Mid- And High-precision Gps Receiver Market Heads For Strong Growth

No audio is available for this content.

Demand for mid- and high-precision GPS receivers is moving up quickly, with broader use across surveying, construction, agriculture, and transport. The core picture is straightforward - advances in satellite navigation technology and wider deployment of automation are pushing this market into a stronger growth phase, according to our research.

Forecast Points to a Much Larger Market by 2030

The report says the market for these Global Positioning System and GNSS devices could reach USD 6.85 billion by 2030, rising at a compound annual growth rate of 12.2%. Growth over the period is tied to better support for autonomy in vehicles and machine control. It is also being lifted by smart infrastructure work, along with the spread of precision agriculture and more accurate mapping tools.

From what I have seen in geospatial hardware cycles, that kind of expansion usually shows up when field accuracy improves enough to move from specialist use into daily operations. That appears to be happening here, helped by stronger GNSS correction services and better positioning reliability.

The market still faces some clear restraints. High equipment costs can slow adoption, and performance can still suffer in difficult signal environments or where correction coverage is limited. Supply chain pressure and certification requirements also remain part of the commercial picture.

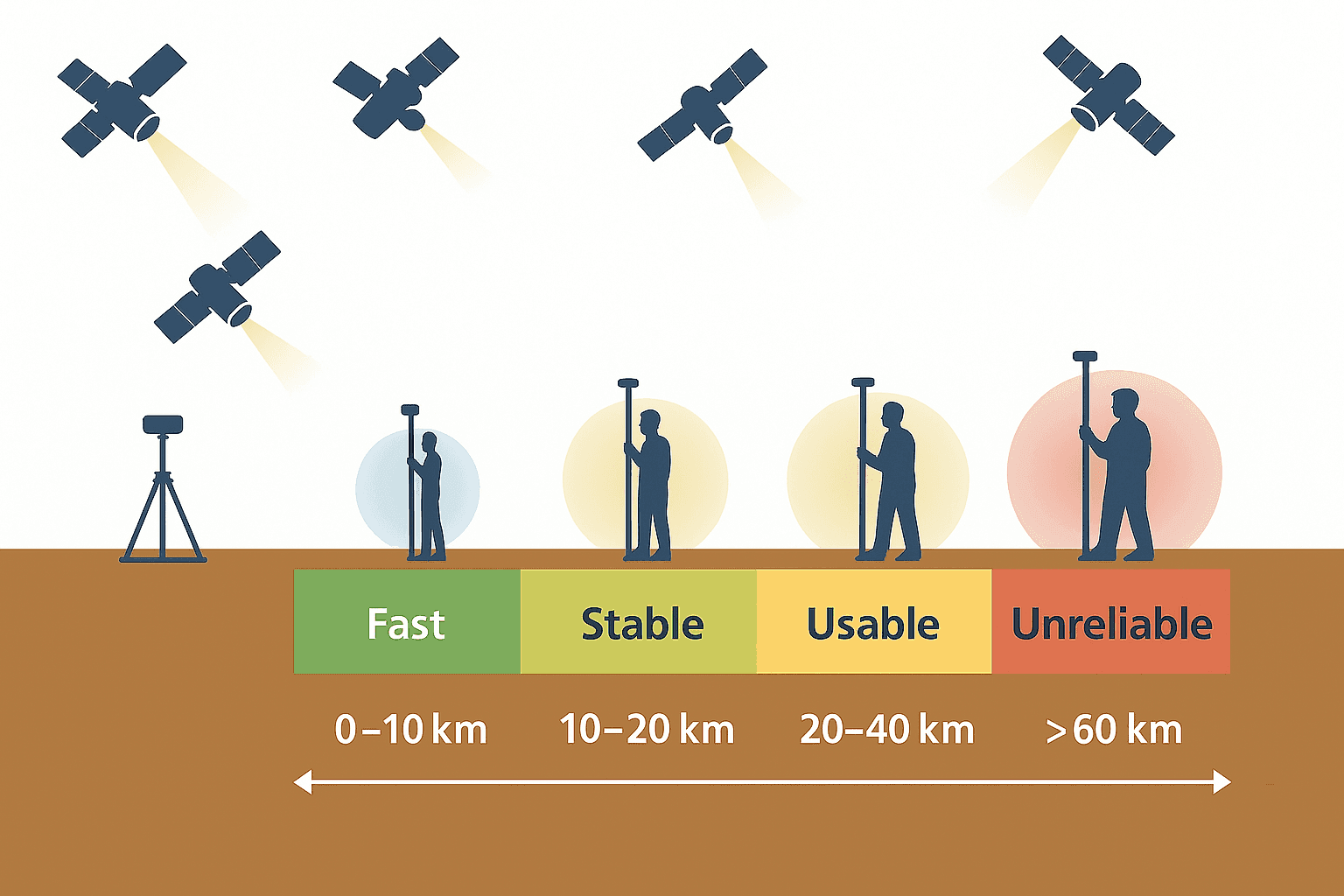

Technology Trends Shaping Receiver Demand

Several technical shifts are helping define the market landscape. One is the push toward centimeter-level accuracy and precision, which matters in surveying, fleet management, and self-driving car systems. Another is the tighter use of RTK and PPK methods, along with multi-frequency signal processing that improves performance when satellite signal conditions are rough.

