While Location Based Services seem to be regarded as the "Next New Thing," it is unclear that LBS will result in "profit" for the majority of the players involved, although it is likely that there will be significant revenues generated by the industry.Let us look at the industry by observing trends in the market and, then, consider the segmentation of the market in order to try to understand the players that might profit as opposed to those who will not profit.

I define LBS as wireless communication technology that combines network services and positioning technology to provide a subscriber with position related services.The service may be available from a mobile handset or other communications device.

Industry Market Overview

Negative Trends

In today's wireless marketplace, voice services are considered a "commodity

business" that do not provide carriers a chance to differentiate themselves.

Next, the rollout of 2G data services has been unsuccessful from a profit

perspective.Finally, there are limited technology standards in the US

market and this situation provokes difficult and costly issues for the

developer community..

Positive Trends

The next generation "always on" networks will provide sophisticated

Location Based Services and faster access speeds.Enhanced devices with

more capable and intuitive user interfaces will become common.Cross carrier,

"push-based" messaging and alerts will be available in the US (Alert services

are available today but not reliably and not cross-carrier).

Future Issues

Carriers are looking to create "stickiness" as a method of monetizing

their wireless infrastructure. Although voice is currently 90% of

wireless carriers' income, it has been forecast that data and other non-voice

services will generate 50% of wireless carrier income by 2005. It

is clear that carriers would like LBS to be an enabler for monetizing their

wireless infrastructure. However, the push towards 3G services is

moving forward with limited standardization. Ninety percent of the

3G licenses awarded will use some form of WCDMA as core technology while

during the 20003-2005 timeframe, TDMA/GSM/WCDMA terminals will account

of over 60% of the global market place.

Changing Technology

One of the major obstacles to successfully monetizing the wireless

infrastructure is that those desiring to provide data services and other

non-voice services must support myriad technology.

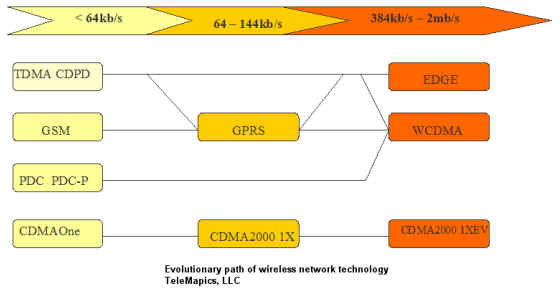

It is clear that there will be significant change in wireless network

technology over the next three to five years.

The issue of wireless networking technology converts to the following carrier

adoptions:

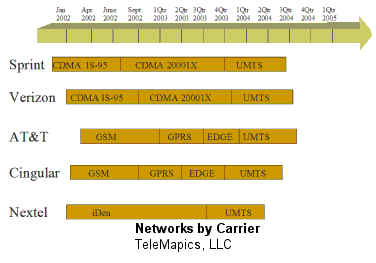

The issue of wireless networking technology converts to the following carrier

adoptions:

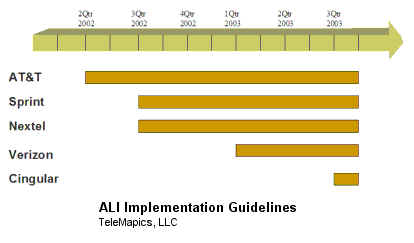

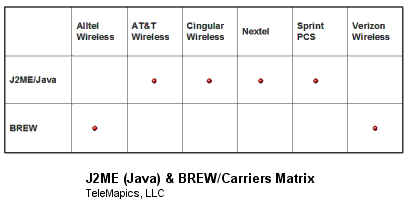

Next, LBS depends on ALI implementation:

Next, LBS depends on ALI implementation:

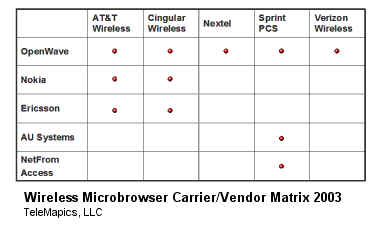

Developing LBS, also, will depend on supporting various micro-browsers:

Developing LBS, also, will depend on supporting various micro-browsers:

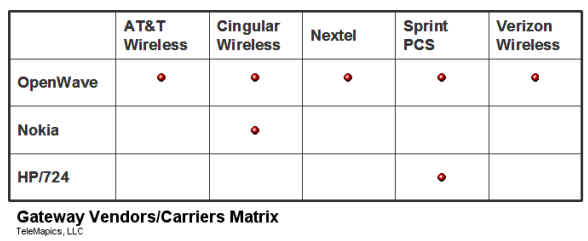

Next, LBS implementations will be influenced by development platforms and

Gateways:

Next, LBS implementations will be influenced by development platforms and

Gateways:

Additionally, it is somewhat disconcerting to consider that supplier must

consider the diversity of individual phones and complications

related to the fact that application bug fixes are often device specific

(client side) and may need to be applied at the phone level (raising

the need to support server side and device resident applications).

