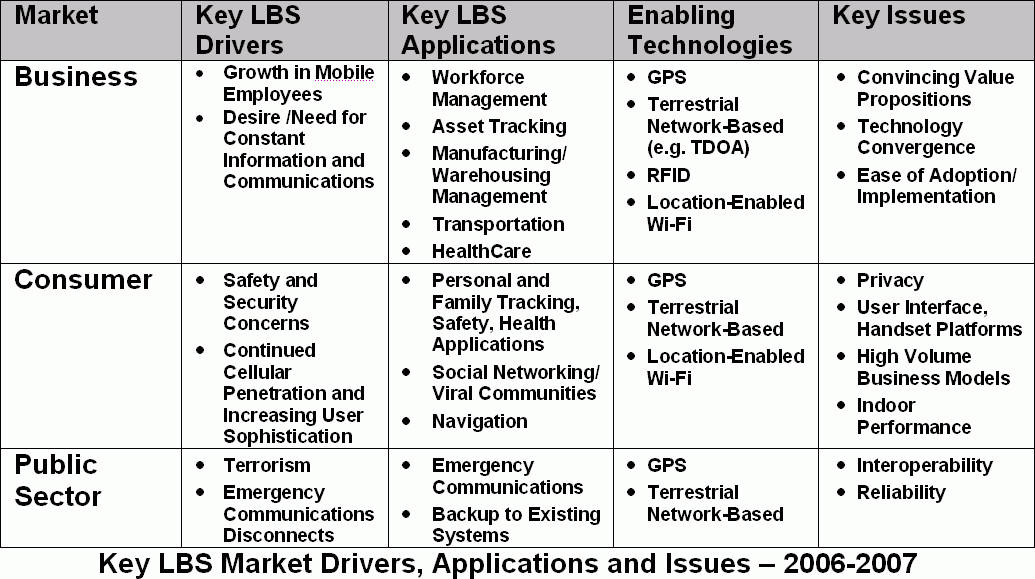

As the above diagram illustrates, the applications that will drive this

growth vary depending on whether you are talking about business,

consumer or public sector markets, the needs of individual segments

within those markets, as well as the particulars of the targeted

geographic region. For business markets, the growth of LBS is being

driven both by an ever more mobile workforce and the need for

continuous information about worker productivity and

the assets being used. For consumer markets, concern with safety and

security will drive adoption of more services, particularly as families

understand the value proposition (e.g. immediately know where children

and seniors are located). Social networking

applications will be adopted by the

youth and singles market sector. Personal navigation services will

continue to gain

in penetration, particularly in Europe. Senior care applications will

grow as Japan’s population continues to age. Opportunities will also

exist in the public sector, as concerns about terrorism and continued

breakdowns in emergency communications during major disasters open

the doors to public sector-focused location-based services as

complements, alternatives or backups to existing systems.

Looking forward beyond 2006 and 2007, LBS stakeholders need to broaden their view beyond just GPS/Network-based location technologies and associated applications, and anticipate its convergence with Radio Frequency Identification (RFID) and location-enabled Wi-Fi. Advances in the price and performance of both offer the opportunity for complementary and in some cases competing location-based services, as well as opening the door for location to be applied to markets not accessible before, such as health care.

In addition, LBS designers need to anticipate the next generation of user interface devices coming down the road. If there is a key remaining technical weakness in the LBS technology value chain it is the multitude of user devices that initiate and receive LBS information. Even more important is that the devices and user interfaces we have are still inherently limiting by forcing the user to physically type LBS requests and receive information on a small screen. These are annoying at best and dangerous at worst for many types of location services. LBS designers need to anticipate a likely shakeout of sorts in user devices (LBS iPod anyone?) and continued advances in voice recognition, LBS data to voice conversion and delivery, and others will enable truly easy-to-use applications, These will be unhindered by the physical and technology limitations that exist in today’s handsets.

We’ve come a long way since the “dark” LBS years earlier this decade, and are finally on the cusp of the opportunities that many of us have been working and waiting for over many years. Let’s make the most of it!

