How Much Taxes Do You Pay on Crypto? 2026 Guide to Reporting, Rates, And Rules

Wondering what you’ll owe in crypto taxes? Calculating digital asset taxes can be tougher than it looks. Many traders underestimate the tax liabilities created by swaps, sales, and rewards, and the IRS has intensified enforcement, so it pays to know the rules.

Feeling overwhelmed by cryptocurrency tax rules? You’re in the right place.

Gordon Law Group is a top crypto tax practice. Since 2014, we’ve prepared more than 1,500 cryptocurrency reports. With both cryptocurrency accountants and crypto tax attorneys under one roof, we make filing fast, precise, and stress-free.

Whether you’re brand-new or a veteran investor, this guide breaks down how crypto is taxed and how to report cryptocurrency on your tax return.

Do I Need to Report Crypto on My Taxes?

Yes. For federal tax purposes, the IRS treats Bitcoin, Ethereum, and other crypto assets as property. Every disposal or receipt—selling, trading, spending, or earning—may create a reportable event. Even if you lost money, you should include all crypto activities to avoid IRS trouble.

There is no general “under $600” exception for reporting crypto disposals. Even small trades, conversions, or purchases made with crypto can create a taxable capital gain or loss that belongs on your return. Separately, simply holding crypto (with no selling, swapping, spending, or earning) generally does not create tax due—but you still need to answer the virtual currency question on Form 1040 accurately based on what you did during the year. And if you received crypto as income (for example, staking rewards or payment for services), it is generally reportable even if the total is under $600.

Important Changes to Crypto Tax Rules in 2025

Starting in January 2025, major changes began reshaping digital asset reporting. Here are the essentials:

- Form 1099-DA: U.S. crypto platforms must track activity beginning January 1, 2025, and send the new Form 1099-DA for digital assets.

- Cost Basis Method: Before 2025, many used a universal method. From January 1, 2025, a wallet-by-wallet approach replaces it.

- Transferring Crypto: Traditional brokers share cost basis and holding periods when you move stocks. A similar standard is coming for crypto, but for now, you must track your own self-transfers to preserve accurate basis.

- Catching Up Matters: Bring prior-year crypto filings up to date now. You’ll need clean historical data to prepare the current year and to avoid becoming a cautionary IRS example.

- Evolving Regulations: Rules are likely to continue shifting under a comparatively crypto-friendly Trump administration. Monitor tax updates, seek professional advice, and consider extending your filing deadline when appropriate.

How Is Crypto Taxed?

Crypto is taxable. The IRS taxes it as property, like stocks, so you generally face two categories of tax:

- Tax on capital gains from trades, sales, or other disposals

- Ordinary income tax on rewards and earnings

This framework applies to Bitcoin, altcoins, NFTs, stablecoins, and other digital assets.

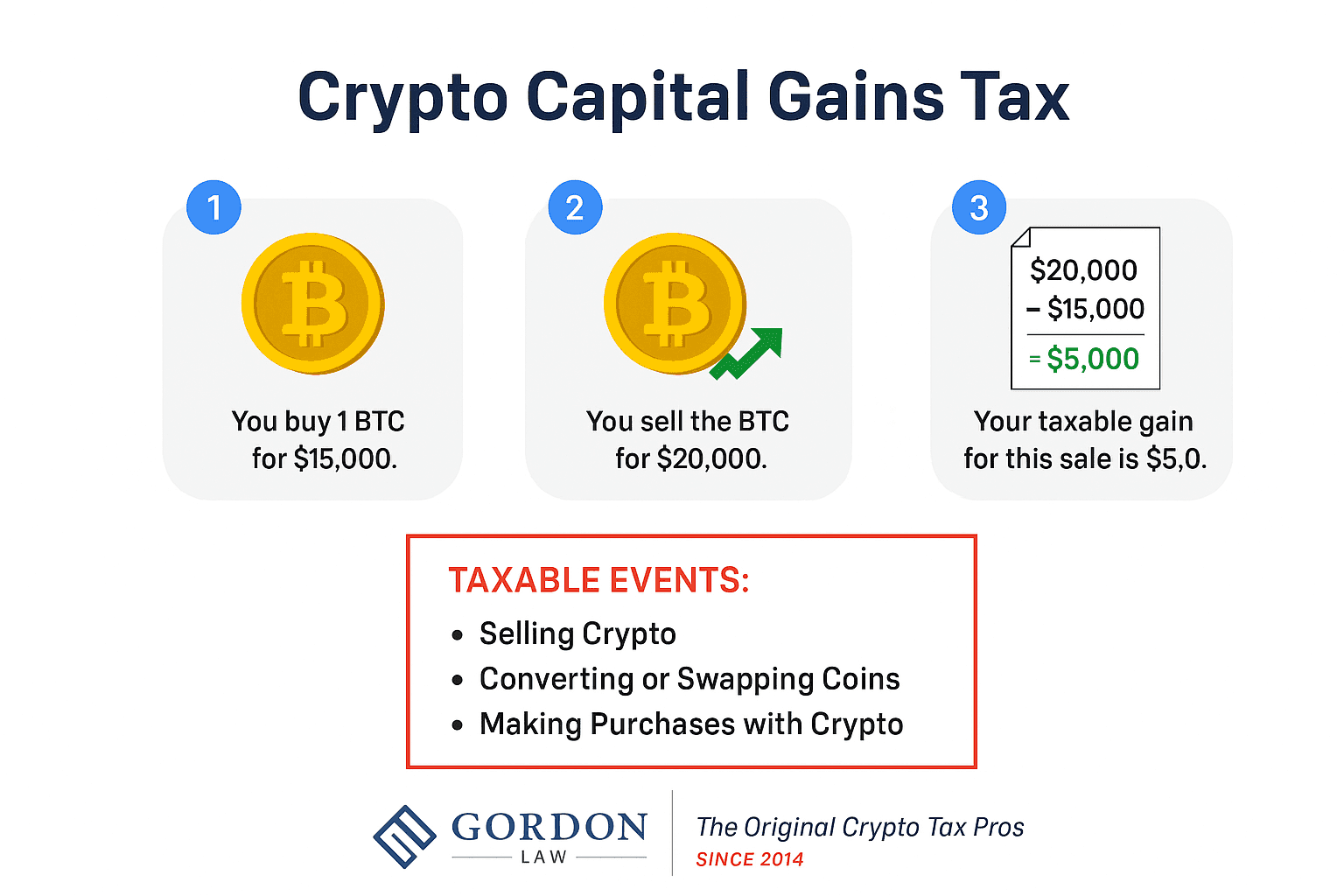

Crypto Capital Gains Tax

When you sell or swap cryptocurrency, any profit above your cost basis is a capital gain and is taxable. If your value decreased, you may have a capital loss.

The rate depends on how long you held each lot before disposing of it.

- Short-term gains: Assets held for one year or less. Taxed at your regular federal income bracket (about 10%–37%).

- Long-term gains: Assets held for more than one year. Taxed at 0%, 15%, or 20% based on your income level.

- Capital gain or loss equals sales proceeds minus cost basis. You must compute this for each individual crypto disposal, which is why reporting can be tedious.

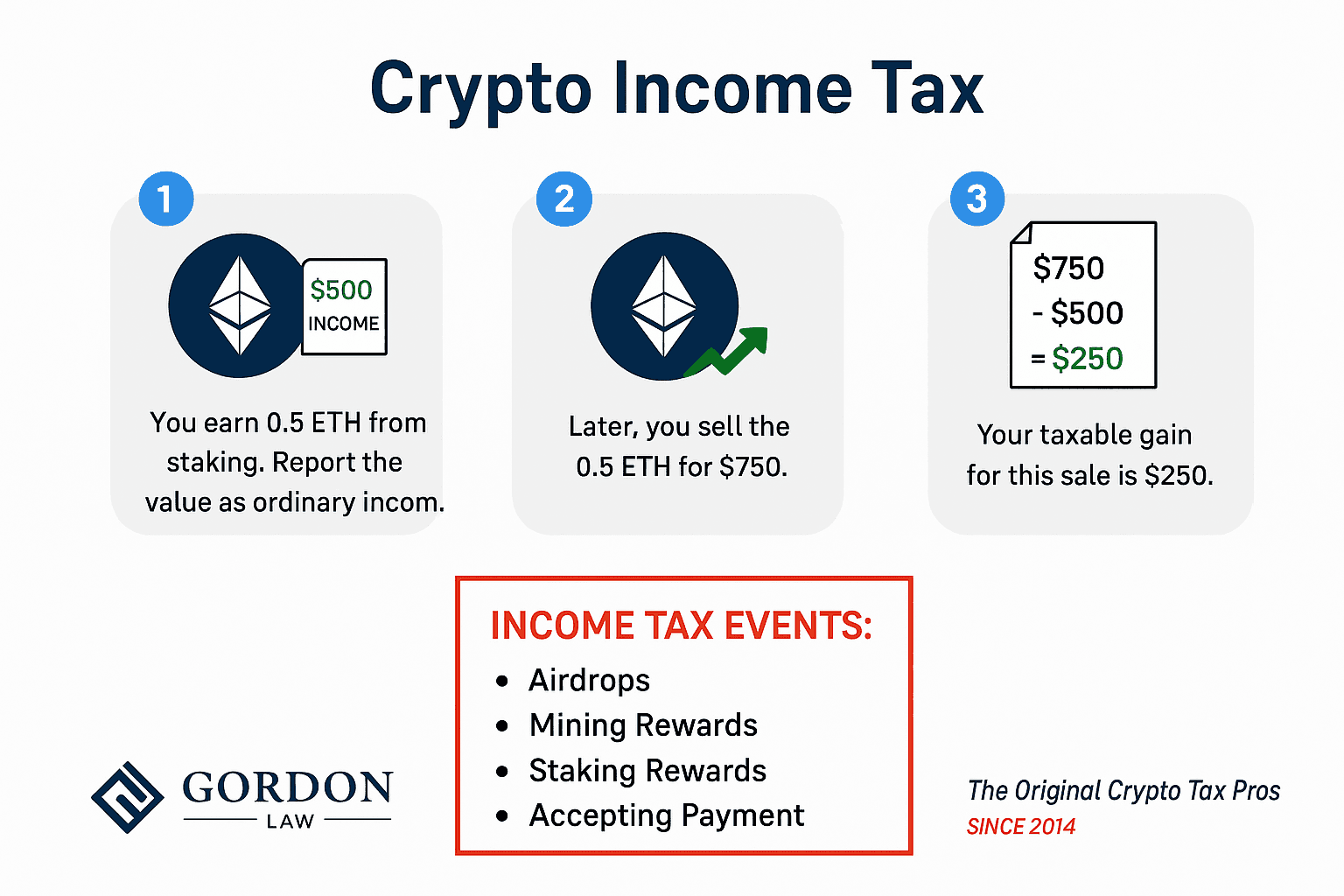

Crypto Income Tax

Income tax applies when you receive crypto other than by purchasing it. Common examples include payment for goods or services, mining, staking, interest, or other rewards. The amount is taxed like wages at ordinary income rates (roughly 10%–37%).

Report the fair market value in U.S. dollars at the moment you receive the asset.

Example: You earn 0.5 ETH from staking when ETH is priced at $1,000. You would recognize $500 of income.

If you later sell, trade, or spend those coins, that triggers a capital gain or loss. Your cost basis is the income you recognized—in this example, $500 for the 0.5 ETH.

What Is the Crypto Tax Rate?

Your crypto tax rate depends on filing status, income, and the nature of the transaction. Short-term capital gains and ordinary income are taxed at regular federal brackets (about 10%–37%). Long-term capital gains use preferential 0%, 15%, or 20% bands.

Crypto Tax Rates for Short-Term Capital Gains and Ordinary Income (Tax Year 2026)

These brackets apply to:

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 10% | $0–$11,600 | $0–$23,200 | $0–$11,600 | $0–$16,550 |

| 12% | $11,601–$47,150 | $23,201–$94,300 | $11,601–$47,150 | $16,551–$63,100 |

| 22% | $47,151–$100,525 | $94,301–$201,050 | $47,151–$100,525 | $63,101–$100,500 |

| 24% | $100,526–$191,950 | $201,051–$383,900 | $100,526–$191,950 | $100,501–$191,950 |

| 32% | $191,951–$243,725 | $383,901–$487,450 | $191,951–$243,725 | $191,951–$243,700 |

| 35% | $243,726–$609,350 | $487,451–$731,200 | $243,726–$365,600 | $243,701–$609,350 |

| 37% | $609,351+ | $731,201+ | $365,601+ | $609,351+ |

Crypto Tax Rates for Long-Term Capital Gains (Tax Year 2026)

These thresholds apply to crypto held for more than one year.

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | $0–$47,025 | $0–$94,050 | $0–$47,025 | $0–$63,000 |

| 15% | $47,026–$518,900 | $94,051–$583,750 | $47,026–$291,850 | $63,001–$551,350 |

| 20% | $518,901+ | $583,751+ | $291,851+ | $551,351+ |

Example (simplified): If you have a $300,000 long-term crypto gain and (for illustration) that gain is your only taxable income, a Single filer would pay 0% on the first $47,025 and 15% on the remaining $252,975, for about $37,946 of federal long-term capital gains tax. Under the same simplified assumptions, Married Filing Jointly would pay 0% on the first $94,050 and 15% on the remaining $205,950, for about $30,893.

If that same $300,000 is short-term gain (taxed like ordinary income), and (again for illustration) it is your only taxable income, a Single filer would owe about $75,375 in federal tax using the 2026 brackets, while Married Filing Jointly would owe about $58,085. Actual tax can be higher or lower depending on total income, deductions, other capital gains, and state taxes.

Which Crypto Transactions Are Taxable?

Most cryptocurrency transactions are taxable. It’s not limited to cashing out to dollars—using crypto to buy goods or services, or trading one token for another, can also create a reportable event.

