EU Space Market Report Maps Growth Across Europe’s Downstream Sector

The latest EU Space Market Report is now out, and it pulls the European Union’s downstream space picture into one view. Published by the European Union Agency for the Space Programme, the update tracks how GNSS, Earth observation, secure satellite services, and related technology are shifting the market in Europe and beyond. It also frames the market at a broader level, with downstream activity expanding across multiple user sectors as demand for positioning, imaging, and secure connectivity keeps rising.

For the first time, the report places GNSS alongside EO, Secure SATCOM, and SSA in one document. That makes the read more useful from a systems angle. I went through the structure much like a GIS overlay, and the value is in seeing where one capability starts reinforcing another rather than treating each satellite service as a separate layer.

According to EUSPA, the publication brings together current developments, emerging trends, and the market dynamics shaping the global downstream ecosystem. It also looks at how user technology is evolving, including cleaner system design and newer commercial initiatives, and why stronger synergy between these areas matters for infrastructure, policy, and Europe’s strategic autonomy.

Rodrigo da Costa, EUSPA executive director, said Europe needs to stop viewing its space capabilities as isolated tools as links between them deepen.He said the report reflects the rising strategic weight of these domains for the European economy, resilience, and autonomy.

He said the report reflects the rising strategic weight of these domains for the European economy, resilience, and autonomy.

Da Costa added that EUSPA wants the broader view of the space ecosystem to support innovation, improve cooperation across the sector, and help build a more competitive and responsive European Union space economy. In practice, EUSPA’s role includes market monitoring and programme uptake support across EU space services, while also helping connect public demand with commercial use.