The report also highlights better alignment with survey software and continued gains in GNSS mapping precision. I read that a bit like checking a coordinate system against a base layer - the hardware matters, but the real value shows up when data lines up cleanly inside working software.

Recent development is also leaning toward smaller modules and tighter links with cloud platforms. That matters because field teams increasingly want receivers that can pass correction data and status information into connected software without much delay.

A free sample of the report is available.

How the Market Is Commonly Segmented

This market is usually broken down by receiver type, application, technology, and end-user. Type splits generally separate mid-precision units from high-precision units. Application coverage centers on field measurement work and machine-guided operations, while technology discussions usually focus on standalone GNSS capability or receivers paired with correction methods such as RTK. End-user demand is most visible in surveying groups and industrial equipment operators.

When I mapped this out, the pattern looked fairly clear - the higher the accuracy requirement, the more the buying decision shifts toward correction support and software compatibility.

Competitive Landscape Includes Established GNSS Suppliers

The sector includes a wide mix of recognized manufacturers and technology firms. A practical way to read the field is by focus rather than by a long vendor roll call.

| Company Name | Key Offerings | Market Focus |

|---|---|---|

| Trimble Inc. | High-precision GNSS hardware and field software | Surveying and construction |

| u-blox AG | GNSS modules and positioning technology | Industrial and automotive uses |

| Hexagon AB | Geospatial instruments and positioning systems | Mapping and industrial workflows |

| Hemisphere GNSS | Receivers, antennas, and correction services | Agriculture and marine positioning |

The sector includes a wide mix of recognized manufacturers and technology firms. Among the better-known names are StoneX Group Inc., Raytheon Technologies Corporation, Hexagon AB, Trimble Inc., and u-blox AG. The broader field also includes Leica Geosystems, NovAtel Inc., Satlab Geosolutions, ComNav Technology Ltd., Tersus GNSS, Geneq Inc., Eos Positioning Systems, NavtechGPS, Thales Group, and Hemisphere GNSS.

The article does not provide market share rankings, so the leading names are best understood as established participants rather than a confirmed top-to-bottom order. Even so, competition appears to be shaped by product integration and by moves to strengthen correction capability or industry-specific positioning tools.

That spread of vendors says a lot about the market itself. It touches geospatial research, agricultural machinery, heavy equipment, and the automotive industry, while also feeding data-heavy uses tied to software, cloud computing, and the internet of things.

Regional Demand and Market Share Patterns

Regional leadership is usually strongest in North America and Asia-Pacific, where demand is supported by precision agriculture, infrastructure work, and vehicle technology programs. Europe also remains important because of its established geospatial and industrial equipment base.

Regional dynamics differ in a fairly practical way. Mature markets tend to buy for upgrade cycles and tighter automation needs, while faster-growth markets are helped by wider infrastructure buildout and expanding adoption of positioning tools in the field.

CNH Industrial Expanded Its Position Through Acquisition

One notable deal came in March 2023, when Netherlands-based CNH Industrial N.V. acquired Hemisphere GNSS for USD 175 million. CNH Industrial works across agricultural and construction equipment, with a strong focus on automation and machine management, so the purchase fits the direction of the wider market.

The aim was to bring Hemisphere GNSS receiver technology and satellite-based correction capability into CNH Industrial systems to improve positioning, autonomy, and machine control in construction and agriculture. Hemisphere GNSS, based in the United States, supplies advanced GNSS receivers and antennas, along with correction services for uses that include surveying and marine operations.

Product Launches Show Where Innovation Is Heading

Leading companies are still bringing out new hardware to hold their position. In October 2026, Unicore Communications Inc. of China launched the UM98XC Series, a next-generation multi-frequency RTK GNSS module built for all-constellation support.

The module works with major satellite systems and supports correction services designed for high-accuracy positioning. According to the product description, it delivers centimeter-level positioning and adds anti-jamming protection. That combination makes it a practical fit for autonomous driving and precision agriculture.

This release highlights Unicore Communications' push to improve GNSS accuracy, reliability, and scale for industrial equipment and vehicle applications.

Selection Factors and Outlook

Key selection criteria usually come back to a short set of practical checks. Buyers tend to focus first on accuracy and correction compatibility, then on reliability in real field conditions. Cost still matters, but software fit and support quality can carry just as much weight once a receiver is in daily use.

COVID-19 disrupted production schedules and hardware supply early on, which created delays for some buyers and projects. At the same time, demand tied to automation and remote field operations helped keep longer-term interest in precision positioning technology intact.

The broader outlook still points upward. Growth opportunities are most visible where automation systems need dependable positioning and where software-connected field equipment becomes standard practice.