The following activities generally result in capital gains or losses:

- Selling crypto for U.S. dollars or other fiat

- Converting or swapping one token for another

- Paying for goods or services with digital assets

- Trading cryptocurrency for NFTs or vice versa

The following are typically taxed as ordinary income:

- Mining or staking rewards

- Airdrops

- Compensation paid in cryptocurrencyInterest, yield, or other reward programs

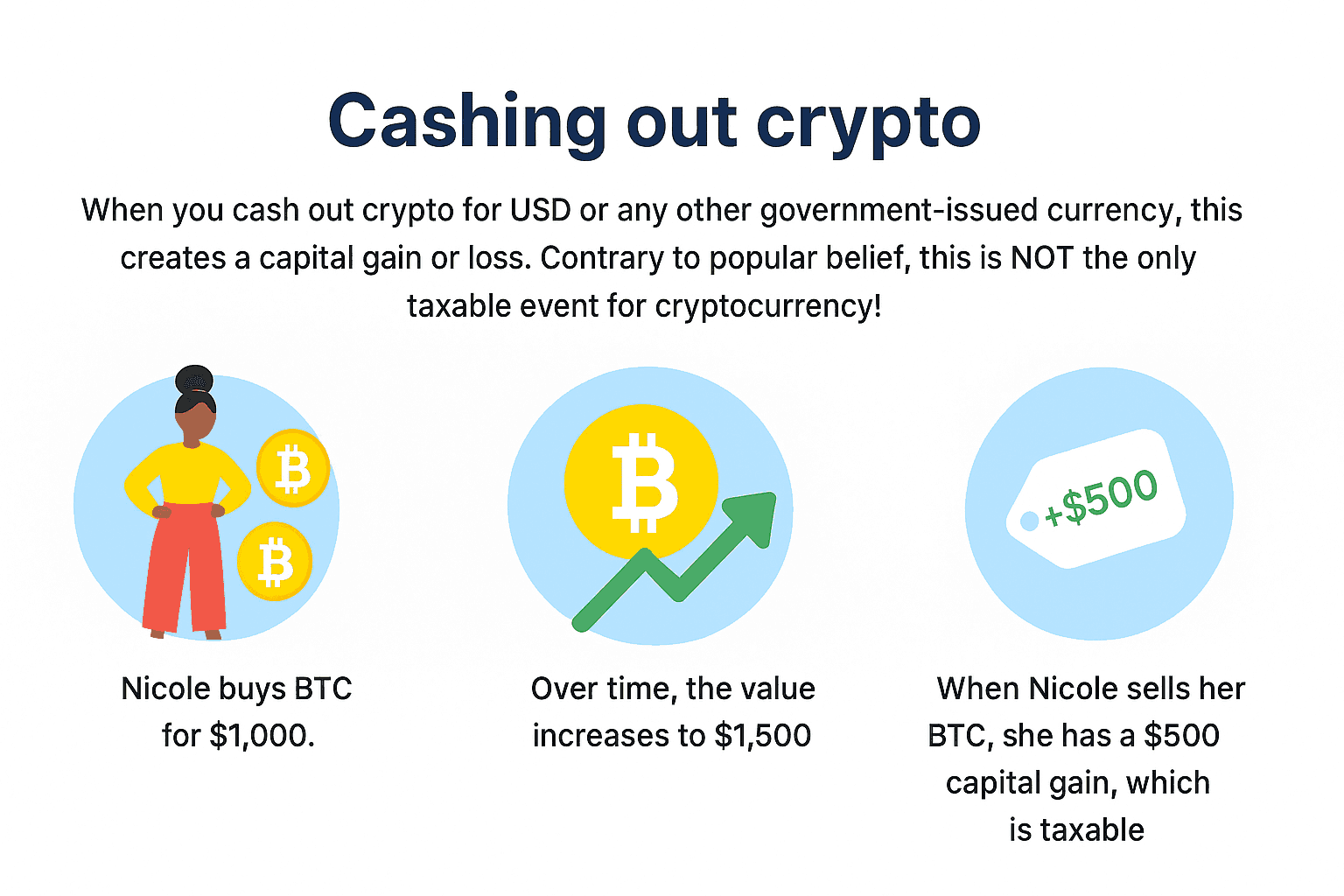

Do You Pay Tax When You Cash Out Crypto?

Yes. Exchanging crypto for U.S. dollars (or any fiat currency) is a taxable disposal that can produce a capital gain or loss.

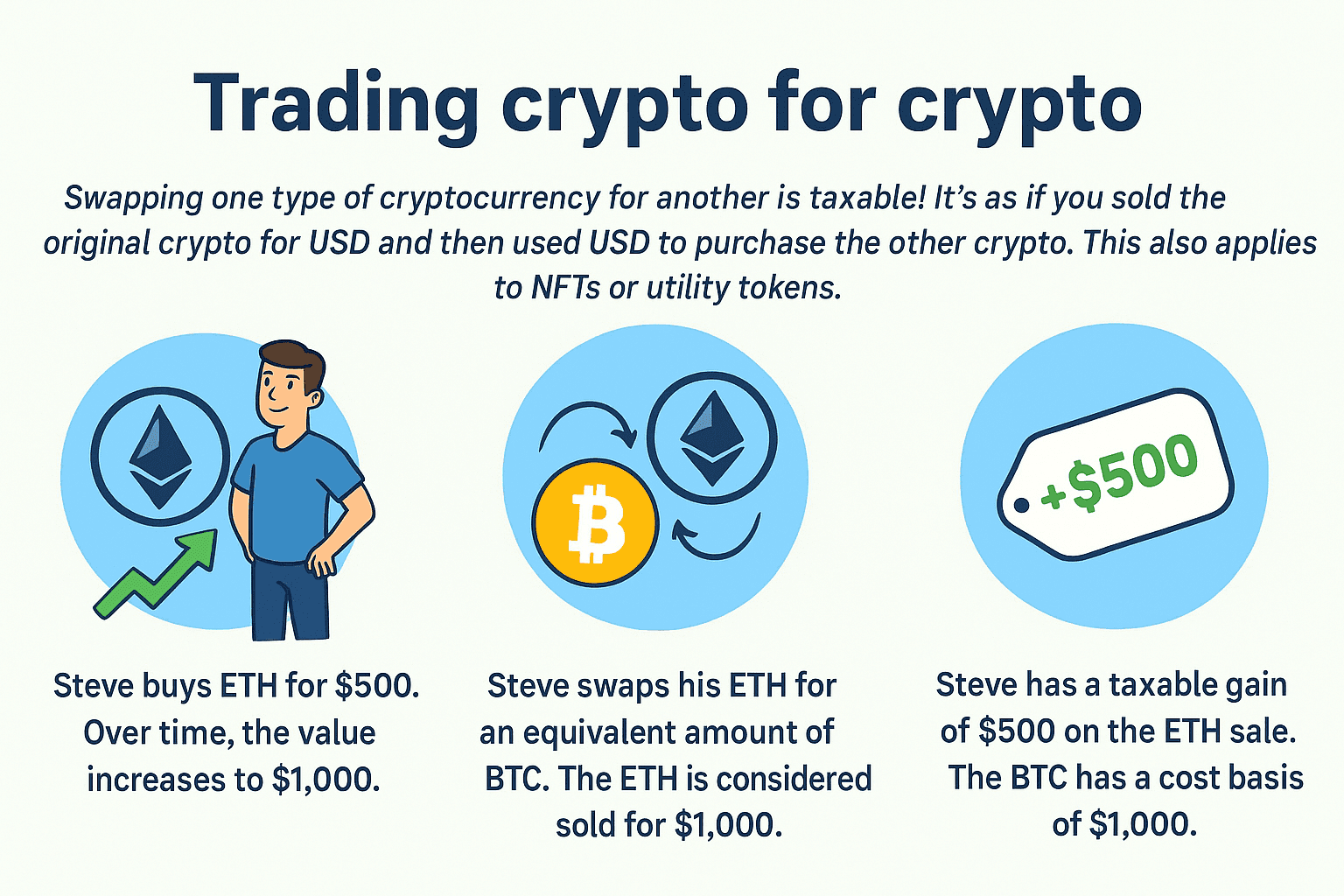

Is Converting Crypto a Taxable Event?

Yes. Swapping one coin or token for another—such as trading ETH for ADA—is treated as if you sold the first asset for dollars and immediately purchased the second, creating a taxable event.

The same applies to stablecoins like USDC. Many investors mistakenly assume crypto-to-crypto conversions are tax-free, but they are not.

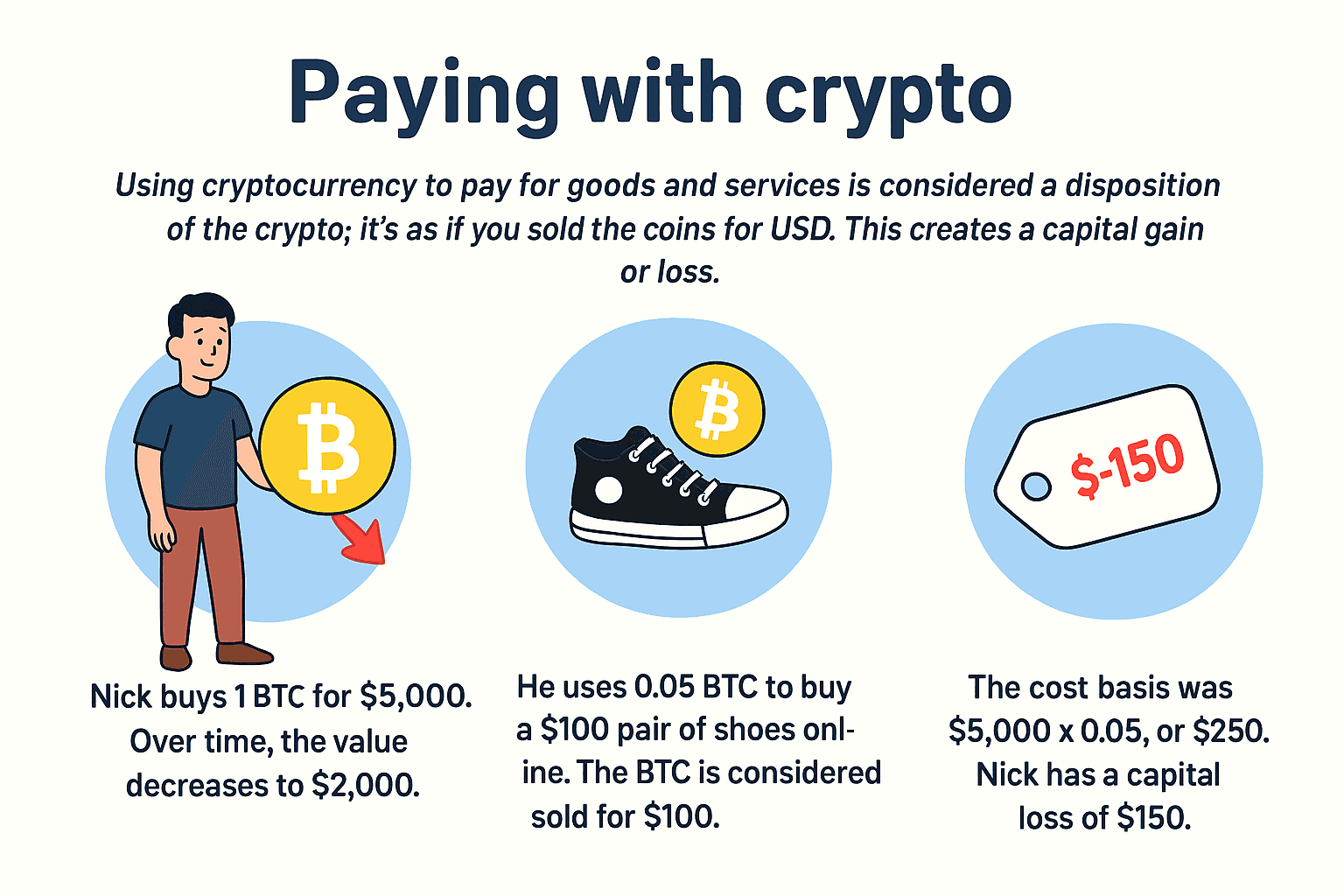

Is Paying With Crypto Taxable?

Yes. Spending crypto is a disposal. Whether you buy services, physical goods, NFTs, or anything else, paying with tokens can generate a capital gain or loss.

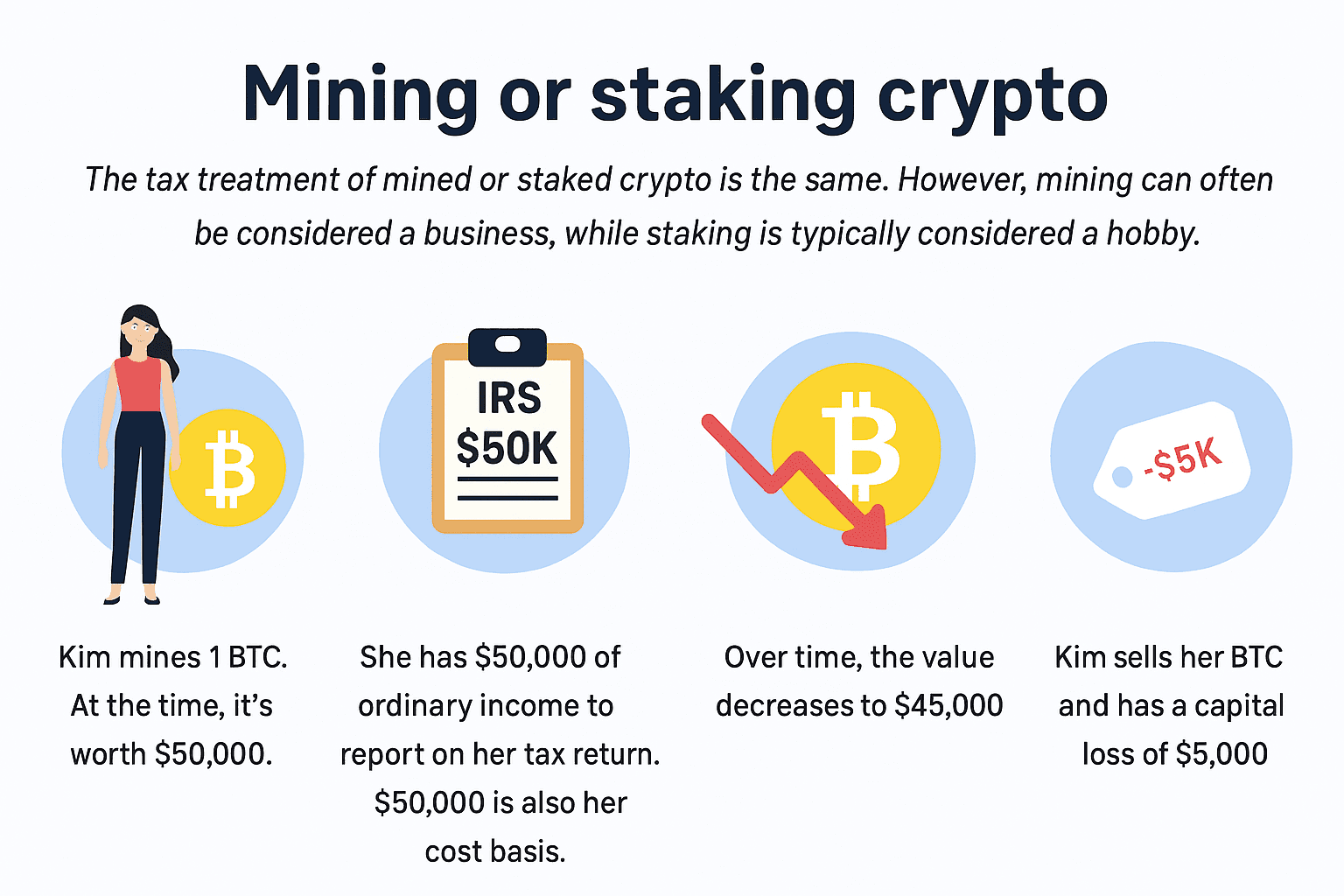

Are There Taxes on Crypto Mining?

Mining rewards are typically ordinary income. In many cases, mining is treated as a business, allowing you to deduct qualified business expenses. Learn the rules before filing to capture the right deductions.

Are Crypto Staking Rewards Taxable?

Yes. Staking rewards are generally treated as miscellaneous or other income rather than business income, which typically means no business deductions. Track the fair market value at receipt.

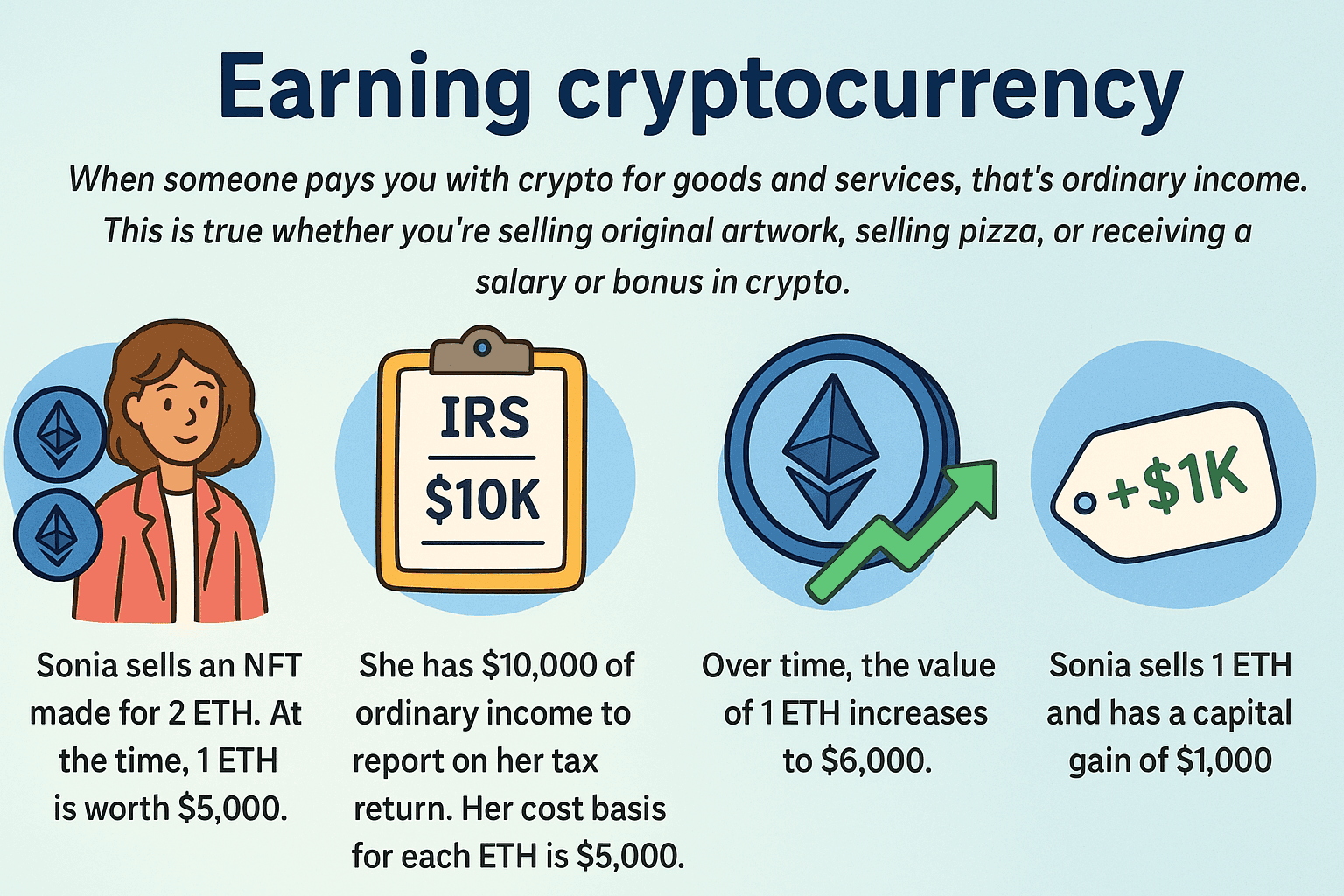

Are There Taxes When You Get Paid in Crypto?

Compensation in cryptocurrency is ordinary income. This applies to sales of original NFTs, services, goods, and wages or bonuses paid in tokens by an employer.

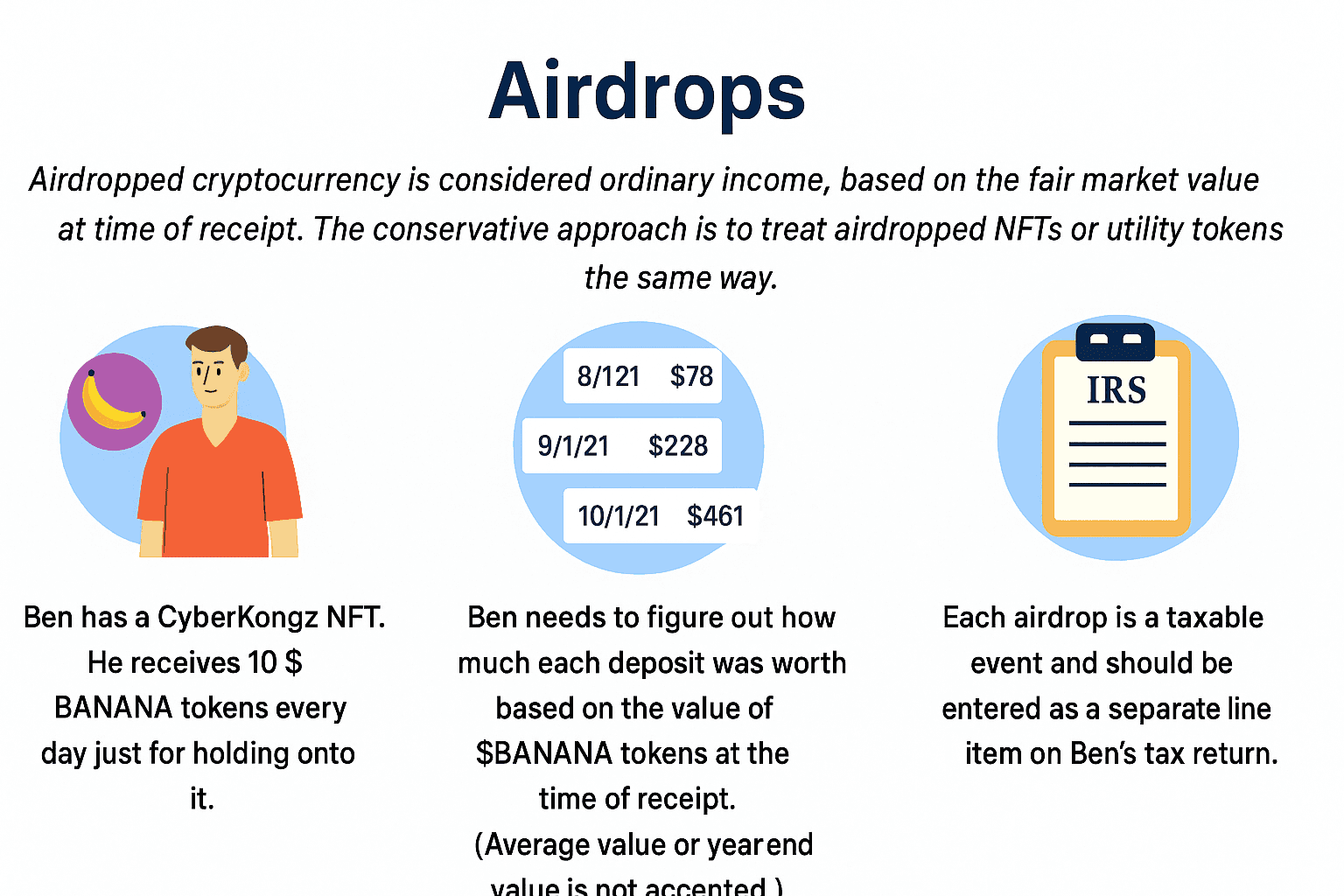

Are There Taxes for Airdrops?

Yes. Airdrops are typically ordinary income when you control the asset. While IRS guidance highlights cryptocurrencies, many taxpayers conservatively treat NFT or utility token airdrops the same way.

Is USDC Taxable?

Yes. Stablecoins such as USDC are treated like other crypto for tax purposes. Trading or converting them can trigger capital gains or losses.

Which Crypto Transactions Are Not Taxable?

Certain transactions are non-taxable, though you may still need records for accurate basis and reporting. Common non-taxable events include:

- Buying crypto with U.S. dollars or other fiat currencyMoving assets between your own wallets or exchanges

- Holding crypto as it appreciates without disposing

- Giving or receiving crypto as a gift within annual and lifetime limitsDonating crypto to a qualified nonprofit

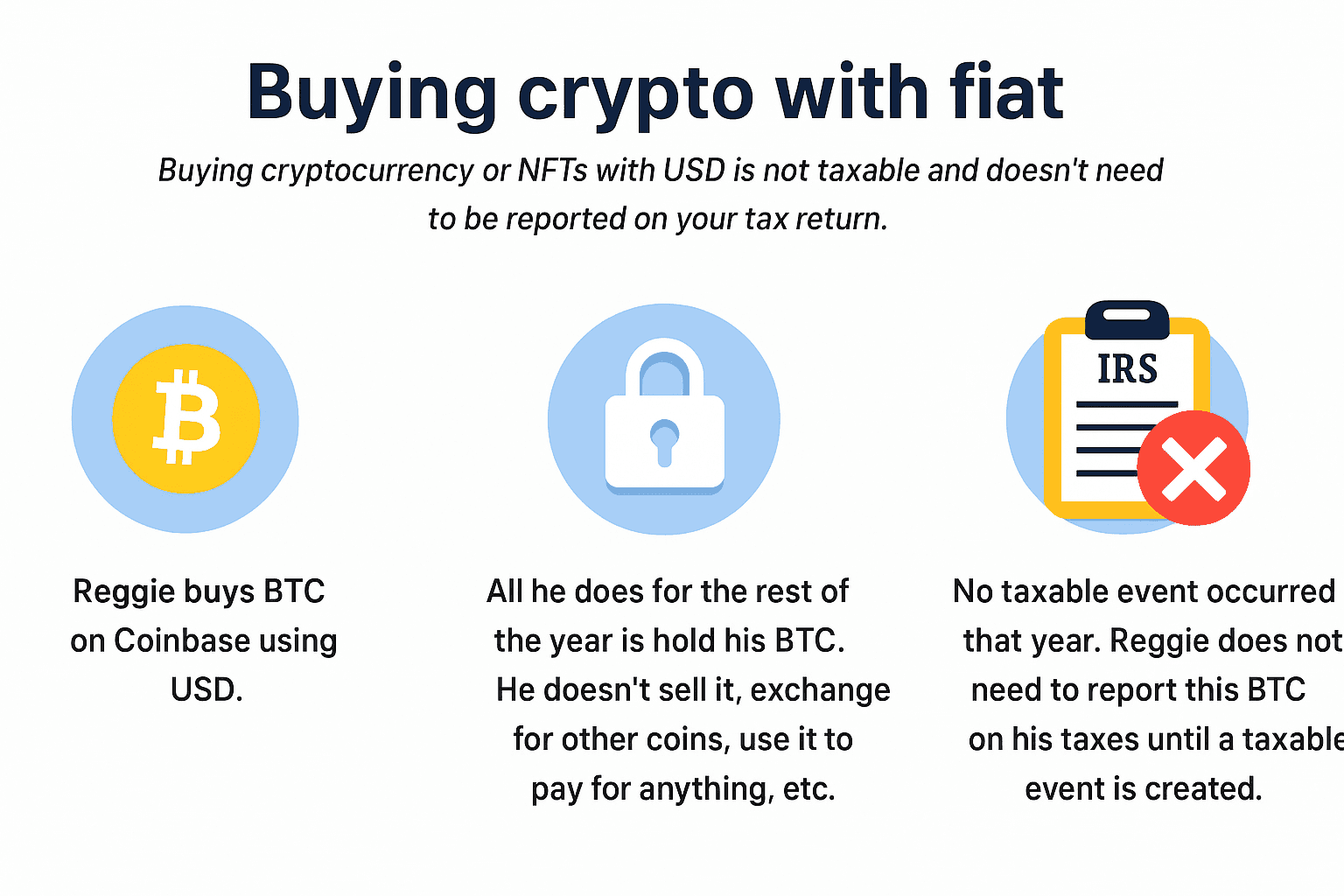

Is Buying Crypto a Taxable Event?

Purchasing with fiat alone is not taxable. If buying was your only crypto activity, you generally do not need to check “yes” to the virtual currency question on Form 1040.

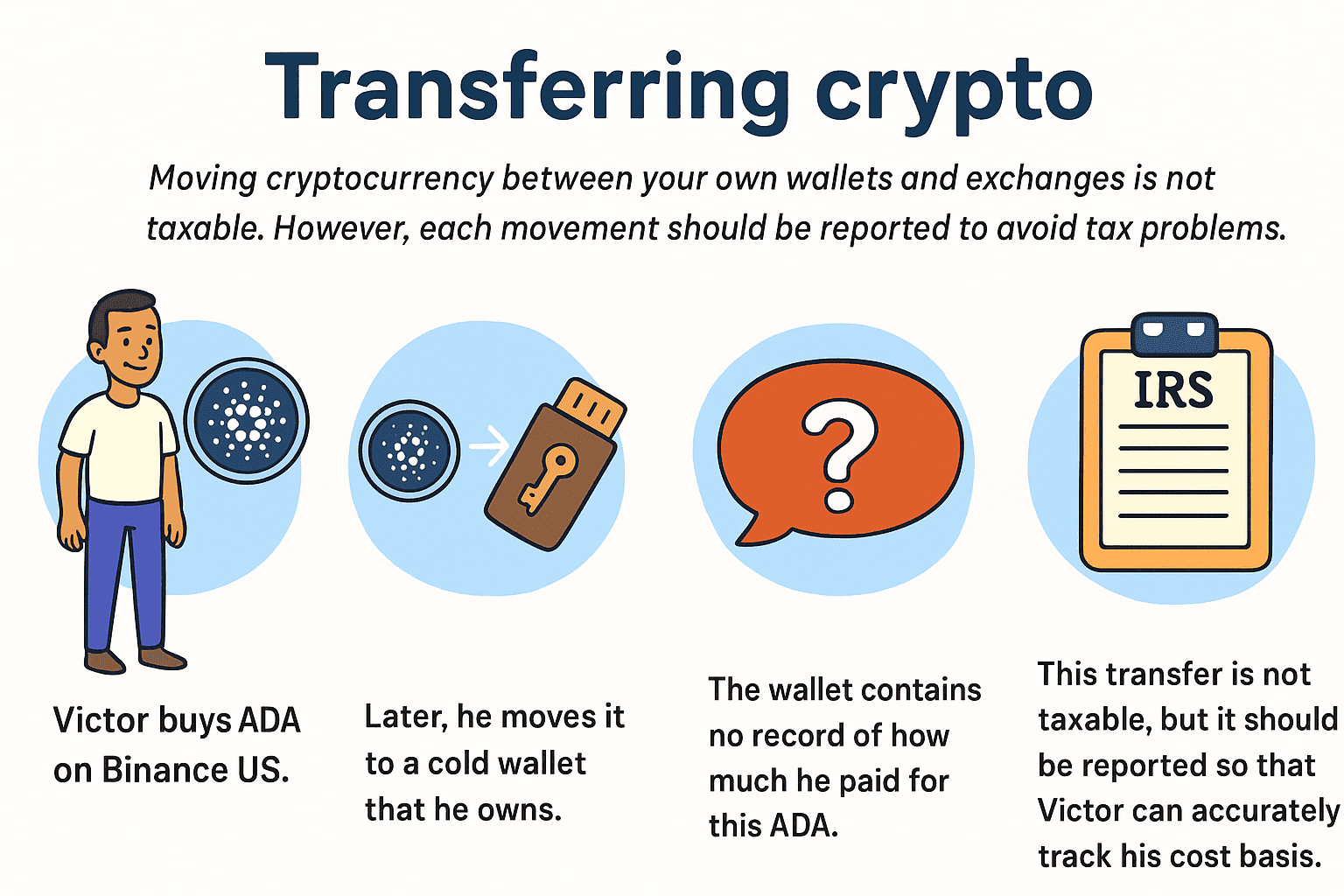

Is Transferring Crypto a Taxable Event?

Transferring coins between accounts or wallets you control is generally not taxable—it’s like moving funds between pockets. Still, keep detailed records so you can match transfers and maintain cost basis continuity.

Crypto tax software often misclassifies self-transfers as taxable. If software inflates activity or income, get expert help to correct it.

If My Crypto Has Gone Up in Value, Do I Have to Pay Tax?

Not until you dispose of it. Unrealized gains while holding are not taxable unless you qualify for special trader treatment. Once you sell, swap, or spend, tax rules apply.

Is Sending Crypto Taxable?

Gifting crypto is typically not taxable to the donor if you stay within annual and lifetime limits. You may need a gift letter or gift tax return, and the transfer must be unconditional with full control relinquished.

Sending crypto between your wallets is not taxable. Paying someone with crypto for goods or services is a taxable disposal.