Why didn’t this happen earlier? The reasons for the slow takeoff of LBS, and why things are different now, boil down to the following:

- Then: Immature positioning technologies. Now: Cellular carriers have finally stabilized their network platforms and position determination technologies, with A-GPS and TDOA in the U.S., for example.

- Then: Multiple network platforms and slow network speeds. Now: 2.5G on a single network platform for nearly all carriers, with 3G on the way.

- Then: Weak handsets in terms of memory, graphics display capabilities and user interface mechanisms. Now: Dramatic feature upgrades, even for low-end handsets.

- Then: Carrier preoccupation with other initiatives: network platform migration, wireless E911, wireless number portability, 802.11x/Wi-Fi. Now: Renewed focus on new revenue sources.

- Then: Immature customer base unaccustomed to dealing with anything beyond voice. Now: Wireless penetration into nearly all significant demographic segments, including children and seniors, and across the entire economic spectrum in nearly all regions of the globe, with increasing user familiarity and sophistication in most segments with new wireless applications. Growing familiarity with location technology (e.g. GPS) across wide swaths of wireless users.

- Then: Confusion on part of location application developers as to what and how to design LBS applications. Now: Creation and stabilization of standards, protocols and application developer programs and tools for both platforms/middleware and handsets, such as Java, MLP, OpenLS, J2ME (GSM) and BREW (CDMA).

- Then: Underestimation of the complexities involved in putting together an integrated end-to-end location business. Now: Hard lessons learned are being applied so that ALL dimensions of an LBS business are appropriately addressed: value proposition articulation, business model selection, user interface design, development tools, partnership strategies, marketing strategies, operational and support execution, etc.

- Then: Mass market approach – Poor value propositions, assumption that one location application fits all, little design innovation. Now: An appreciation for AND execution towards individual LBS segments, particularly in articulating clear value propositions, with product packaging focused on delivering that value and marketing to match.

Other issues still need to be resolved. Difficulties in location tracking in indoor environments continue to bedevil certain applications. Privacy concerns are, if anything, even more acute then they were a few years ago, yet the technical, legal and political mechanisms for dealing with them have progressed only slightly.

That said, improvements have been made on enough fronts that we are finally on the cusp of an LBS breakout. 2005 was the year of LBS’ reemergence, with carriers such as Sprint Nextel and Vodafone demonstrating a renewed commitment to location based services. 2006 will be the year of new application introduction, as other carriers and a proliferation of new developers begin to bring their applications online. 2007 will see subscriptions to LBS applications begin an explosive growth phase as familiarity with LBS applications penetrates a critical mass of market segments and those segments, which will see the benefits of adoption enjoyed by their peers or competitors.

|

Looking forward beyond 2006 and 2007, LBS stakeholders need to broaden their view beyond just GPS/Network-based location technologies and associated applications, and anticipate its convergence with Radio Frequency Identification (RFID) and location-enabled Wi-Fi. Advances in the price and performance of both offer the opportunity for complementary and in some cases competing location-based services, as well as opening the door for location to be applied to markets not accessible before, such as health care.

In addition, LBS designers need to anticipate the next generation of user interface devices coming down the road. If there is a key remaining technical weakness in the LBS technology value chain it is the multitude of user devices that initiate and receive LBS information. Even more important is that the devices and user interfaces we have are still inherently limiting by forcing the user to physically type LBS requests and receive information on a small screen. These are annoying at best and dangerous at worst for many types of location services. LBS designers need to anticipate a likely shakeout of sorts in user devices (LBS iPod anyone?) and continued advances in voice recognition, LBS data to voice conversion and delivery, and others will enable truly easy-to-use applications, These will be unhindered by the physical and technology limitations that exist in today’s handsets.

We’ve come a long way since the “dark” LBS years earlier this decade, and are finally on the cusp of the opportunities that many of us have been working and waiting for over many years. Let’s make the most of it!

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement