The market for wireless data applications in the

enterprise has entered a transformational phase, and growth is

accelerating. A major component of the change is the integration of

location into mobile applications to provide context to mobile data and

increase their utility. VDC Research recently asked enterprise IT

managers if they had integrated, or were planning to integrate,

location data into their applications; 18.9% reported that they already

had, while 20.7% said they planned to do so. By integrating location,

application developers can increase usability and managers can improve

control and visibility into their operations.

It is important for a supply chain manager to know the drop-off location of a package so that processes and transactions can be completed. This task can be supported by a geofencing application that allows him to determine within which geographic areas the service has been provided and helps ensure that visibility and control are maintained. Giving "road warriors" the ability to seamlessly obtain directions to the next business meeting without even accessing their calendars improves usability. These are examples of how location data are leading to more sophisticated applications and business processes. Location-aware applications will be the norm in the future, and the competition to deliver these services will intensify. New business models and distribution channels will continue to evolve, presenting more dynamic partnership opportunities and go-to-market strategies.

The emergence of location and the ways in which it produces contexts and value when integrated with other data sources are also changing how vendors are deploying mobile applications. Mobile platforms are becoming more flexible and componentized so business process experts can integrate appropriate data to produce solutions that result in tremendous ROI. This decoupling of features and functionality will also lead to delineation in the value chain and vendors will increasingly focus on what they do best.

Market participants need to understand changes in the current value chain and technology in order to make the right decisions today that will position them to take advantage of this growing opportunity. In order to better understand the direction of the market, planners should understand how different players participate in bringing location applications to market and the importance they add to the value chain. They should understand how location is determined, data are integrated and applications are sold.

LBS Value Chain

Vendors that contribute in the LBS value chain include content providers, application platform vendors, applications and carriers. Content vendors provide a wide variety of data that power LBS applications. Content includes digital maps, weather, points of interest and real-time traffic. LBS application platforms provide development environments and technologies which allow application vendors to provide applications based on location-based services. Mobile LBS applications are prepackaged applications used to serve a specific market need.

Content Vendors. While mobile content and maps are valuable by themselves, the true value of mobile content lies in its integration with other data sources within an application. Mapping data integrated with traffic information and points of interest can lead to powerful navigation applications. By combining data from multiple sources, the resulting value to the user is greater than the sum of the individual parts.

Many of the vendors that offer content for LBS applications also provide content to the Internet and other enterprise applications. Mobile location-based services are becoming a high growth market for content vendors that support location-based services. While the market for mobile content is less developed, the content market that evolved during the Internet era is more established and very incestuous and complex. Vendors have multiple partners from which they will collect data and add value, and then recycle those data back to the originating partner.

Specific content vendors that are powering location-based services include:

Application Platforms. Application platform vendors provide platforms and middleware that usually incorporate APIs to integrate data and content from multiple sources. Application platforms also provide client-side software and Software Development Kits (SDKs) that allow developers to create custom and semi-custom user interfaces.

Beyond development environments, LBS platforms will also provide map rendering, location fixes and management of mapping databases.

Prominent LBS application platforms include: Wavemarket, deCarta, ESRI and Autodesk.

Applications. Application vendors add value to the value chain through their understanding of workflow and business processes in the niches that they serve. The ability to translate those business processes and requirements into mobile software applications is a core competency of application vendors. Leading LBS applications used in the enterprise are: tracking applications that help track assets and workers, and turn-by-turn navigation applications that help workers reach their destination quickly. LBS application vendors that have seen widespread adoption include Networks in Motion (NIM), TeleNav, and Gearworks.

LBS Technologies

The location of a mobile device can be determined in a number of ways. Location can be calculated by the network, the mobile device or a combination of the two.

When a device calculates location on its own, it needs a GPS receiver to communicate with satellites circling the earth. This method is very accurate but it can take time for the device to find and get a fix from the satellites. The device also requires a GPS receiver. When using the network, the location of a device is calculated by determining the location of the base station with which the device is communicating. Although this method (Cell-ID method) can quickly determine location, it can be much less accurate due to the potential size of a cell. Location accuracy provided by the network can be improved by using triangulation and time calculations. These methods are known as E-OTD/U-TDO, or A-FLT.