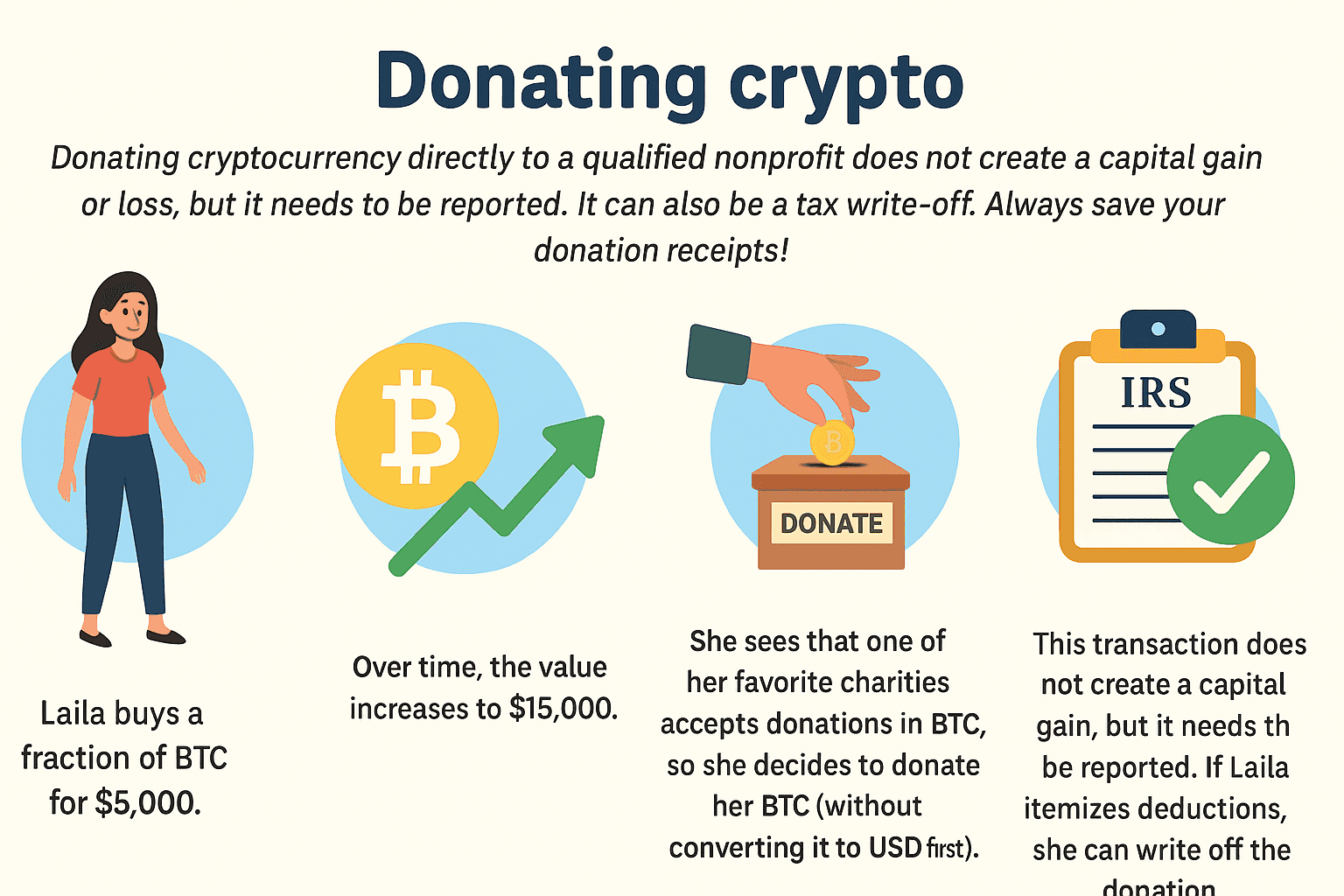

Is Donating Crypto Taxable?

Donations of crypto to eligible charities do not trigger capital gains tax, and the donation may be deductible. It’s a powerful strategy to reduce taxes on appreciated assets.

Do I Have to Report Crypto If I Lost Money?

Yes. You must report losses as well as gains. Doing so can help offset profits and lower your overall tax bill, while also preventing potential IRS headaches. Accurate reporting of both sides ensures you don’t overpay.

In general, capital losses from crypto can offset capital gains. If you have more capital losses than capital gains for the year, you can typically deduct up to $3,000 of the excess against other income ($1,500 if Married Filing Separately), and carry any remaining unused loss forward to future years.

Do Crypto Exchanges Report to the IRS?

Many exchanges send information to the IRS. When the IRS already has data on your accounts, accuracy on your return becomes critical.

Common forms used include 1099-MISC and 1099-B. For crypto, these often do not provide everything needed to file correctly.

Tax enforcement isn’t limited to what a platform emails you. The IRS can match exchange reports to your return, request records, and use blockchain analytics to identify patterns that suggest unreported activity.

In addition to exchange reporting, the IRS may use information-sharing agreements, summonses, and transaction tracing on public blockchains to connect addresses and activity to taxpayers. Form 1099-DA is designed to standardize digital asset reporting, and it can make mismatches between what you report and what a broker reports easier to detect.

Popular exchanges that share data with the IRS include:

- Coinbase

- Binance US

- Kraken

- Gemini

- Bitstamp

- Robinhood

- Cash App

- PayPal

Pro Tip: Beginning January 2026, cryptocurrency “brokers”—including decentralized exchanges and certain wallets—will issue Form 1099-DA. Activity in 2025 will be tracked, making IRS crypto audits easier and unreported activity easier to spot.

What Happens If I Don’t Report Crypto on My Taxes?

Skipping or misstating crypto transactions can lead to significant consequences: audits, steep penalties, and even criminal tax exposure in severe cases.

The IRS has targeted crypto evasion for years and will soon receive much more detailed information via Form 1099-DA. File correctly to stay out of trouble.

Gordon Law Group can help fix past returns and resolve issues. If you’re worried about your crypto filings, contact us for assistance.

How to Avoid Crypto Taxes

You may not be able to eliminate taxes entirely, but smart planning can legally lower what you owe on digital assets. Common approaches include harvesting capital losses to offset gains, holding positions longer to potentially qualify for long-term capital gains rates, donating appreciated crypto to avoid recognizing the built-in gain, and timing sales so gains and losses fall in the same tax year. Depending on your situation, you may also be able to defer or reduce tax by using certain retirement account strategies (where available) or by structuring activity so income and deductions are properly matched.

Our tax planning team helps crypto traders choose strategies tailored to their situation.

How to Report Crypto on Taxes

Accurate reporting keeps you compliant and reduces the chance of IRS problems. In general, crypto activity is reported on your annual federal return for the tax year, and any tax due is typically paid by the filing deadline. If you have significant crypto income or gains during the year, you may also need to make estimated tax payments so you’re not underpaid when you file. An extension can give you more time to file, but it usually does not extend the time to pay.

On the federal side, crypto reporting commonly involves Form 1040 (including the virtual currency question), Form 8949 (to list disposals and calculate gains and losses), and Schedule D (to summarize overall capital gains and losses). Crypto-related income may also be reported on Schedule 1 (for certain “other income” items) or Schedule C (for business income, such as certain mining or self-employment activity). Information documents such as Form 1099-DA, Form 1099-MISC, or Form 1099-B may be provided by exchanges or brokers, but you still must reconcile them to your complete records.

Follow these steps to file correctly:

- Step 1: Gather records. Collect any tax forms from exchanges and export complete transaction histories from every exchange, wallet, and account you used during the year.

- Step 2: Compute gains and losses. For each trade or disposal, calculate the capital gain or loss and compile them for Form 8949. Consider specialized crypto software or a seasoned crypto tax professional.

- Step 3: Summarize on Schedule D. After completing Form 8949, carry the subtotals to Schedule D to report overall capital gains and losses.

- Step 4: Report ordinary income. Include crypto income—such as payments, mining, staking, and rewards—on the appropriate lines (often Schedule C for business activity). Don’t rely solely on exchange forms.

- Step 5: Get expert help. Complex scenarios often require legal and tax analysis. A professional can validate positions and reduce risk.

By following this workflow, you can file with confidence. If you hit a snag, Gordon Law Group can streamline the process and deliver accurate crypto tax reports.

Best Way to Do Crypto Taxes

If you trade frequently or interact with DeFi and NFTs, an experienced crypto accountant is usually the most reliable and time-saving option. Gordon Law Group can also prepare and file your entire return.

Crypto tax software can help with cost basis and reporting, but complex activity often requires significant cleanup to achieve accurate results.

Common problems with crypto tax software include:

- Limited or no support for NFTs and DeFi transactionsInability to connect to niche chains

- Misclassifying self-transfers as taxable activity

- Overstating income or gains

We provide advanced troubleshooting for crypto tax software. If you can’t get clean results, save time and money by working with our crypto tax team.

No comments yet. Be the first to share your thoughts.