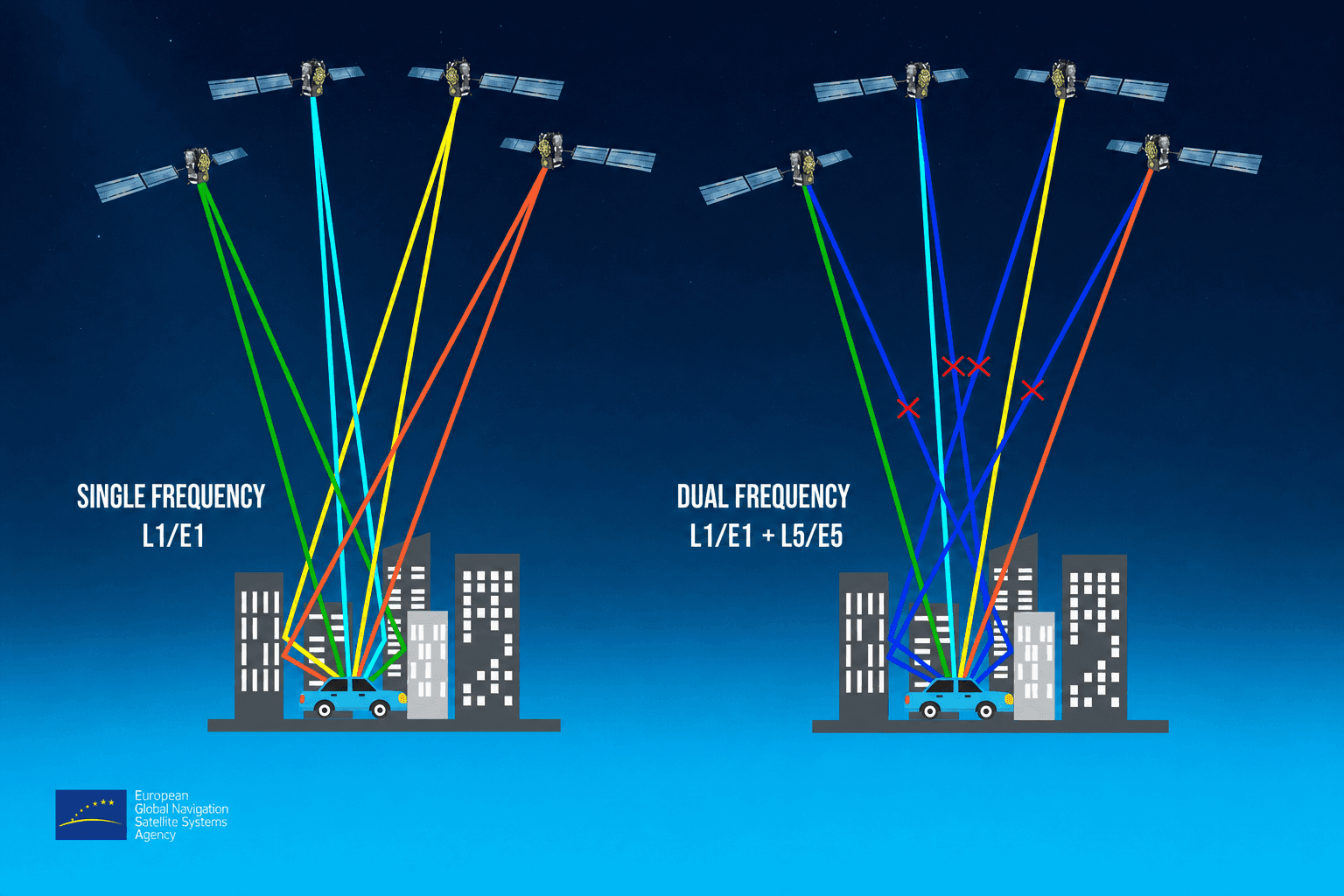

GNSS and EO

The report points to continued expansion in both satellite navigation and Earth observation across all 16 market segments under review, though this summary does not break out every segment one by one. In EO, revenue is estimated at €3.5 billion in 2024 and is projected to reach €7.9 billion by 2034. Agriculture holds the biggest share, which fits with how Earth data keeps moving into everyday decision systems on the ground.

For GNSS, revenue is expected to grow from €300 billion in 2024 to €580 billion by 2034. EUSPA says service revenue is rising faster than device revenue, which suggests that the real value is increasingly tied to data services and digital ecosystem layers rather than hardware alone.

| Segment | 2024 Revenue | 2034 Revenue | 2040 Revenue |

|---|---|---|---|

| EO | €3.5 billion | €7.9 billion | - |

| GNSS | €300 billion | €580 billion | - |

| Secure SATCOM data services | - | - | Almost €1.2 billion |

Most of that income still comes from consumer uses and the road sector. The installed base of GNSS-enabled devices worldwide is forecast to approach 10 billion by 2034, a scale that underlines how deeply GPS-style positioning is now woven into the broader economy.

Secure SATCOM

The Secure SATCOM segment is centered on surveillance, critical infrastructure, and crisis response. In this market, data service revenue generated by EU users is expected to climb from above €200 million in 2025 to almost €1.2 billion by 2040.

Early demand is led by maritime surveillance in 2025. By 2040, the report expects activity to shift toward law enforcement operations and civil protection. That change is tied to stronger security requirements and more reliance on dependable connectivity.

Existing and Future Synergies

The report also looks at how large external pressures are reshaping the space market. Two of the clearest growth drivers are climate stress and geopolitical tension, both of which are pushing closer links between EO and GNSS, with Secure SATCOM adding resilience where continuity matters. On the restraint side, the picture is tighter budgets and more complex security demands, which can slow deployment even as demand rises.

Taken together, these capabilities are becoming more important for environmental monitoring and disaster response, while also supporting smarter management of urban systems and infrastructure.

Launch Market Questions Around Europe

The report is focused on the downstream market, so it does not serve as a full guide to European space launch services. Still, the wider competitive picture is easy to read. Europe has opportunities in sovereign access and in launch support for institutional missions, while the harder side is cost pressure and a more crowded global field.

That also shapes how Europe competes globally in launch services. Its strengths are public programme backing and a deep industrial base. Its weaknesses are slower market response and less pricing flexibility than some rivals.

ESA remains central to that wider space economy even beyond launches. Its economic impact shows up through programme funding and industrial coordination, helping sustain capabilities that feed commercial activity across Europe.

Where to Find the Full Report

The document is available from EUSPA through its publications and market report pages. Related material, including programme updates and supporting documents, is usually published in the same EUSPA resource area, alongside European Commission space policy material.