The assisted GPS location method uses both the wireless network and GPS to determine location. The network communicates the location of the nearest satellite to the device, reducing the time it takes the device to locate a GPS satellite to determine location. This reduces latency and battery drain without sacrificing accuracy.

Business Model and Distribution Channels

Recently carriers have taken a more active role in distributing and marketing LBS applications. The saturation of the wireless voice market has driven carriers to look for new revenue sources; navigation applications and location services are becoming a good revenue source and a driver of wireless data plans.

Revenues generated from navigation applications sold through carriers are shared with the rest of the value chain. Through these partnerships, carriers usually takes 50% of the revenue, content providers get 20-25% and application and platform vendors get 25-30%. An application vendor with a strong brand and reputation will have more leverage at the negotiating table and can demand a higher percentage of the revenue share.

Advertising-based models are also gaining traction in the LBS application market. National brands, portals and media outlets that generate revenues through advertising are providing navigation applications free to their users. Retail advertisers are providing customers with turn-by-turn directions to their storefront in an attempt to drive traffic to the store.

Market Size and Growth

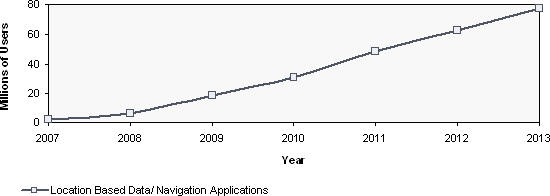

Location-Based Services. In 2007, there were 2.1 million users of mobile location-based service applications and this number is expected to increase at a 53% growth rate, reaching 27.3 million in 2013.

Growth Drivers and Barriers. The growth of location-based services on mobile devices is driven by:

The e-911 rules presented by the FCC require wireless carriers to supply an increasingly accurate location to emergency personnel when a 911 call is made from a mobile phone. The rule mandates an increasing level of accuracy though 2012. To stay in compliance with the rule carriers are increasing their investment in location services.

Enterprise applications are integrating location into their applications and platforms due to the increased ROI it provides. Delivery companies are reducing delivery windows from four to two hours through tracking of vehicles and better management of their fleets. Reducing unauthorized miles is also an important driver for fleet-tracking applications, as costs can reach $2 a mile.

In the construction market, employers can determine where workers are when they are clocking in or out to make sure they are on site when they do so. Applications are also emerging in which workers are automatically clocked in when they are on the job site.

Geofencing and asset-tracking applications are also prominent in the enterprise space. The application will keep track of assets and generate alerts when assets are not where they are supposed to be. One example is the tracking of toxic waste, which has high security requirements.

LBS applications have seen strong adoption and many barriers have been overcome. While enterprises have seen significant ROI from LBS-enabled applications, business processes have not always been redesigned to take advantage of the new technologies. Often employees are not comfortable with their employers tracking their every move and this "big brother" mentality has been a big hurdle for LBS providers. Increasingly LBS vendors are illustrating the benefit of location and tracking to employees. One example is the story of a delivery worker who was trapped in his truck after an accident in a remote location. Dispatchers knew exactly where he was and when he did not check in, they found him and saved his life.

Conclusion

The location-based services market will get more complex and fluid as vendors battle for supremacy in this fast-growing market. While most of the attention will be focused on consumer applications due to the exponential growth rates and large market for generic applications, the enterprise market will also present great opportunities for market participants. Mobile enterprise application vendors will seek ways they can increase the utility of their offerings through the integration of location.

It is important for a supply chain manager to know the drop-off location of a package so that processes and transactions can be completed. This task can be supported by a geofencing application that allows him to determine within which geographic areas the service has been provided and helps ensure that visibility and control are maintained. Giving "road warriors" the ability to seamlessly obtain directions to the next business meeting without even accessing their calendars improves usability. These are examples of how location data are leading to more sophisticated applications and business processes. Location-aware applications will be the norm in the future, and the competition to deliver these services will intensify. New business models and distribution channels will continue to evolve, presenting more dynamic partnership opportunities and go-to-market strategies.

The emergence of location and the ways in which it produces contexts and value when integrated with other data sources are also changing how vendors are deploying mobile applications. Mobile platforms are becoming more flexible and componentized so business process experts can integrate appropriate data to produce solutions that result in tremendous ROI. This decoupling of features and functionality will also lead to delineation in the value chain and vendors will increasingly focus on what they do best.

Market participants need to understand changes in the current value chain and technology in order to make the right decisions today that will position them to take advantage of this growing opportunity. In order to better understand the direction of the market, planners should understand how different players participate in bringing location applications to market and the importance they add to the value chain. They should understand how location is determined, data are integrated and applications are sold.

LBS Value Chain

Vendors that contribute in the LBS value chain include content providers, application platform vendors, applications and carriers. Content vendors provide a wide variety of data that power LBS applications. Content includes digital maps, weather, points of interest and real-time traffic. LBS application platforms provide development environments and technologies which allow application vendors to provide applications based on location-based services. Mobile LBS applications are prepackaged applications used to serve a specific market need.

Content Vendors. While mobile content and maps are valuable by themselves, the true value of mobile content lies in its integration with other data sources within an application. Mapping data integrated with traffic information and points of interest can lead to powerful navigation applications. By combining data from multiple sources, the resulting value to the user is greater than the sum of the individual parts.

Many of the vendors that offer content for LBS applications also provide content to the Internet and other enterprise applications. Mobile location-based services are becoming a high growth market for content vendors that support location-based services. While the market for mobile content is less developed, the content market that evolved during the Internet era is more established and very incestuous and complex. Vendors have multiple partners from which they will collect data and add value, and then recycle those data back to the originating partner.

Specific content vendors that are powering location-based services include:

- Digital map providers - these vendors own databases of digital maps and will license the map information for location-based services. Leading vendors include NAVTEQ and Tele Atlas.

- Traffic data providers - will aggregate and scrub real-time traffic data from multiple sources and provide them to users through wireless data application vendors. Leading vendors include Inrix and Navteq.

- Weather data vendors - will provide real-time weather data collected throughout a wide geographic area. Leading vendors include Weather Bug and Accuweather.

Application Platforms. Application platform vendors provide platforms and middleware that usually incorporate APIs to integrate data and content from multiple sources. Application platforms also provide client-side software and Software Development Kits (SDKs) that allow developers to create custom and semi-custom user interfaces.

Beyond development environments, LBS platforms will also provide map rendering, location fixes and management of mapping databases.

Prominent LBS application platforms include: Wavemarket, deCarta, ESRI and Autodesk.

Applications. Application vendors add value to the value chain through their understanding of workflow and business processes in the niches that they serve. The ability to translate those business processes and requirements into mobile software applications is a core competency of application vendors. Leading LBS applications used in the enterprise are: tracking applications that help track assets and workers, and turn-by-turn navigation applications that help workers reach their destination quickly. LBS application vendors that have seen widespread adoption include Networks in Motion (NIM), TeleNav, and Gearworks.

LBS Technologies

The location of a mobile device can be determined in a number of ways. Location can be calculated by the network, the mobile device or a combination of the two.

When a device calculates location on its own, it needs a GPS receiver to communicate with satellites circling the earth. This method is very accurate but it can take time for the device to find and get a fix from the satellites. The device also requires a GPS receiver. When using the network, the location of a device is calculated by determining the location of the base station with which the device is communicating. Although this method (Cell-ID method) can quickly determine location, it can be much less accurate due to the potential size of a cell. Location accuracy provided by the network can be improved by using triangulation and time calculations. These methods are known as E-OTD/U-TDO, or A-FLT.

The assisted GPS location method uses both the wireless network and GPS to determine location. The network communicates the location of the nearest satellite to the device, reducing the time it takes the device to locate a GPS satellite to determine location. This reduces latency and battery drain without sacrificing accuracy.

Business Model and Distribution Channels

Recently carriers have taken a more active role in distributing and marketing LBS applications. The saturation of the wireless voice market has driven carriers to look for new revenue sources; navigation applications and location services are becoming a good revenue source and a driver of wireless data plans.

Revenues generated from navigation applications sold through carriers are shared with the rest of the value chain. Through these partnerships, carriers usually takes 50% of the revenue, content providers get 20-25% and application and platform vendors get 25-30%. An application vendor with a strong brand and reputation will have more leverage at the negotiating table and can demand a higher percentage of the revenue share.

Advertising-based models are also gaining traction in the LBS application market. National brands, portals and media outlets that generate revenues through advertising are providing navigation applications free to their users. Retail advertisers are providing customers with turn-by-turn directions to their storefront in an attempt to drive traffic to the store.

Market Size and Growth

Location-Based Services. In 2007, there were 2.1 million users of mobile location-based service applications and this number is expected to increase at a 53% growth rate, reaching 27.3 million in 2013.

|

Growth Drivers and Barriers. The growth of location-based services on mobile devices is driven by:

- The success of personal navigation devices (PND)

- The integration of GPS capabilities in mobile devices and the e-911 mandate

- The integration of location and tracking in enterprise applications

The e-911 rules presented by the FCC require wireless carriers to supply an increasingly accurate location to emergency personnel when a 911 call is made from a mobile phone. The rule mandates an increasing level of accuracy though 2012. To stay in compliance with the rule carriers are increasing their investment in location services.

Enterprise applications are integrating location into their applications and platforms due to the increased ROI it provides. Delivery companies are reducing delivery windows from four to two hours through tracking of vehicles and better management of their fleets. Reducing unauthorized miles is also an important driver for fleet-tracking applications, as costs can reach $2 a mile.

In the construction market, employers can determine where workers are when they are clocking in or out to make sure they are on site when they do so. Applications are also emerging in which workers are automatically clocked in when they are on the job site.

Geofencing and asset-tracking applications are also prominent in the enterprise space. The application will keep track of assets and generate alerts when assets are not where they are supposed to be. One example is the tracking of toxic waste, which has high security requirements.

LBS applications have seen strong adoption and many barriers have been overcome. While enterprises have seen significant ROI from LBS-enabled applications, business processes have not always been redesigned to take advantage of the new technologies. Often employees are not comfortable with their employers tracking their every move and this "big brother" mentality has been a big hurdle for LBS providers. Increasingly LBS vendors are illustrating the benefit of location and tracking to employees. One example is the story of a delivery worker who was trapped in his truck after an accident in a remote location. Dispatchers knew exactly where he was and when he did not check in, they found him and saved his life.

Conclusion

The location-based services market will get more complex and fluid as vendors battle for supremacy in this fast-growing market. While most of the attention will be focused on consumer applications due to the exponential growth rates and large market for generic applications, the enterprise market will also present great opportunities for market participants. Mobile enterprise application vendors will seek ways they can increase the utility of their offerings through the integration of location.

From Our Homepage

Saying Farewell to an Amazing Journey

Communicating with Maps

Is There a GIS Career Ladder?

What does it mean to be geospatially smart? Series

Ways Real Estate and Property Developers Utilize Melissa GeoData for Data-Driven Decisions

Unlocking Value From Daily Satellite Imagery and Insights

Maximizing the Value of Your Address Data with Geo Addressing

How Indoor Mapping Enhances the Security of Smart Buildings

Look Ahead: AI, Location Intelligence and Efficiency

Collaboration Takes on Sea Level Rise & Dynamic Technology Environments

Brownies for Brownfields

Has Everything Been Mapped Already?

How Is Data Literacy Changing in an Artificial Intelligence Landscape

Portfolios for GIS Professionals: More Than Just Maps

How to Create a Distance Matrix in QGIS - A Step-by-Step Guide

7 Ideas for Bringing GIS into the K-12 Classroom

The Geography of Movement