Additionally, it is somewhat disconcerting to consider that supplier must

consider the diversity of individual phones and complications

related to the fact that application bug fixes are often device specific

(client side) and may need to be applied at the phone level (raising

the need to support server side and device resident applications).

It is clear that the diversity of technology comprising the wireless infrastructure supporting the carriers' platforms provokes the need for those working in LBS to develop and support a complex, service provider environment. These development and support expenses are continuing obligations that spiral as your application supports more carriers. Unfortunately, having more customers does not guarantee that you have more income as development and support costs may exceed the compensation offered by the carrier. While this sounds counter intuitive, you should consider that most carriers operate a "walled garden" Internet and unless you are inside of their walls, you do not receive any visitors. Finally, it is important to note that carriers, today, are attempting to provide increasingly services based on proprietary offerings. Providers with unique services are being pushed to the periphery of the Wireless Web.

How Will the Game Play Out?

It is clear that the carriers will generate substantial revenue from

LBS services due to their role as infrastructure providers (and gatekeepers).

Whether or not the carriers will generate profit is unclear due to the

financial issues relating to the acquisition of spectrum and providing

a reliable infrastructure that must operate under significant government

oversight and regulation.

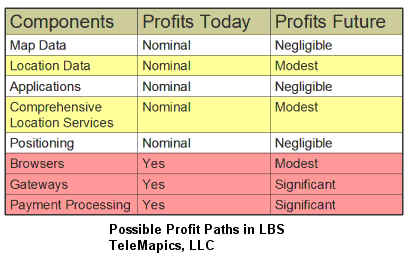

Who else will make money in LBS, and of those, will anyone make a profit?

Based on our familiarity with LBS, Wireless and Technology, TeleMapics

offers the following chart, presenting our best estimates of where the

"money will flow in LBS":

It is TeleMapics position that the "take off" of LBS services will be slow

and complicated by the fact that Carriers are not presently prepared to

sell LBS (ask a carrier's sales representative to explain how to use the

wireless Internet to gain some understanding of the scope of this problem).

Next, although it was believed that applications involving safety would

lead the market, there has been some reconsideration of this assumption

based on the poor renewal rate for GM's OnStar service (which has been

characterized by consumers as a safety based service).Also, the assumption

that LBS "push-based" services would be attractive to consumers has been

reconsidered as a "marketing idea gone bad". Further, today's LBS

applications are "clumsy" and location data (not map data) are so poor

in quality that LBS is dismissed by consumers as ineffective. Although

early adopters and "True Believers" love LBS, the size of these groups

does not constitute a mass market capable of generating sustainable, profit-based

growth.

It is TeleMapics position that the "take off" of LBS services will be slow

and complicated by the fact that Carriers are not presently prepared to

sell LBS (ask a carrier's sales representative to explain how to use the

wireless Internet to gain some understanding of the scope of this problem).

Next, although it was believed that applications involving safety would

lead the market, there has been some reconsideration of this assumption

based on the poor renewal rate for GM's OnStar service (which has been

characterized by consumers as a safety based service).Also, the assumption

that LBS "push-based" services would be attractive to consumers has been

reconsidered as a "marketing idea gone bad". Further, today's LBS

applications are "clumsy" and location data (not map data) are so poor

in quality that LBS is dismissed by consumers as ineffective. Although

early adopters and "True Believers" love LBS, the size of these groups

does not constitute a mass market capable of generating sustainable, profit-based

growth.

Finally, LBS services will suffer from confidentiality issues and this concern will further impede the market. The success of the industry requires that customers believe confidentiality is not a problem. Today, the majority of consumers are uneasy about possible extension of LBS to "surveillance databases"

What Might Change the Outlook for Profitability in LBS?

- Profitability in the market for LBS could change in an instant, if existing Yellow Page Companies were to embrace LBS. These companies have successful franchises that include location information. They, also, have viable sales channels. Unfortunately, most of the existing Yellow Page companies are wary of the Wireless Internet, as it is considered a distraction from today's exceptionally robust revenue stream.

- Today's LBS solutions amplify the center and leave the periphery unacknowledged. Adding location information surrounding a person's position is similar to providing peripheral vision to a person who has been limited to seeing with tunnel vision. At TeleMapics, we feel that the possibility of creating "knowledge ecologies" may make LBS a desired application, particularly if a method is developed to transfer to LBS the information contained in "Community Based Knowing".

- Finally, it is possible that the simultaneous voice and data capabilities of 3G networks will allow voice interrogation to be coupled with visual inspection of "pick lists, solving the difficult problem of searching for location targets presented on phone based systems.

In order to create a profitable LBS industry, the players need to develop an inviting and invisible technology. There is a need to create LBS that help make sense of the surrounding world when our customers require this type of help.

(This paper was based on a presentation delivered at a Special Session

of the World Congress on Intelligent Transportation Systems in October

2002. Michael L.Sena of Michael L.Sena Consulting AB [ml.sena@mlscab.se]

graciously arranged the Special Session)